Data centre-driven load is reshaping the utility ecosystem from planning and regulation through to tariffs, risk allocation and infrastructure build‑out, and regulators are rapidly rewriting rules to protect existing ratepayers while still enabling growth. The core tensions are who pays for new wires and generation, how to manage reliability amid very large, spiky loads, and how to avoid a build‑out pipeline that outruns realistic data centre demand.

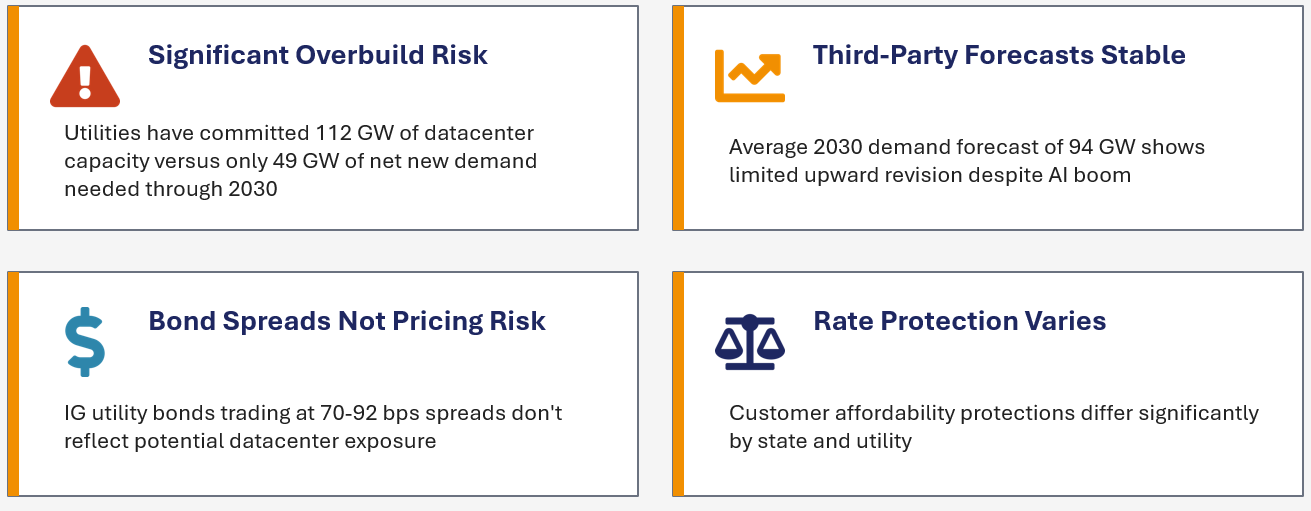

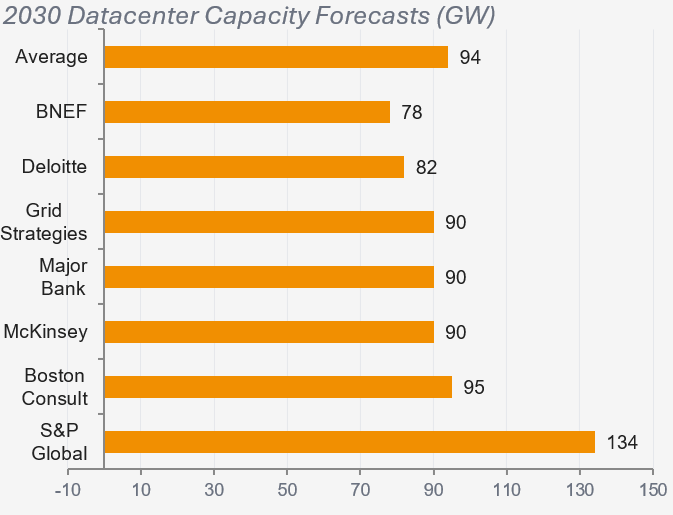

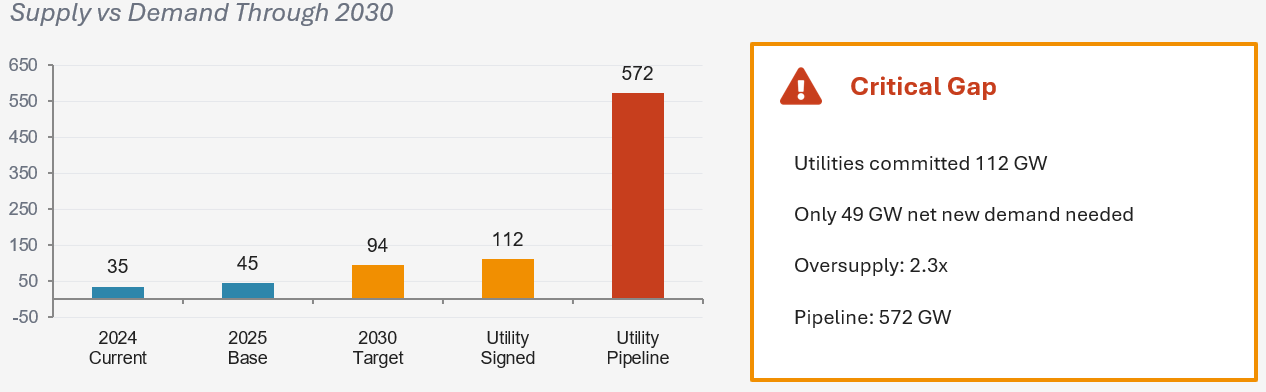

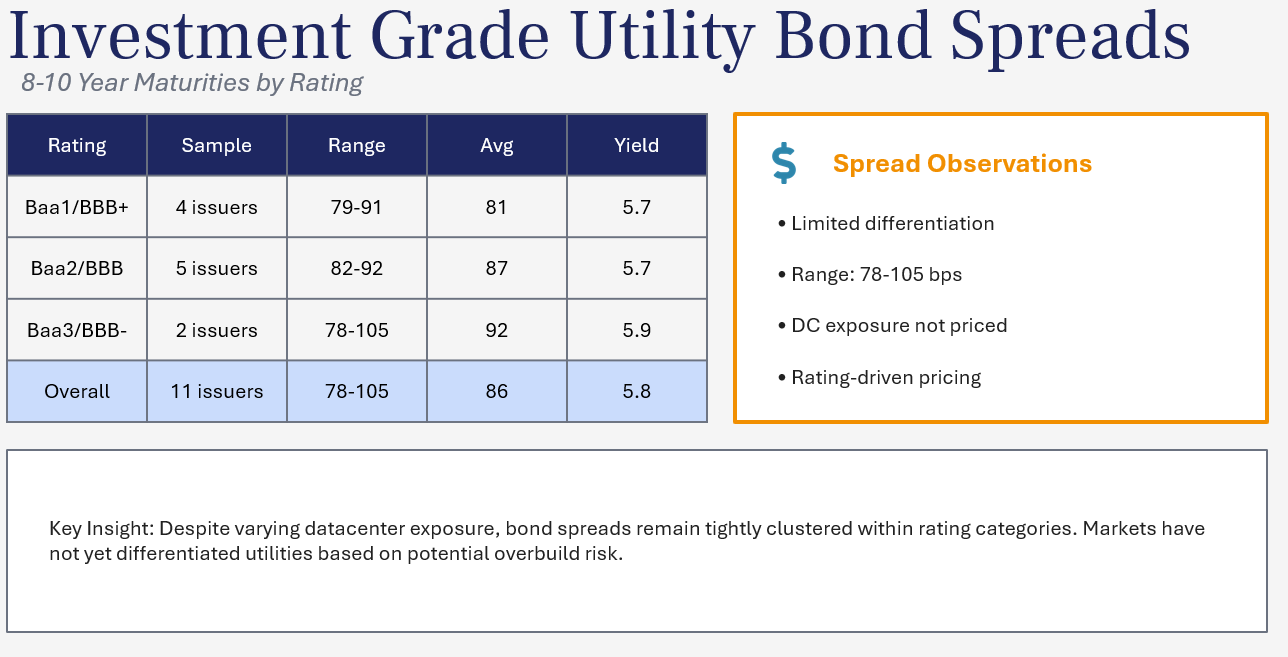

The U.S. utility sector is entering a period of heightened uncertainty. This is driven by aggressive datacentre capacity commitments that significantly outpace projected demand growth. Third-party forecasts for datacentre power needs have remained largely stable. These forecasts show limited upward revision despite widespread enthusiasm around artificial intelligence. This raises questions about whether supply plans