Policy makers (governments and central banks), since the GFC, appear to have found the ultimate recipe to perpetuate growth cycles without any major bumps through a combination of fiscal and monetary stimulus. Just as irrigating an already flooded farm has implications for crop growth, the same applies to economies – you can borrow growth from the future, but there is an eventual payback – problem is governments and policy makers are happier aligning their actions with the election cycle. Besides, long-term is a theoretical concept anyway and in the investment world, it’s often described as a short-term investment gone bad!. Irrespective, markets love the stimuli, and who are we to argue.

In context, the previous two weeks have seen the unleashing of monetary easing in the two largest economies, for different reasons – one to retain growth (the US) and another one to revive growth (China). Despite this difference, the backdrop is similar in many respects – both economies have built up considerable leverage since the GFC, admittedly at the sovereign level (in the case of China, quasi-sovereign, through LGFVs). Similarly, the monetary easing path is aimed at stimulating demand through leverage build up in private hands (corporate and individuals) to support growth. While eventually monetary measures stimulate credit growth, do note, borrowing decisions are far more pro-cyclical (and hence positively correlated with interest rates) and depend on cash flow outlook/ confidence, far more than interest rates alone. Whether the Fed or the PBOC succeed in instilling this confidence to get the necessary leverage driven growth boost, remains to be seen – but the markets are clearly loving it.

There is however a point of distinction, almost an accident rather than a planned one, in our view. Arguably, the US economy sits atop a 15+ year expansionary cycle. On the flip side, China’s long-ish covid shut down has brought the economic cycle closer to early stage and somewhat diametrically opposite to that of the US business cycle. More than structural trends, we love cyclical trends as these can be far more profitable for investors – besides, as we noted earlier, long-term is theoretical!

.png)

China

It's easy to dismiss the budding optimism in China Equities following monetary measures announced in late Sep. Naysayers will cite lack of fiscal stimulus, inadequate measures to boost depressed consumption, parallels with Japan, excessive leverage amongst other long-term headwinds, leading to yet another fake-out. While these are factual, legit misgivings, and in many respects we do share some of the skepticism, the counterpoint of cumulative monetary signals stimulating growth at the margin, can also not be dismissed. For market participants, counter-trend moves (in risk assets) can be profitable affairs, especially in an asset class that has been so off-the investors' radar. Valuations may not be a catalyst, but cheap valuations do help the case.

Positioning comes with plenty of risks - aside from this potentially being yet another false dawn, an inevitable pullback after the initial burst is also a distinct possibility. We hold the view that should the measures take hold, there is likely to be substantial upside, even if just a momentum trade. And given the context of an over 55% decline in HSCEI, since early 2021, if it’s real, it ain’t late!.

How to Position

With the over-riding proviso that any positioning in China carries “another false dawn” risks, we see the following opportunities:

- Index/ ETF opportunities – The stimulus is aimed at reviving broad based growth, that should “lift all boats” – this is an easy opportunity with adequate diversification. Key stops on the HSCEI at 6950-7000 and 31.5-32 for KWEB.

- Sector Specific Opportunities – We see initial opportunities in China Tech, exporters and eventually domestic consumption sectors. Tech has been impacted by policy uncertainty while consumption has been held back since covid – so these become the most natural mean reversion opportunity. Exporters are doing particularly well, especially in the EV space.

- Relative Trades – Pairing China longs with shorts in either India, or broader EM or even the SPX, all look attractively positioned.

