How Three Converging Forces Are Repricing Global Credit Risk

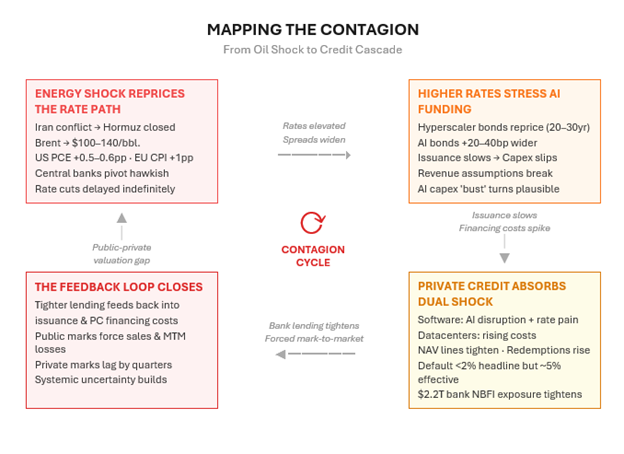

Global credit markets are being reshaped by three forces that, viewed individually, are each significant—but viewed together constitute the most dangerous cocktail for credit investors since 2007–08. The first ingredient is the largest corporate debt-financing cycle in history: over USD 120 billion of hyperscaler bonds issued in a single year, with potentially USD 1.5 trillion more to come, to fund an AI infrastructure buildout consuming nearly 100% of free cash flow. The second is a private credit ecosystem—now USD 3 trillion and systemically intertwined with banks and insurance—carrying concentrated software exposure precisely as AI disrupts those borrowers' business models, while simultaneously absorbing hundreds of billions in data-centre project debt. The third is a live geopolitical shock: the Middle East conflict that erupted in late February 2026, driving oil up, threatening Strait of Hormuz transit (if sustained could prove fatal for the credit markets), and forcing central banks away from the rate cuts that both the AI capex cycle and the private credit refinancing wall desperately need. None of these is a standalone risk. Each one intensifies the others. Together, they create a self-reinforcing repricing loop across investment-grade, high-yield, private credit, and emerging markets simultaneously. This note maps that loop.

Portfolios can reduce the impact by reassessing the correlation within its constituents, focusing on liquidity terms, while being nimble to exploit the dispersions within and all these while maintaining geographic diversification.

To understand why credit markets are repricing, it is essential to see the three forces not as parallel risks but as a single feedback loop.

This is not a sequential chain—it is a simultaneous, multi-directional stress. The Middle East conflict does not merely add to AI credit risk or private credit risk; it is the accelerant that transforms both from forward-looking concerns into a present-tense repricing event. Each force, left alone, might be manageable. Combined, they produce correlated drawdowns across segments that portfolios were designed to treat as diversified.

Ingredient 1: The AI Capex Debt Machine

Addressing the first ingredient in detail, we have the five largest hyperscalers—Amazon, Alphabet, Meta, Microsoft and Oracle—collectively issued roughly USD 121 billion of bonds in 2025, a multi-fold increase from the USD 28 billion annual average of 2020–24. Credit Sights now projects their aggregate capex at approximately USD 750 billion for 2026, with 75% allocated to AI infrastructure. Capital intensity ratios have surged to 45–57% of revenue—levels previously associated with industrial utilities, not technology firms—and aggregate capex now consumes close to 94–100% of operating cash flows after dividends and buybacks.

This means the AI buildout is now structurally dependent on external debt markets. Morgan Stanley and JPMorgan project the technology sector may need to issue as much as USD 1.5 trillion over the coming years. Bank of America notes the Big Five hyperscalers are on pace to match the Big Six banks' average annual issuance of USD 157 billion—a development that would fundamentally reshape the composition of global investment-grade indices.

This debt dependency collides directly with the Middle East conflict. Prior to the February 2026 escalation, consensus expected the Federal Reserve to begin cutting rates in spring 2026—a benign backdrop for absorbing massive tech supply. That narrative has been shattered. Oil's surge is projected to add 0.5–0.6 percentage points to U.S. headline PCE inflation (Goldman Sachs), potentially pushing it back above 3%. Sustainably elevated oil prices could prove to be fatal for the credit markets. The ECB faces what ING has termed a 'genuine dilemma': energy-driven inflation versus weakening growth. Asian central banks in Malaysia, the Philippines and Indonesia are pausing or reversing easing.

