Executive Summary

A quiet but highly consequential trend is reshaping the global tyre industry: the steady migration toward larger rim sizes (18–22 inches) across passenger vehicles. What began as a by-product of SUV penetration has now been reinforced and accelerated by the rise of electric vehicles (EVs).

This migration is structurally margin-accretive for tyre manufacturers. Larger-diameter tyres command higher prices, involve more complex engineering, and exhibit lower price elasticity, allowing manufacturers to expand gross margins even in periods of weaker volumes.

The EV transition brings additional complexity: heavier vehicles, higher instantaneous torque, stricter rolling-resistance requirements, noise constraints, and packaging geometry that often necessitates bigger rims and bespoke EV tyre designs. As automakers increasingly produce EVs with18–21" wheels, the mix shift is feeding directly into tyre companies’ P&Ls through higher ASPs, richer replacement cycles, and product differentiation. Further, our discussions with industry experts corroborate these findings.

This publication analyses the engineering forces behind this trend, outlines why the economics skew positively toward tyre companies, and highlights global and Chinese players best positioned to benefit.

1. Engineering Drivers Behind the Move to Larger Rim Sizes

Understanding the tyre mix shift requires understanding the engineering realities of modern EVs and SUVs. The EV drivetrain and chassis architecture fundamentally alter tyre requirements.

1.1 The Battery Pack and Vehicle Packaging

Most EVs today use a skateboard-style battery pack integrated into the floor. This creates three structural effects:

- Higher ride height because of the vertical thickness of the battery pack.

- Different suspension geometry, requiring larger wheel arches.

- Preference for large-diameter wheels to maintain handling performance and design profile.

Put simply: to accommodate battery-pack architecture while maintaining vehicle dynamics, many EVs default to 18–21" rims.

1.2 Higher Vehicle Mass → Higher Load Index Tyres

EVs are typically 20–30% heavier than equivalent ICE models because the battery pack can weigh 300–700 kg.

Heavier vehicles require tyres with:

- Higher load index

- Stronger carcass and bead materials

- Reinforced sidewalls

- Larger rim diameters to distribute forces more effectively

This pushes manufacturers to develop EV-specific tyres with higher structural rigidity, often paired with larger diameter wheels and lower-profile sidewalls.

1.3 EV Torque Characteristics: Instantaneous, High Output

Electric motors deliver maximum torque from zero RPM, creating:

- Higher shear stress on tyre tread blocks

- Faster wear potential

- The need for tread compounds that balance grip, rolling resistance, and longevity

- Preference for wider, larger-diameter tyre formats

This torque behaviour favours ultra-high performance (UHP) or high-rim-diameter designs, even for mass-market EVs.

1.4 Rolling Resistance and Range Sensitivity

EV range is highly sensitive to tyre rolling resistance. Reducing rolling drag by even 10% can add:

- ~3–4% more driving range on a typical EV

To achieve low rolling resistance, manufacturers use:

- Larger-diameter tyres with narrower sidewalls

- Stiffer internal structures

- Advanced silica and polymer compounds

- Aerodynamically optimised design (large wheels improve airflow when paired with low-profile tyres)

The net result is a propensity for larger rim sizes paired with low rolling resistance technology.

1.5 Noise Constraints: The EV Quietness Penalty

EVs lack engine noise, making road roar and tyre noise extremely noticeable. To reduce cabin noise, EV tyres increasingly use:

- Acoustic foam inserts

- Pattern optimisation

- Tread-block sequencing

- Sidewall harmonics dampening

These technologies scale naturally with premium, large-rim tyres, improving ASPs further.

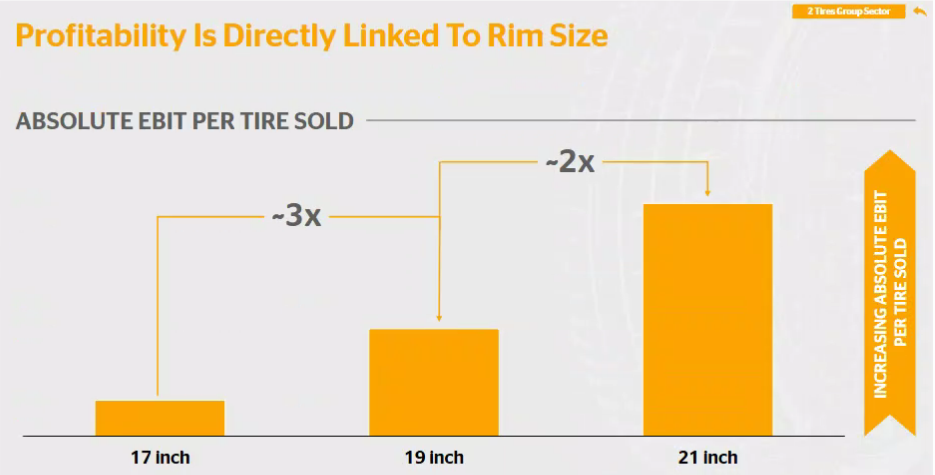

2.Why Larger Rim Sizes Drive Better Economics for Tyre Companies

The tyre industry benefits from this mix shift in three powerful ways: pricing, mix, and technical complexity.