First Up, Price Action – If It’s Real, It Ain't Late

Both onshore and offshore equities have rebounded sharply, rallying 13% and 22% respectively from recent lows (mid-Sep 2024). Pullbacks/ consolidation are likely. More importantly, we need to look at this in the context of a decline of over 55% (HSCEI) and of over 25% (Shcomp), since early 2021, and over 65% underperformance vs. SPX and over 70% vs. India (both since early 2021) – as such, should the stimulus unlock growth, the move thus far is only the beginning, and hence far from late. The breakout, in absolute and relative terms both, is holding for now and directionally, any pullbacks will be opportunities to enter longs. Given the risk of another false down, we would urge index level stops at 6950-7000.

source: Tradingview.com

What Ails China Equities

While the “why China” is a shorter list, it’s important to contextualize why investor positioning has been extremely light in China. In one sentence, everything that could go wrong, did – policy uncertainty driving weaker corporate profitability, driving unemployment driving consumption weakness driving deflationary pressures – and the vicious circle repeats. The monetary stimulus aims to break this vicious circle and while the jury is out, the market clearly believes, this is the one that acts as the circuit breaker.

Policy Uncertainty

- Focus on “common prosperity” has often come at the expense of private enterprise

- Unclear re-opening strategies post COVID

Weak Industrial Profits/ Lack of Investment

- Investments, both foreign and domestic, a key plank of economic growth in China, has clearly been impacted by policy uncertainty

- Industrial profits are down c18%y/y in Aug'24.

- Loan growth has consequently also seen a downward trajectory.

source: Tradingeconomics.com

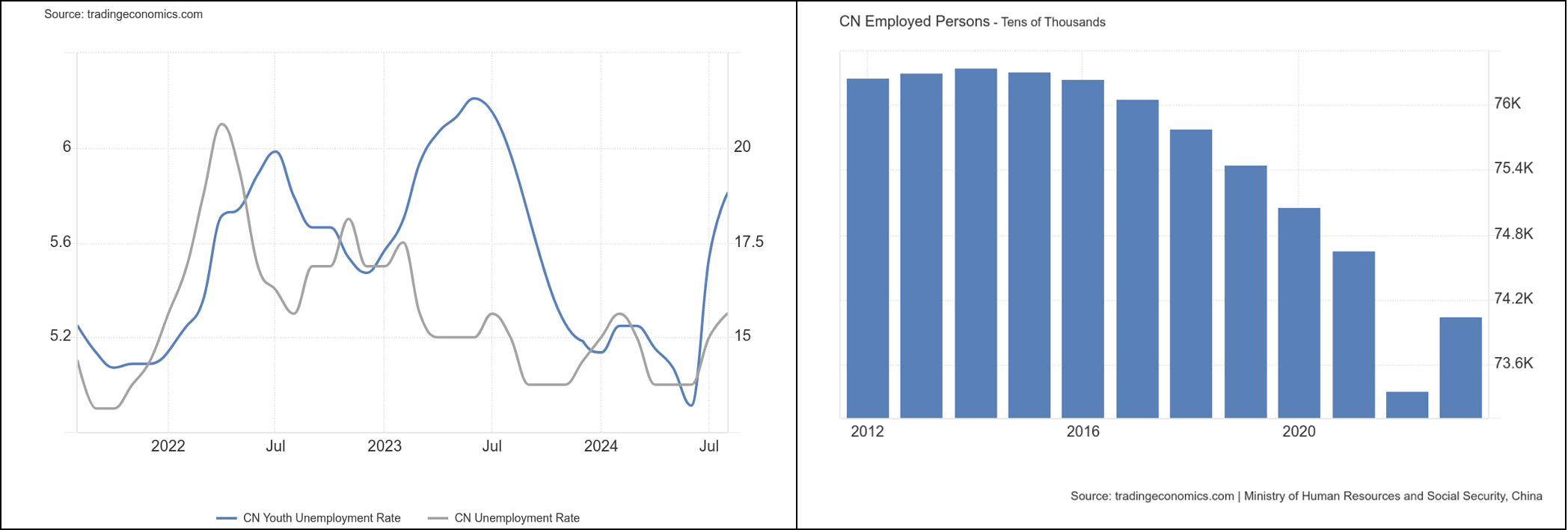

Jobs Weakness

- Faced with policy uncertainty and weakening industrial profits, job creation has lagged

source: Tradingeconomics.com

Weak Consumption & Housing

- Both a factor of jobs weakness as well as an uncertain policy backdrop, consumption has fallen sharply

- A combination of excess supply and weak consumer confidence has driven substantial weakness in housing and the property sector.