For hyperscaler issuers, this means the cost of the AI buildout is rising in real-time. New-issue concessions for AI bonds were already averaging approximately 12 basis points—nearly five times the 2.5 bp average for the broader IG market—before the conflict. With risk appetite now contracting further, future jumbo deals face even wider concessions, potential issuance delays, or both. Any slowdown in the pace of debt funding directly threatens the capex timelines that underpin these companies' AI revenue projections.

The market is already differentiating sharply within the hyperscaler complex. Oracle's five-year CDS has more than tripled since September 2025 to levels last observed around the 2008 financial crisis, reflecting negative free cash flow projections through 2029 and concentrated customer risk. Meta's bond yields have risen approximately 30 basis points year-to-date despite stable ratings. Meanwhile, Alphabet and Amazon have widened only modestly (~10 bp), reflecting stronger free-cash-flow profiles and greater capacity to self-fund.

This dispersion is instructive: The market is not rejecting AI credit broadly but is punishing issuers whose leverage trajectories assumed continued access to cheap, plentiful debt. The Middle East conflict, by threatening to keep that debt expensive and scarce, turns what was a company-specific concern (Oracle) into a systemic question about the entire AI capex funding model.

Ingredient 2: Private Credit at the Intersection

Moving to the second ingredient, Private credit, originating out of the west, is the segment where the AI capex cycle and the geopolitical shock concentrate their combined damage most acutely. The USD 3 trillion private credit market sits at the intersection of both forces (with the exception of Asia): it is simultaneously a major funder of AI data-centre infrastructure and the largest lender to the software sector that AI is disrupting—and it is doing both under financial conditions that the Middle East conflict is actively worsening.

The Software Squeeze: AI Disruption Meets Rate Pain

Software and services account for roughly 17–20% of private credit and BDC portfolios by deal count, making it the single largest sector bucket. Within this, stress is concentrated in unprofitable or slow-growth names that borrowed at peak 2021–22 valuations via growth debt or PIK-heavy structures. These borrowers face a two-front assault: AI tools are eroding their business models while higher-for-longer rates—now locked in by the energy shock—make refinancing into 2026–27 progressively more punitive.

UBS has warned that in an aggressive AI disruption scenario, default rates in U.S. private credit could climb to 13%, meaningfully above the stress projected for leveraged loans (~8%) and high-yield bonds (~4%). More broadly, private credit defaults are expected to increase by as much as 3% points in 2026, outpacing other credit segments. The IMF's 2025 Financial Stability Report found that approximately 40% of private credit borrowers have negative free cash flow, up from 25% in 2021. Payment-in-kind usage—a leading indicator of liquidity strain—has risen to roughly 8% of BDC investment income.

The Middle East conflict intensifies every dimension of this stress. By keeping central banks on hold or hawkish, it ensures the rate relief that leveraged software borrowers need will not arrive in time. By widening risk premia, it raises the spreads these borrowers must pay to refinance. And by triggering risk-off flows, it tightens the subscription lines and NAV facilities that private credit vehicles rely on for liquidity.

The other side of the intersection is the rapid growth of AI data-centre financing within private credit itself. Projected AI infrastructure capex of several trillion dollars through 2030 has drawn private lenders into large-ticket, long-duration structured financings—joint ventures, sale-leasebacks and bespoke project finance—that banks are less willing to underwrite in size. Estimates suggest nearly USD 200 billion of total debt was raised for data-centre development in 2025, including transactions exceeding USD 10 billion, such as the approximately USD 27 billion Meta–Blue Owl joint venture.