are getting ahead of actual consumption trends. At the same time, investment-grade utility bond spreads remain compressed. They show little differentiation based on datacentre exposure. This suggests that credit markets have not yet begun to distinguish between utilities with varying levels of overbuild risk. Compounding this, the strength of ratepayer protection mechanisms differs meaningfully across states and utilities. This creates an uneven regulatory landscape. Utilities operating in jurisdictions with weaker affordability safeguards could face greater credit pressure if datacentre demand fails to materialize as expected. Taken together, these dynamics point to a disconnect between the scale of capital being deployed and the market's current assessment of the associated risks.

Before we deep dive into the core a basic understanding of the ecosystem is warranted.

The basic ecosystem

- Developer / hyperscaler: Google, AWS, Microsoft, AI players seeking huge, often 24/7 power blocks, with tight timelines and sometimes green‑power requirements.

- Transmission owner / RTO / ISO: Manages interconnection studies, transmission capacity, and often capacity markets (e.g., PJM, SPP, ERCOT‑adjacent).

- Regulated utility (wires + often generation): Files integrated resource plans (IRPs), requests capex and rate hikes to serve new load, designs large‑load tariffs.

- Regulator (PUC/BPU etc.): Has the statutory mandate to ensure "just and reasonable" rates, prevent undue discrimination, and apply cost‑causation so existing customers don't cross‑subsidise new data centres.

- Retail customers (residential, small C&I): Ultimately bear costs in bills unless regulators ring‑fence costs to large loads.

Risk of overbuilding: pipelines vs real demand

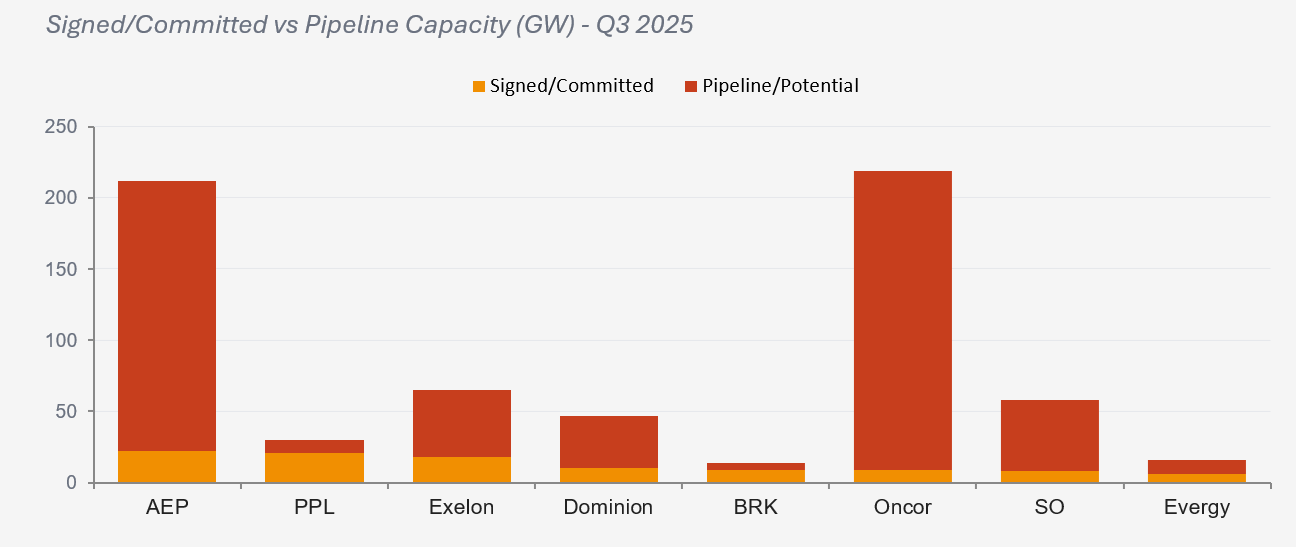

Conceptually, the core risk is that the pipeline of planned lines, substations and plants is ultimately sized off a short‑cycle technology boom (AI/ML compute demand) rather than long‑cycle, regulated load growth, with ratepayers holding the residual if the cycle turns.