Deflationary Pressures

- Both producer and consumer inflation have been negative/ treading water for some time now, even as the developed world grappled for a couple of years with run-away inflation.

- We see deflationary pressures as a fallout of weak business and consumer confidence, but the environment becomes self-reinforcing.

.png)

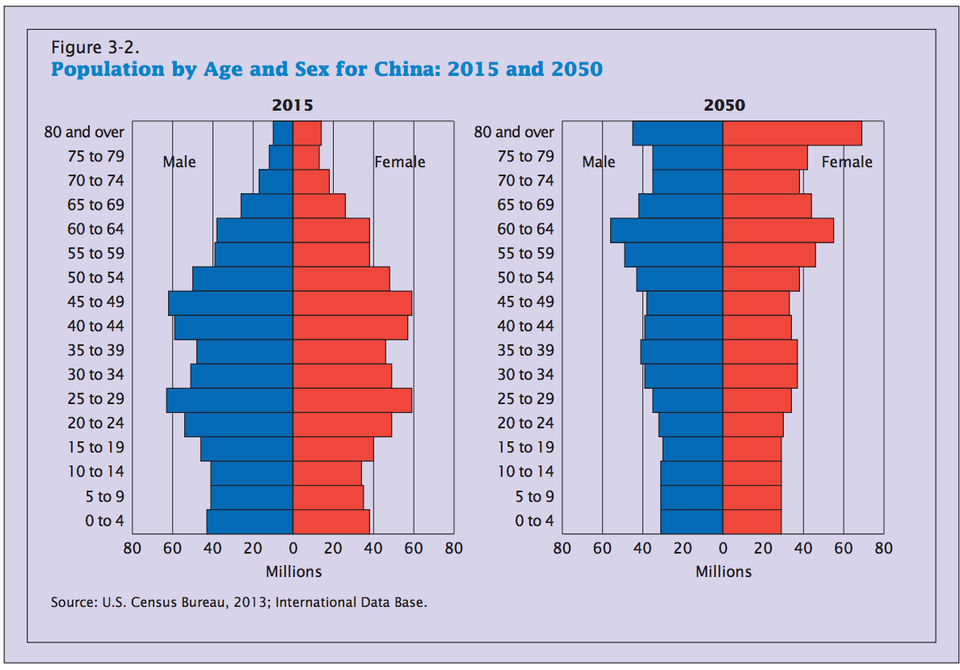

Long Term Issues – Debt and Demographics

- Unsustainable debt (aggregate at c300%) is likely to provide a future growth headwind

- Demographics - with an ageing population and in decline in aggregate, is a long-term headwind.

Is There a Bright Spot?

- Export growth has held up relatively strongly, despite trade barriers. This could however change should the developed world head into a slowdown

- EV exports – Boasting a top two positioning amongst EV manufacturers, China companies have deliver strong exports in the EV segment

Positioning Opportunities - Absolute Trades

Given the near vertical rise, and stretched oscillator positioning, a likely pause/ pullback is likely. Long positions can be protected with stops in the 6950-7000 area for the HSCEI and 31.5-32 for KWEB. Next resistance is in the 7800 area for HSCEI and 36 for KWEB.

source: Tradingview.com

Positioning Opportunities - Relative Opportunities - vs. India and vs. SPX

HSCEI's underperformance vs. Nifty and SPX, partially erased since PBOC's announcements, has headroom of over 10% pts vs. Nifty and of over 3.5%pts vs. SPX. As noted before, a breather is likely before the next move up, given stretched oscillator positioning.

source: Tradingview.com

All investments carry risk, for more important information please read this disclaimer.

%20(16).png)

.png)

.png)