Introduction

NVIDIA reported another solid quarter that underscores the strength of the long-term AI infrastructure story, even as near-term execution showed a few cracks. Q2 results featured revenue growth of 56% YoY and another EPS beat, though datacenter segment revenue modestly lagged Wall Street’s lofty expectations. Importantly, the magnitude of quarterly beats continues to narrow, reflecting the difficulty of exceeding the very high bar that the Street has now set.

Despite this, management commentary reinforced the view that demand remains well ahead of supply. Phrases like “everything is sold out — H100, H200, and Blackwell” highlight how structural demand continues to outpace NVIDIA’s ability to ship product. Against this backdrop, we roll forward our model, incorporate a higher baseline of growth, and raise our price target to $227.3 per share (from $196). Overall, we see this quarter as a net positive, reaffirming that the AI trade is alive, thriving, and compounding long-term value creation.

Our view

This was a constructively positive quarter, even if some metrics fell short of whisper expectations. The company continues to post outsized YoY growth above 50%, while gross margins hold above 72%. Importantly, NVIDIA is not demand-limited — it is supply-limited.

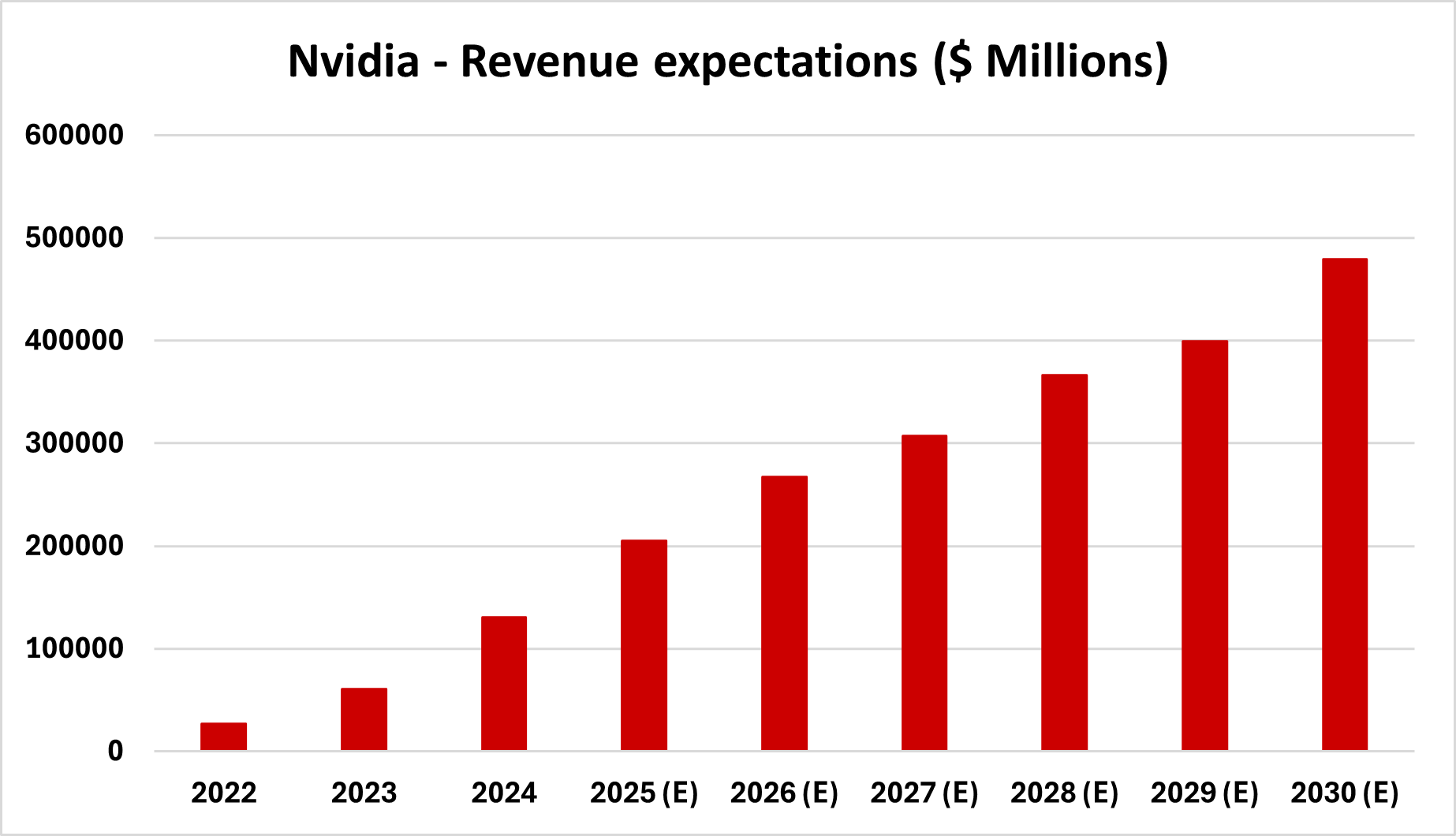

The long-term AI thesis is intact and strengthening: NVIDIA now pegs AI infrastructure TAM at $3–4 trillion by decade’s end, up from $600B today. The current market is almost exclusively CSP-driven, but over the coming years, enterprises, sovereigns, startups, and neo-cloud providers will increasingly contribute to demand, broadening the customer base and deepening the market opportunity. This implies a 40%+ CAGR for AI infrastructure spend through 2030.

Rolling our model forward by one quarter and incorporating stronger baseline numbers from this print, we raise our price target to $227.3/share (from $196). While risks remain around China policy and rising competition from custom silicon, the durability of NVIDIA’s demand pipeline, visibility into the Rubin product cycle, and unmatched ecosystem lock-in make this quarter a reaffirmation of the company’s central role in the AI trade.

Unpacking the $3–4 Trillion TAM Number

Of the overall cost of setting up AI-related datacenters, the cost of compute, networking, and other adjacent businesses where NVIDIA has exposure makes up roughly 30–40%.

Within this segment, compute alone takes the lion’s share, and today NVIDIA commands an ~80% share of the compute market. While custom silicon adoption and competition from AMD may erode some share, we believe it is reasonable to assume NVIDIA retains ~50% share, given its first-mover advantage and currently irreplaceable tech stack.