2.1 Larger Rims Command Higher ASPs

A typical 19–21" tyre can be priced 1.6–2.0xhigher than a 15–16" tyre.

Even controlling for raw materials, larger tyres incorporate:

- More rubber and steel

- Higher load and speed ratings

- More complex construction

- EV-tuned compounds and noise-reducing elements

This translates directly to higher gross margins.

2.2 EV Tyres Create a Premium Tier

EV-specific tyres tend to be priced at a premium to standard tyres, because they must balance four competing factors:

- Load capacity

- Wear resistance

- Rolling resistance

- Noise reduction

This allows manufacturers to build a “High Value” segment—similar to Pirelli’s strategy—that consistently prints mid-teens margins.

2.3 Replacement Market Economics Improve

Most EVs ship with large wheels from the factory. When replacement time comes, consumers generally stick to:

- The same rim size

- The same load index

- The same EV-specific requirements

- Often the same brand or OE-approved pattern

This locks in higher-value replacement cycles, which are the profit engine of the tyre industry.

2.4 EV Tyres Wear Faster → Higher Volume Turnover

Due to higher torque and mass, EV tyres often wear 10–20% faster than ICE tyres.

This increases:

- Replacement frequency

- Total lifetime tyre spend per vehicle

- Volume predictability for large-rim segments

3. Investment Implications: Who Benefits?

Tyre manufacturers with strong positions in 18–22" sizes, UHP products, and EV-specific lines will disproportionately win.

Below are the most attractive players globally and in China.

4.Global Winners

4.1 Pirelli (PIRC IM)

Purest global play on ≥18" and EV-specialised tyres

- “High Value” tyres (≥18") make up the majority of revenue.

- Strong EV positioning with hundreds of EV OE homologations.

- Mid-teens EBIT margins, helped by premium mix.

- Most directly levered to the same mix dynamics as luxury EVs and premium SUVs.

4.2 Michelin (ML FP)

Balanced compounder with strong mix tailwinds

- High-rim and UHP tyres drive a meaningful share of profit.

- Consistently maintains strong margins via price/mix discipline.

- Very diversified (aviation, mining, specialty), offering downside protection.

4.3 Bridgestone (5108 JP)

Large-rim segment explicitly identified as structural growth driver

- Strong position in North America—the world’s largest SUV-heavy market.

- Clear portfolio shift toward premium, high-rim-diameter tyres.

4.4 Continental (CON GY – Tyre Division)

OEM-heavy, high-tech tyre business benefiting from EV fitments

- Significant presence in premium German OEMs (BMW, Mercedes, Audi).

- High-value replacement market opportunity.

- Potential strategic unlocking of tyre division value over time.

4.5 Hankook – EV-specialist products climbing the value ladder

Why it’s interesting:

- Aggressively pushing the iON EV tyre line (summer, all-season, winter) with technology explicitly aimed at:

- High load support

- Managing EV torque

- Low rolling resistance and low noise.

- High exposure to mid-to-large rim sizes on premium Asian and European EVs, especially as Korean OEMs (Hyundai/Kia/Genesis) and some European brands scale EV offerings.

EV angle:

More of a rising challenger – not as premium as Michelin/Pirelli yet, but the strategy is to ride the EV/large-rim trend to migrate the brand up the value curve.

5. Chinese Winners

China is crucial because its EV export wave is disproportionately driving global demand for 18–21" tyres.

5.1 Sailun Group (601058 CH)

Fastest-growing Chinese play on EV-specific tyres

- Produces the ERANGE EV line with advanced compound technology.

- Strong penetration into 18–22" rim sizes.

- Moving aggressively into mid-to-premium positioning.

5.2 Zhongce Rubber (603049 CH)

China’s largest tyre manufacturer with a rising EV-UHP portfolio

- Launching EV-ready UHP tyres under Westlake and Goodride.

- Strong export positioning as Chinese EVs penetrate global markets.

Conclusion

The transition toward bigger tyres and larger rim sizes is one of the most powerful and underappreciated structural shifts in the global automotive supply chain.

This trend is being driven not by consumer fashion but by engineering necessity:

- Battery-pack architecture

- Higher vehicle mass

- Instantaneous EV torque

- Rolling resistance and range optimisation

- Noise and comfort constraints

These dynamics make larger-diameter, high-performance, EV-optimised tyres a multi-year profit tailwind for the industry.

The winners will be tyre manufacturers with:

- High exposure to ≥18" rim sizes,

- Strong EV-specific technical capabilities,

- Premium brand positioning, and

- Robust global replacement channels.

In an industry with structurally low volume growth, this mix-driven transformation is one of the clearest long-term margin expansion opportunities, which in turn should lead to strong double digit earnings growth.

.png)

%20(14).png)

.png)