Ignore the Narrative. Look at the Numbers

In our previous note, we argued that global investors are measuring India with the wrong ruler, that the Nifty 50 and MSCI India, both heavily concentrated in large-cap legacy businesses, are structurally incapable of capturing India's transformation story. We said the real India lives in the mid-cap universe. In this note, we bring the data. Over the past one year, the Nifty 50 has delivered -5%. This figure is responsible for the narrative currently forming in global investment circles, that India is in a bear market, and that capital should be redeployed elsewhere. And yet, through every month of this supposedly lackluster market, Indian retail investors have kept buying. Systematic Investment Product (SIP) inflows have remained at robust levels, month after month, with domestic investors collectively deploying their savings into Indian equities with a consistency and conviction that has absorbed foreign selling. The domestic investor understands something the foreign investor is missing, that the Nifty, for all its visibility as India's supposed market barometer, is not where the new India is being built.

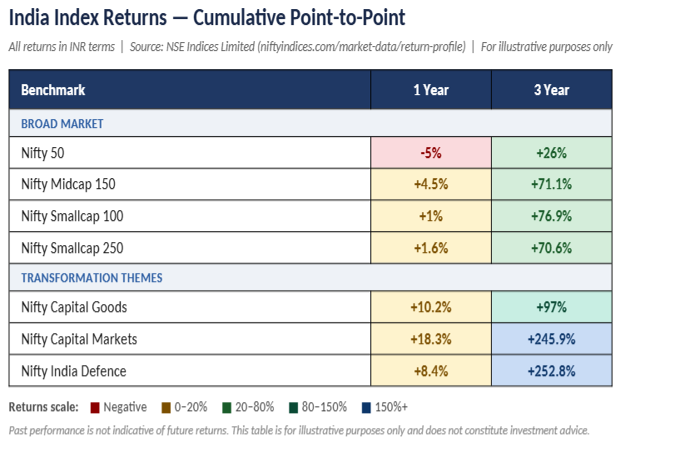

Is India Really in a Bear Market? Ask the Right Index

As we have been highlighting in previous issues of The Beam, the consensus view on India among global investors today can be summarized in three words: expensive, slowing, un-investable. If viewed from the perspective of the Nifty, down 5% over one year, that narrative would be justified. We say the question itself is wrong, because it is being asked of the wrong index. An economy whose capital goods index is up 10% in one year and 97% in three years is not in a bear market. An economy whose defense ecosystem has delivered 250% in three years is not in a bear market. An economy where mid-cap companies, the companies executing India's transformation, have delivered 71% over three years against the Nifty's 26% is not in a bear market.

What India is in is a rotation, a powerful, structural, earnings-driven rotation from the legacy large-cap businesses toward the mid-cap companies that are writing its next one.

Same Country. Completely Different Returns

Let us now look at the data closely. Over the same one-year period in which the Nifty delivered -5%, the Nifty Midcap 150 delivered +5%, Nifty Small cap 250 delivered +2% and Nifty India Capital goods delivered +10%. Defense delivered +9%. These are not different asset classes. They are not different countries. They are India, the same India that the Nifty is supposedly representing. Extend the horizon and the story becomes overwhelming. Over three years, the Nifty 50 has delivered 26%. Respectable. But Nifty Midcap 150 delivered 71% over the same period, nearly 2.5 times the Nifty's return. Nifty Small cap 100 delivered 71%. The themes we speak about delivered far more with Nifty Defense delivering a cumulative 252%. Capital markets delivering similarly and Capital goods 97%.

The Earnings Picture Confirms What the Returns Are Telling You

The return divergence is not a valuation illusion. It is also supported by earnings. Mid-cap India has, over the past three to five years, delivered earnings growth that has structurally and sustainably outpaced the Nifty 50. The reasons are precisely those we identified, organized sector companies gaining market share from unorganized competitors as formalization accelerates; defense companies moving from order booking to order execution as indigenization gathers pace; manufacturers benefiting from China-plus-one supply chain realignment; NBFCs and financiers riding the credit democratization wave into underpenetrated markets. These are not companies re-rating on hope. They are companies delivering on earnings, and in many cases, just beginning to hit their operating leverage inflection points.