Regulators and consumer advocates are increasingly concerned that today's exuberant AI and cloud narratives could lead utilities to overbuild generation and grid capacity based on inflated data centre demand forecasts. That creates several risk vectors:

- Stranded asset risk: If the AI/data centre boom slows, fails to materialise as forecast, or shifts to other regions or on‑site solutions, utilities could be left with excess capacity and long‑lived assets whose costs still flow into rates.

- "Boom‑bust" rate cycles: A surge in grid capex justified by short‑term load growth can create multi‑year bill increases for households and small businesses if large customers exit or renegotiate, triggering political backlash and regulatory pushback.

- Moral hazard from guaranteed recovery: If regulators allow utilities to roll nearly all data centre‑driven capex into the generic rate base with weak minimum‑take or collateral requirements, they blunt incentives to scrutinise demand forecasts or negotiate robust contracts.

- Planning and governance responses: Emerging policy proposals emphasise proactive regulatory approaches, scenario‑based IRPs, and explicit rules that tie approval of new capacity to firm offtake commitments, cost sharing and risk‑transfer mechanisms for large loads.

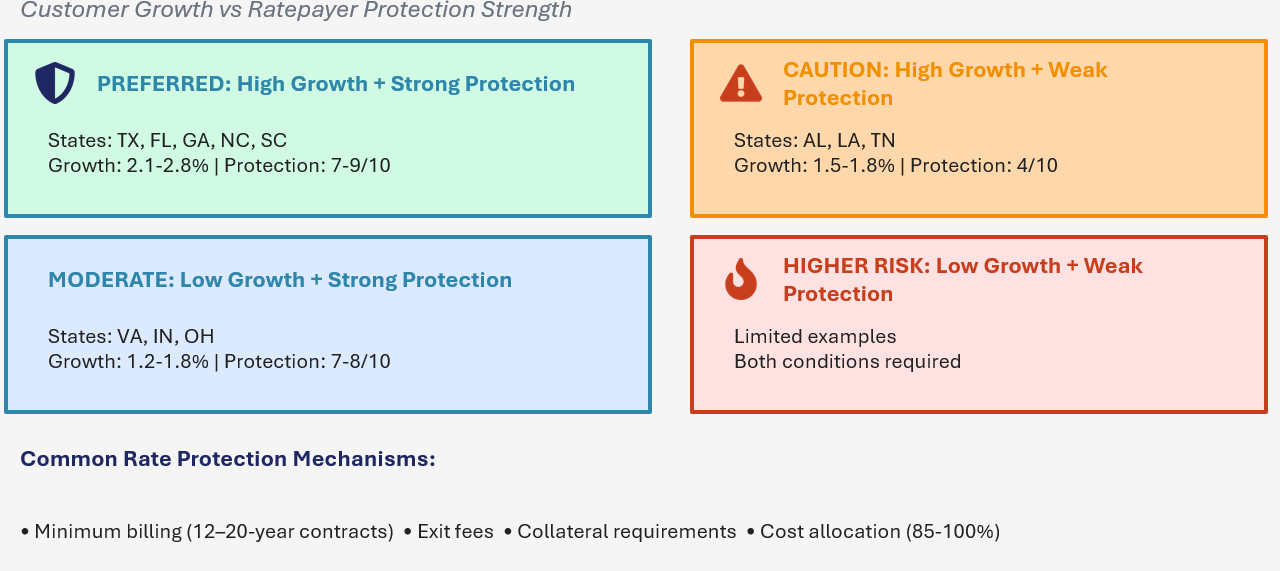

Ratepayer protections and tariff design

A key political and regulatory response has been to ensure that data centres pay for the incremental grid and generation costs they cause, rather than socialising these across households and small businesses. Tools now commonly used include:

- Minimum billing demand / take‑or‑pay: Contracts require large loads to pay for 80–90% (sometimes more) of contracted capacity even if they don't fully use it, protecting utilities from stranded costs if the load underperforms or exits.