Running back-of-the-envelope calculations based on this framework yields a 5-year forward revenue potential of ~$500B, implying a CAGR of ~20%. This highlights the enormous runway for growth, even after the unprecedented scaling NVIDIA has achieved over the past 24–30 months.

That said, we caution that execution risk remains. The biggest trigger for a blip in this roadmap would be inadequate returns on the massive investments being made by hyperscalers, neo-clouds, enterprises, and sovereigns. If AI workloads fail to deliver expected monetization, infrastructure spend could temporarily retrace.

Key Data Points

Q2 FY2026 Results (ended July 27, 2025):

- Revenue: $46.7B (vs. $46.1B consensus) → +56% YoY, +6% QoQ.

- GAAP EPS: $1.08; Non-GAAP EPS: $1.05 (vs. $1.01 consensus).

- Gross margin: 72.7% non-GAAP (inline).

- Datacenter revenue: $41.1B, up 56% YoY but slightly below whisper expectations.

- Gaming revenue: $4.3B (+49% YoY).

- Professional visualization: $601M (+32% YoY).

- Automotive: $586M (+69% YoY).

Cash Flow & Capital Returns

- $24.3B returned to shareholders in H1 FY2026 via buybacks/dividends.

- Board approved additional $60B buyback authorization (no expiration).

- $14.7B remains under existing authorization.

- Dividend: $0.01/share payable Oct 2, 2025.

Q3 FY2026 Guidance (vs. consensus):

- Revenue: $54B ±2% (cons. ~$53B).

- Gross margin: ~73.5% non-GAAP (±50bps).

- OpEx: $4.2B non-GAAP.

- Other income: ~$500M.

- Tax rate: ~16.5% (±1%).

- Importantly, no H20 shipments to China included in outlook.

Key Takeaways from the Call

- China uncertainty: CFO Colette Kress emphasized that H20 shipments to China are not included in Q3 guidance. If export restrictions ease, management estimates a $2–5B upside. Jensen Huang reinforced China’s importance to global AI research.

- Demand still supply-constrained: Huang noted “everything is sold out — H100, H200, and Blackwell”. Supply remains the gating factor, not demand.

- AI Infrastructure TAM: Management framed a massive $3–4 trillion AI infrastructure opportunity by 2030, compared to ~$600B today. Importantly, today’s spend is almost entirely concentrated among large cloud service providers, but future growth will be driven not only by CSPs scaling further but also by enterprises, startups, sovereign AI projects, and emerging neo-cloud players entering the market.

- Rubin roadmap: Next-generation Rubin GPUs are already in fab, with volume shipments expected in 2026. Provides visibility into NVIDIA’s product cadence.

- CSP dynamics: Management highlighted trillion-dollar CSPs increasingly collaborating with each other to secure AI capacity (e.g. Meta recently signing up for cloud capacity from Google), a rare sign of scarcity at scale.

- Networking strength: Spectrum-X Ethernet and InfiniBand adoption continue to support full-stack datacenter leadership.

%20(16).png)

.png)

.png)