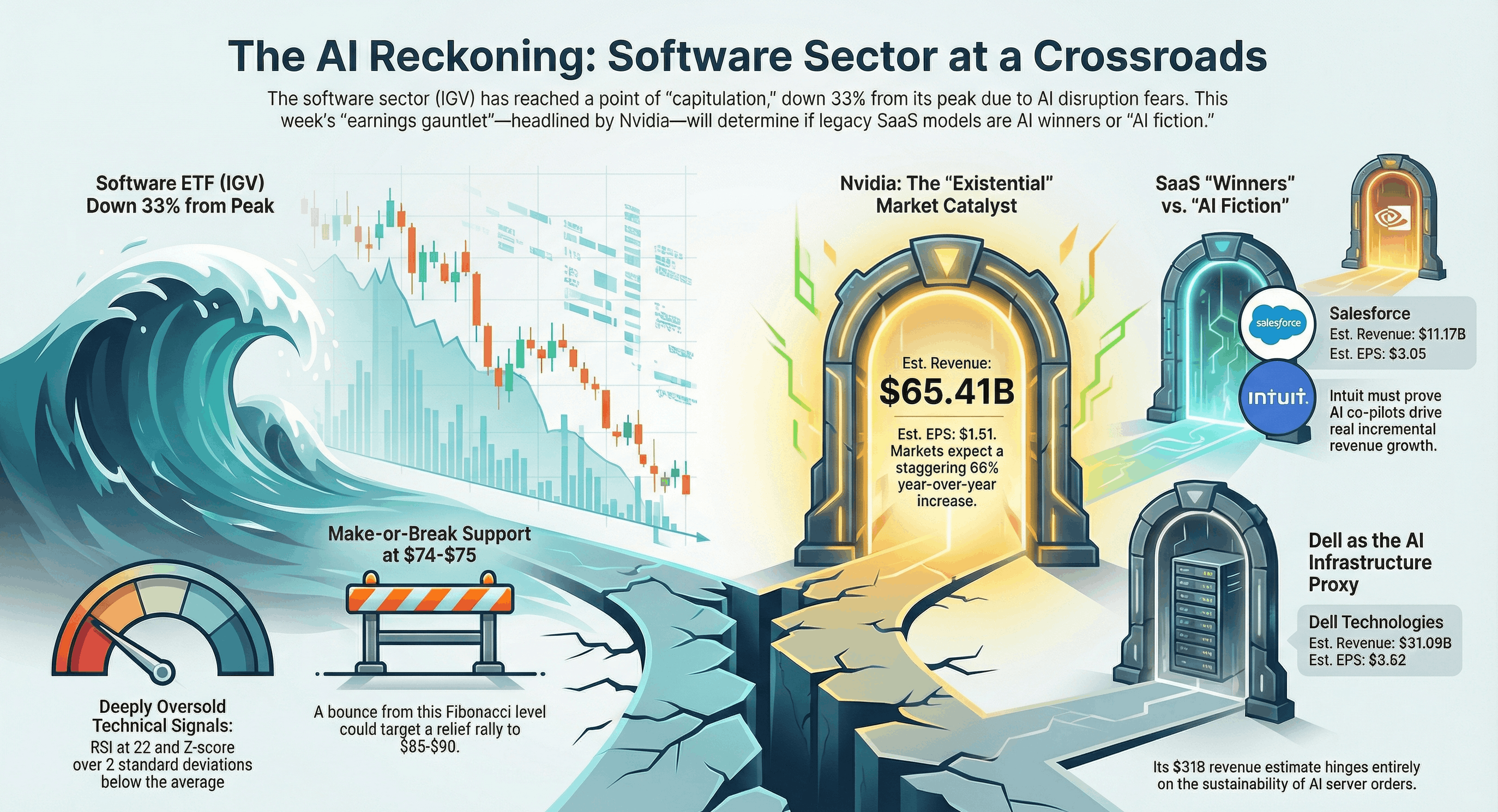

Software sector capitulation has reached fever pitch. IGV is down more than 30% from peak, kissing Liberation Day lows as AI disruption fears materialize.The sell-off is indiscriminate, but is the threat as uniform? While the threat is real, the process takes time. Technicals scream dead cat bounce potential even if fundamentals remain challenged. Nvidia's earnings on Wednesday will dominate. Expectations are elevated and stakes existential. A software earnings gauntlet (Salesforce, Workday, Intuit, Dell) will test whether SaaS business models can withstand the AI onslaught. Macro cross-currents will add fuel - US consumer confidence, house prices, PPI, plus India GDP (forecast 7.8% vs 8.2% prior) signal global growth divergence. Political volatility also looms as Trump likely retaliates to adverse Supreme Court ruling, while Middle East tensions threaten oil/risk-premium expansion.