- Special large‑load tariffs: States are explicitly authorising separate tariffs for loads above a threshold (e.g., 50–150 MW), with higher fixed charges, tailored demand charges, and sometimes curtailment provisions.

- Cost‑causation and direct assignment: Transmission and distribution upgrades required to serve data centres are increasingly being directly assigned to those customers under "you pay for what you trigger" principles.

- Prohibitions on undue discounts: Some proposed rules would bar deep discounts on fossil‑heavy PPAs for data centres if these lead to higher bills for everyone else.

- Legislative guardrails: Multiple US states have passed laws requiring studies of whether non‑data‑centre customers are "unreasonably" subsidising them and exploring special tariffs or contributions to grid upgrades.

Disruptions and operational risks

Very large, geographically clustered data centres can create both short‑term operational stress and new systemic risk modes for the grid. Key disruption channels:

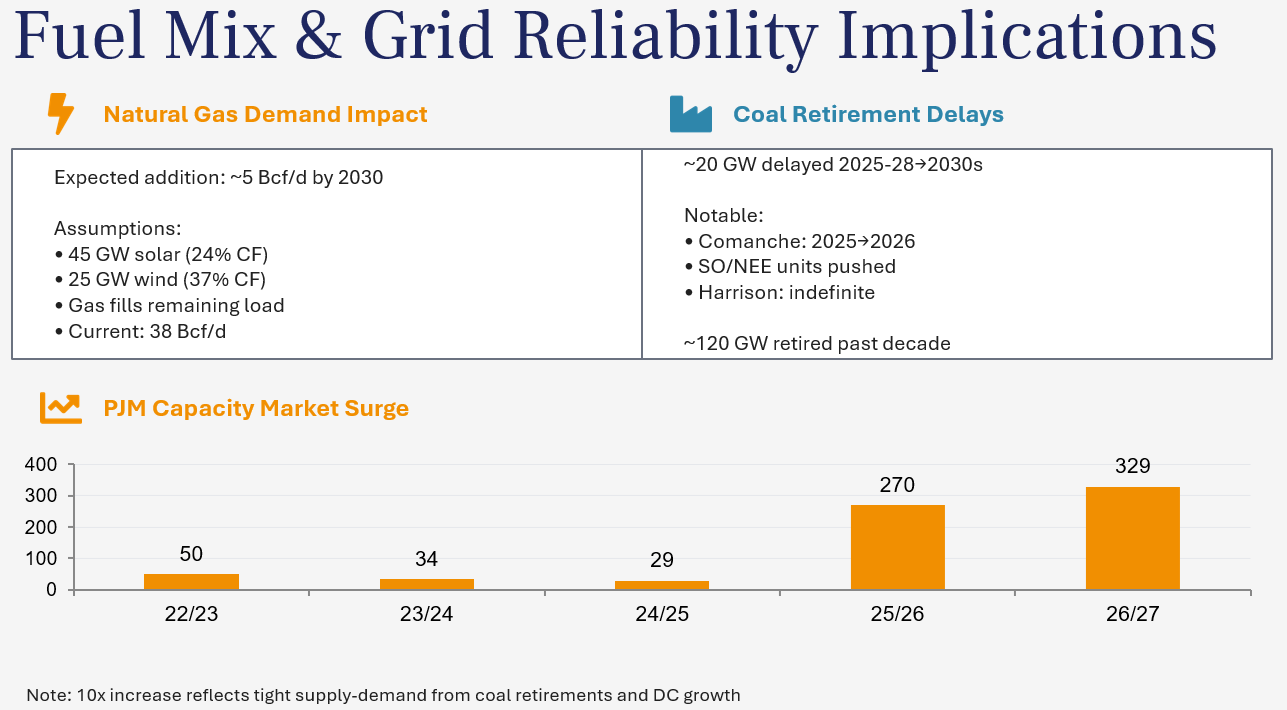

- Local grid strain and congestion: Data centres can draw as much power as a mid‑sized town, driving congestion and local price spikes, and forcing accelerated transmission and distribution reinforcement.