While these structures typically carry asset backing and long-dated contracts, they embed meaningful construction risk, technology-obsolescence risk and counterparty concentration. If AI capex expectations moderate—whether because hyperscaler revenues disappoint, because geopolitical uncertainty delays buildout timelines, or because higher rates change the project economics—spreads on these structured deals could gap wider. Some projects may be delayed or resized entirely. The same conflict-driven macro environment that pressures software borrowers simultaneously threatens the data-centre project pipeline that was supposed to be private credit's next growth engine.

The Correlation Trap

Here lies the cocktail's most dangerous property: the same macro driver—a combination of elevated rates, slowing growth and heightened risk aversion, all amplified by the geopolitical shock—hits software loans, AI data-centre project debt, listed tech credit and broader high-yield/EM beta at the same time. Portfolios that believed were diversified across 'tech credit, private lending, infrastructure' and 'EM' discover that under stress, these exposures behave as a single high-beta factor. What was thought as diversification becomes concentration.

How Should Portfolios Be Positioned to Face the Storm?

- Rethink Correlation Assumptions

Stress testing must assume materially higher cross-bucket correlations—between private direct lending, listed BDCs, high-yield technology, EM high-yield and infrastructure debt—under combined macro-plus-geopolitics scenarios. Historical diversification assumptions built on single-shock models are inadequate for an environment where rates, AI capex risk and geopolitical premia move together. The three-ingredient cocktail demands a three-shock stress test. - Monitor the Cluster, Not the Silos

Portfolios overweight in software private credit, technology high-yield, BDCs and AI infrastructure should be monitored as a single correlated cluster. The war amplifies the correlation between these exposures; in a sustained conflict scenario, they behave as one high-beta factor rather than as independent allocations. Concentration limits should be applied to the cluster as a whole, not to each silo individually. - Tiering Liquidity is Now Urgent

Distinguish between daily-liquid listed credit (high-yield, EM, BDCs) and locked-up private vehicles. In the current environment, public marks move first and force sales, while private marks lag—potentially for quarters. This gap is not merely an accounting inconvenience; it is a source of forced selling, redemption pressure and systemic uncertainty. Portfolios with significant illiquid private credit exposure alongside liquid HY and EM positions face the risk that the liquid book is sold to meet redemptions, concentrating the remaining portfolio in precisely the illiquid exposures that are most at risk. - Exploit the Dispersion

The cocktail creates losers but also relative-value opportunities. Within the hyperscaler complex, the spread between Oracle (debt-dependent, rate-sensitive) and Alphabet (strong FCF, modest widening) has blown out and may offer pair-trade opportunities for fundamental credit analysts. Across the curve, the concentration of AI issuance at the 20–30-year point creates specific curve dynamics; intermediate maturities may offer better risk-adjusted value where supply pressure is lower. In EM, differentiation between commodity exporters (benefiting from oil) and importers (suffering from inflation) creates alpha potential—but only for investors who are actively managing the geopolitical dimension rather than passively absorbing it. - Build Explicit Geopolitical Hedges

The Middle East conflict underscores the need for explicit geopolitical risk budgets within credit portfolios. Energy-sector CDS, inflation-linked instruments and oil-price options may be warranted for portfolios with significant long-duration IG or EM exposure. More broadly, investors should demand higher compensation for any credit exposure whose refinancing or revenue assumptions implicitly require a benign rate environment—because the conflict has made that assumption unreliable.

Conclusion: The Cocktail is Already Mixed

The three forces examined in this note are not three separate risks. They are one risk, expressing themselves through three channels. The AI capex cycle creates the leverage. Private credit creates the fragility. The Middle East conflict creates the catalyst. Remove any one of the three, and the credit market is stressed but manageable: without the AI buildout, private credit faces a normal-cycle default uptick; without the conflict, hyperscalers can refinance cheaply and buy time; without the private credit nexus, the AI cycle is a contained IG story. But all three are present simultaneously. The leverage, the fragility and the catalyst are interacting in real time, producing a repricing that is broader, faster and more correlated than any single-factor model would predict. For credit investors, the implication is clear: this is not a time for siloed risk management. The portfolio that survives the storm is the one that recognizes these three forces as a single cocktail—and positions for the correlations that cocktail creates, not the diversification that existed before it was mixed.

.png)

%20(14).png)

.png)