This earnings season separates AI winners from AI fiction, and with the software sector already priced for Armageddon, even modest beats could ignite savage short squeezes - but only if Nvidia doesn't detonate the entire narrative first.

IGV (Software ETF) DailyChart

The carnage is complete. IGV trading at 8.8 is down 33% in a near-vertical capitulation, now sitting at the 50% Fibonacci retracement level (Oct 22 lows to recent all-time high), after piercing below all relevant moving averages (20/50/200day) with violent momentum. BUT, it's deeply oversold - RSI at 22 and z-score over 2 std deviations below average are at 2022’s depressed levels, levels from where previous up-moves have started. MACD histogram is massively negative, showing extreme bearish momentum but starting to show very early divergence hints at these lows. Spiking volumes into the sell-off suggest capitulation – but is it exhaustion yet?

The $74-$75 zone (61.8% Fib) is make-or-break support; a bounce from here could target $85-$90, while a break would open air pockets to $62 (78.6% Fib) or worse. This is textbook oversold, prime for a violent short-covering rally if positive catalysts emerges (Nvidia beats? Software names surprise? Trump doesn't nuke the market?).

source: Trading View

Sector Rotation Chart

Rotational trends scream risk-off. Technology (XLK) has been underperforming for a while, but shows initial signs of regaining momentum. Meanwhile, value (XLB, XLI) and Defensives (XLU, XLV) have been firmly entrenched in the “Leading quadrant”, but show early signs of fading momentum. What’s been a classic defensive rotation, appears to have gone too far – can tech bounce back? The current setup favors mean reversion trades in oversold growth - any short-covering rally in software could ignite a ferocious rotation back into the Leading quadrant. This week’s earnings from software names and Nvdia will set the tone!

source: Stockcharts

Earnings Calendar

This week's earnings calendar is a high-stakes showdown between old economy resilience and new economy disruption. Wednesday's Nvidia print is the undisputed main event - consensus expects a whopping $65.4B in revenue (+66% YoY) and $1.51 EPS (+70%), driven by Blackwell GPU ramp and hyper-scaler CapEx arms race. Expectations are stratospheric, positioning is crowded, and any guidance disappointment could trigger a sector-wide implosion. Nvidia'sreport will set the narrative for whether AI infrastructure spending remains a one-way bet or faces its first real air pocket.

The software cohort (Salesforce, Workday,Intuit, Autodesk) faces an existential test - can legacy SaaS players provetheir AI co-pilots drive incremental revenue, or are they just cost-cutting their way through a secular decline? Salesforce must demonstrate Einstein GPT is more than vapor-ware and that CRM seat growth isn't cannibalizing into agent-based pricing. Workday's sticky HR platform offers some defensibility, but Intuit faces the ultimate disruption risk - GenAI tax prep could hollow out TurboTax's moat faster than bulls expect. Sell-side is cautiously optimistic, but the guidance tone will matter infinitely more than the Q4 beat. If management teams signal budget scrutiny, longer sales cycles, or pilot-to-production delays on AI products, the sector's dead cat bounce thesis evaporates.

Dell Technologies emerges as a dark horse -its $31B revenue estimate (+30% YoY) hinges on AI server orders, making it a critical Nvidia demand proxy. A strong print with robust Infrastructure Solutions Group growth would validate the AI infrastructure super-cycle; a miss would raise uncomfortable questions about hyper-scaler CapEx sustainability. Meanwhile, mega-cap retailers (Home Depot, Lowe's, TJX) will reveal whether the US consumer is cracking under rate pressure or merely shifting spend. HomeDepot's -4% revenue guide signals housing market pain, but TJX's off-price model should benefit from trade-down dynamics.

source: Trading Economics

Macro Calendar

source: Trading Economics

.png)

%20(14).png)

.png)