- Frequency and stability issues: AI data centres have highly variable and sometimes abrupt load changes, challenging frequency regulation and voltage stability if not properly managed with grid‑side and load‑side controls.

- Event risk from sudden disconnection: A 2024 incident in Virginia's "Data Centre Alley" saw 60 of over 200 data centres disconnect quickly due to a protection malfunction, forcing them onto on‑site generation and stressing the wider system.

- Outage and reliability externalities: When utilities or RTOs cannot bring enough capacity or network upgrades online in time, the concentration of large loads heightens the risk of brownouts or voltage sags for surrounding customers.

In response, emerging frameworks (e.g., SPP's High Impact Large Load rules) integrate load and generation interconnection, require firm commitments and sometimes curtailment or self‑supply to maintain reliability and ensure that large loads internalise the stability costs they impose.

Credit Implications

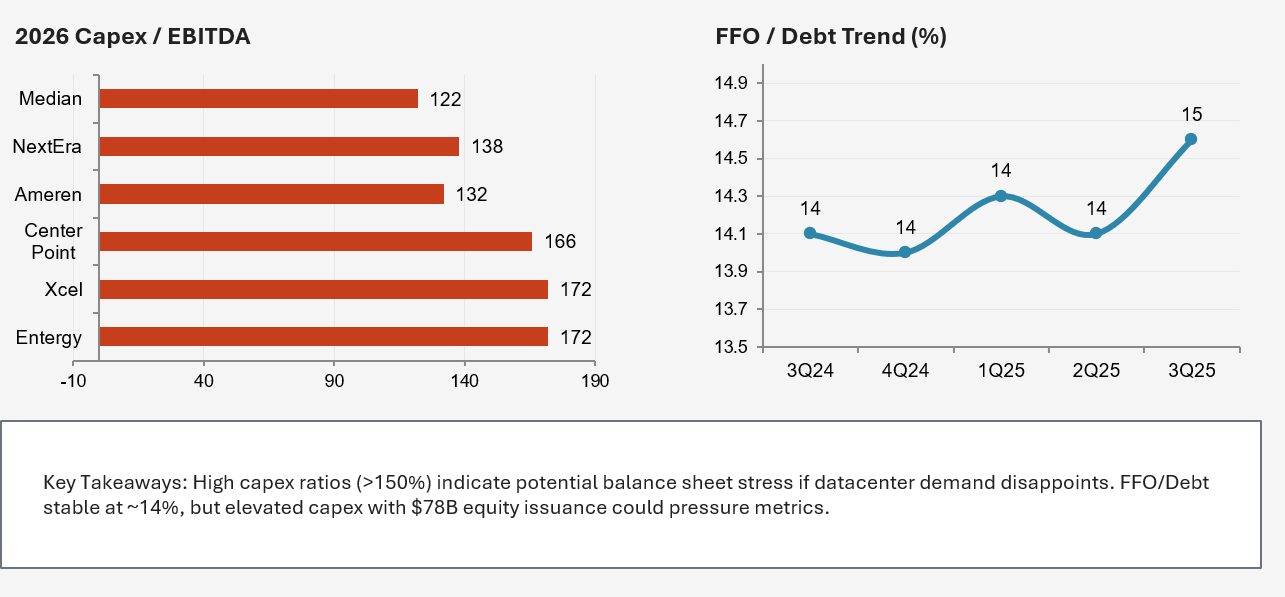

U.S. utilities are deploying capital at an aggressive pace to meet anticipated datacentre demand, pushing capital expenditure levels well above historical norms relative to earnings. Several issuers are running capex-to-EBITDA ratios that exceed comfortable thresholds, signalling potential balance sheet strain if the expected load growth fails to materialize. While funds from operations relative to debt have remained broadly stable in recent quarters, this apparent resilience masks the scale of forward-looking commitments — the sector has collectively turned to substantial equity issuance to fund expansion, introducing dilution risk alongside rising leverage. The concern is straightforward: if datacentre demand disappoints against the backdrop of a significant oversupply of committed capacity, utilities could find themselves carrying stranded or underutilized assets financed by debt and equity that now weighs on credit metrics. Spread widening, downward rating pressure, and further equity needs become realistic outcomes in a demand shortfall scenario. The market's current pricing, which shows minimal spread differentiation based on datacentre exposure, suggests that these balance sheet vulnerabilities are not yet being reflected in credit valuations — leaving limited margin for error if the overbuild thesis plays out.

