Bearish narratives have to feel challenged by major US equity indices breaking new high ground. Whether driven by the absence of disaster scenarios or growth expectations, the fact of price action cannot be ignored. More importantly though, this breakout needs to sustain - ultimately price and fundamentals need to converge - either growth and earnings expectations are too pessimistic or price action will be negated - this divergence needs resolution.

As with any successful rocket launch, the upward thrust (in this case price) needs to be more than the force of gravity and air resistance (in this case fundamentals) - we surely have a launch, but whether this becomes a successful liftoff, needs confirmation. As such, rather than abandon caution, we remain advocates of using low volatility to have partial hedges in place in equities. Treasuries mostly better than corporate bonds (except European Financials) and fresh positions in gold will have to wait.

From a macro perspective, economic growth has a slowdown hue, albeit not recessionary. While tariffs threaten growth more than inflation, in our view, for now there is too much uncertainty on the direction and level of tariffs in itself, so assessing the impact, a second order effect, becomes that much more elusive. Likewise on corporate earnings - after a consensus beating 13% first quarter, 2Q’25 outlook is sombre with consensus expecting a modest 5% earnings growth and a weaker showing for the second half as well. We suspect this is a low bar to beat and its macro uncertainty that has driven estimates down, rather than actual data. Valuations are back to being expensive, but they themselves aren’t a catalyst. From a fundamental outlook perspective, it would appear that markets have gotten ahead of themselves - but what can go right?

What Can Go Right?

source: Lighthouse Canton

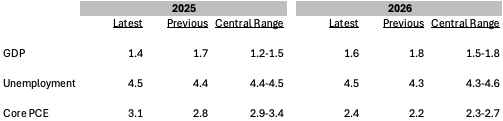

Fed Forecasts - Tempered Growth and Slightly Higher Unemployment

source: FED

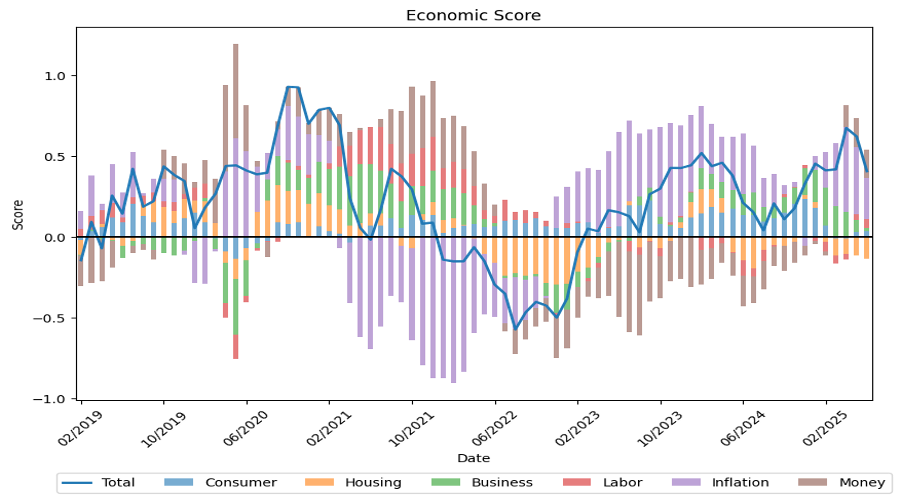

Lighthouse Canton Econ Model Shows Moderation in Progress

source: Lighthouse Canton

Consensus Estimates for 2Q'25 are Modest at 5%

source: Factset

...even as estimates for the full year continue to get revised down

source: Factset

Price Action - SPX Breakout - BUT Not Confirmed. Trend and Momentum Indicators supportive - but stretched

source: Trading View

Sentiment Indicators are not at Extremes

source: CNN

%20(16).png)

.png)