Consider what is happening beneath the surface. There are defense electronics companies whose order books today are three to four times their annual revenue, a level of earnings visibility that most Nifty 50 companies would envy. There are specialty chemical manufacturers who have, in the space of three years, gone from being domestic-only players to having forty percent of their revenues denominated in foreign currency, as global agrochemical and pharma companies shift supply chains away from China. There are listed hospital chains expanding into Tier 2 and Tier 3 cities, serving a newly insured middle class that simply did not exist as a paying customer five years ago, and whose revenue per occupied bed has grown twenty percent in two years as the acuity of cases treated rises with insurance penetration. There are capital market intermediaries whose assets under management have grown at thirty percent per annum for four consecutive years, riding the financialization of Indian household savings, and whose operating leverage means that earnings have grown faster still. There are power transmission and distribution companies sitting on order books that are four to five times annual revenues, as India's grid infrastructure races to keep pace with data center demand, electric vehicle adoption and industrial capex. And there are precision cooling companies, specialty cable manufacturers, transformer and switchgear businesses, and high-performance computing hardware assemblers, the unglamorous but essential backbone of India's AI infrastructure buildout, quietly compounding order books and revenues as India's data centre capacity scales from 1.5 gigawatts today toward an estimated 8-9 gigawatts by 2030. Many of these companies are not in the Nifty 50. They are outside the Nifty and in the mid and small cap universe. And they are, without exception, compounding earnings at rates the index simply cannot replicate.

The Next Generation of India Inc is Listing in Mid and Small Cap

What makes this even more compelling is the pace at which the investable universe in mid cap and small cap companies is expanding. In 2024, 75 companies raised approximately $17.9 billion, a record that made India the most active IPO market in the world, accounting for 30% of global IPO listings that year. But the volume tells only half the story. The character of these listings has shifted. Three years ago, India's IPO pipeline was dominated by consumer internet platforms, retail chains and financial services companies. Today it is defense component manufacturers, electronics manufacturing services, specialty chemical exporters, data center infrastructure players, precision engineering firms and capital market intermediaries. Companies that, in many cases, did not exist as listable entities five years ago. Several were too small, too niche or too early in their growth curves to access public markets. They are now mid and small cap companies with institutional shareholding and growing liquidity. The investable universe for India's transformation story is actively growing, and it is growing in exactly the sectors that will define the next decade.

More Than Half of India is Not in the Room

The Nifty 50's fifty companies represent roughly 48% by market capitalization. Which means that by any measure, more than half of India is simply not in the room when global investors discuss Indian equities. But the more powerful point is not the static snapshot. It is growth. Five years ago, the ex-Nifty market capitalization of India, the listed universe sitting entirely outside the fifty names that dominate global perception of this market, was approximately USD 0.9 trillion, constituting 41% of total market capitalization. Today that has increased at a CAGR of 22% to USD 2.4 trillion constituting 52% of the total Indian market capitalization. It has grown 172% in five years. The Nifty 50 itself, over the same period, has grown 70%. The universe that global investors are ignoring has grown at 2.3x the index they are watching. And the share of India's top ten companies in total market value has fallen from 31% in 2021 to 21% today, because newer, mid-sized companies are growing faster than the giants. This is a structural wealth creation event, and it is happening entirely outside the benchmark.

Is the Story Over? No. But It Is a Different Chapter.

A fair question at this point is whether the alpha has already been made. We confess, the most explosive phase of mid-cap alpha creation, the simultaneous re-rating of earnings and multiples that defined much of the 2021 to 2024 cycle, may be largely done in several segments. But double-digit earnings compounding across multi-year structural themes is a very different and very durable return driver. Defense, manufacturing, credit formalization, financialization of savings, AI infrastructure, none of these themes are in their final chapters. Most are in their middle ones. Some are still in nascency. This assessment is supported by the macroeconomic backdrop. With a structurally benign oil price environment that materially improves India's current account and fiscal arithmetic, three significant trade deals in various stages of completion that will open new export corridors for Indian manufacturers, and a capex cycle that is transitioning from government-led to increasingly private-sector driven, dormant for nearly a decade, is finally showing up in order books across capital goods, engineering and manufacturing, the preconditions for sustained mid-cap earnings compounding remain firmly in place.

.png)

%20(14).png)

.png)