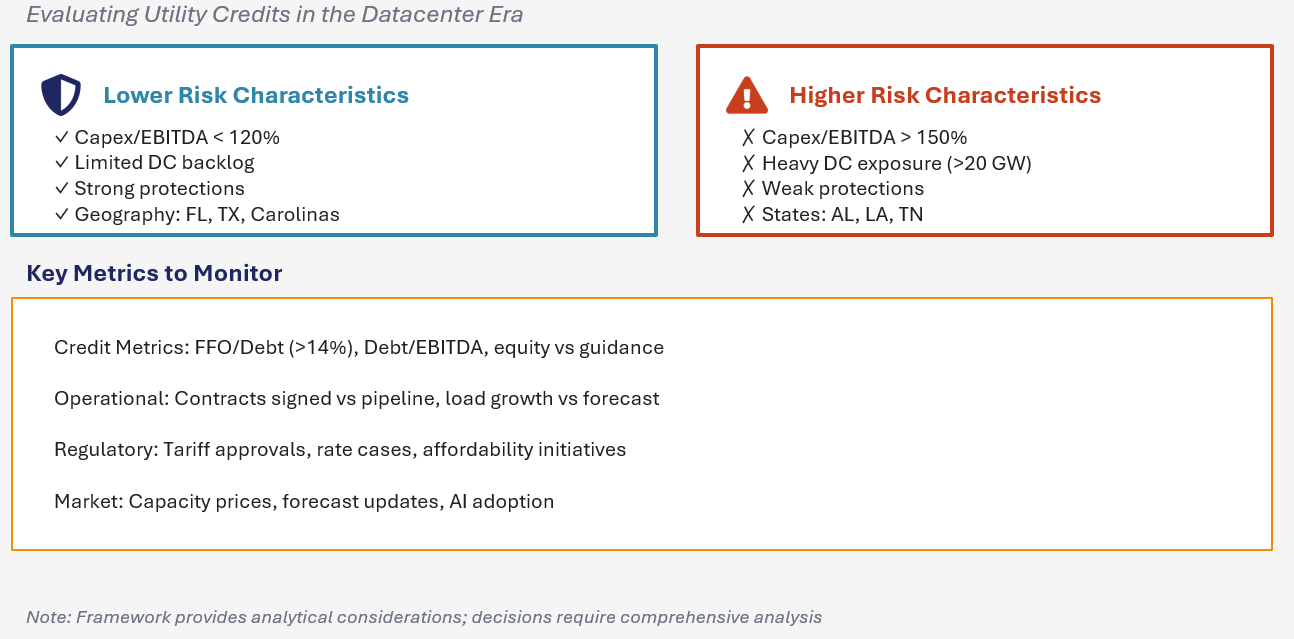

Conclusion

The investment framework for evaluating utility credits in the datacentre era draws a clear line between lower-risk and higher-risk profiles. Utilities with moderate capital intensity, limited datacentre backlog exposure, strong ratepayer protection mechanisms, and favourable geographic positioning in states with robust regulatory frameworks represent the more defensible end of the spectrum. Conversely, issuers carrying elevated capex burdens relative to earnings, heavy datacentre pipeline commitments, weak affordability safeguards, and exposure to jurisdictions with less supportive regulatory environments warrant greater caution. Monitoring should be anchored around four pillars: credit metrics including funds from operations relative to debt, leverage ratios, and equity issuance trends against guidance; operational indicators such as the pace of actual contract signings versus pipeline and realized load growth versus forecasts; regulatory developments including tariff approvals, rate case outcomes, and affordability initiatives; and broader market signals like capacity pricing movements, third-party demand forecast revisions, and the trajectory of AI adoption. The framework underscores that not all utility credits are equally exposed — differentiation based on these factors will be critical as the sector navigates the gap between committed supply and uncertain demand.

.png)

%20(14).png)

.png)