Table of Contents

Why the stress gripping Western private credit markets is Asia's structural advantage – and why Asia is built for this moment

Executive Summary

Redemption restrictions at several large Western private credit funds, regulatory scrutiny of portfolio valuations, and IMF warnings on liquidity mismatches have triggered concern across the private markets industry – and redemption enquiries from private banking clients across Hong Kong and Singapore. This publication argues that the stress is not a verdict on private credit as an asset class. It is a verdict on three specific failures: aggressive underwriting in software and SaaS businesses whose repayment assumptions are now broken by AI disruption; structural mismatch between open-ended fund vehicles and illiquid underlying assets; and hidden bank leverage amplifying system-wide risk well beyond what investors were told they held.

None of these failures characterise Asia's private credit market. The region remains structurally differentiated, significantly less crowded, and at the early stage of a multi-year growth cycle that Western markets have already passed through. The question for allocators is not whether private credit is broken. It is whether they are in the right part of it.

Section 01 | The Divergence: Western Overcrowding vs Asia's Structural Opportunity

The roots of the current stress in Western private credit are not primarily about asset quality in isolation. They reflect what happens when too much capital chases too few opportunities in a market that has grown faster than its underwriting discipline can absorb. The global private credit market reached $3.5 trillion in AUM by end-2024, with the US accounting for approximately 65% of that total – implying roughly $2.3 trillion in US private credit alone. Global deployment volumes hit $592.8 billion in 2024, up 78% on the prior year. This pace of growth has consequences.

The contrast with Asia-Pacific is stark. Despite the region contributing nearly two-thirds of global economic growth in 2023, APAC's private credit market accounts for a fraction of regional lending – estimated at only 1.8% of the region's overall credit market even by 2027. Banks still account for approximately 79% of all lending in Asia, compared with just 33% in the US. The APAC market grew from roughly $39 billion in 2020 to $59 billion by 2024 – healthy growth, but from a base where the structural overcrowding, covenant erosion and deployment pressure of Western markets simply have not taken hold.

"The US market has become extremely crowded. Large amounts of capital have entered both public and private assets over the past four to five years. In credit markets – where the upside is capped by the contractual return and the downside in default can be severe – that crowding creates real and lasting problems."

— Sanket Sinha, Managing Director & CEO, Global Asset Management, Lighthouse Canton

That asymmetry is the defining feature of credit investing. A lender cannot participate in equity-like upside if a borrower outperforms. The contractual return is the ceiling. When deployment pressure rises and managers compete for mandates, underwriting standards erode and the asymmetry worsens – precisely at the moment when market conditions appear most benign.

"You inevitably end up picking more losers than you can afford when too much capital is chasing the same opportunities. At that point, deployment pressure begins to take priority over portfolio quality."

The Capital Gulf: US VS Asia-pacific Private Credit AUM (USD BILLIONS)

Single-axis comparison - the scale difference is the story.Both series plotted on the same axis.

Asia: Early Cycle, Full Opportunity Set

Asia-Pacific private credit is entering what industry researchers characterise as a pivotal stage in its evolution – moving from niche alternative to essential component of corporate financing. The forces driving this are structural: ongoing retrenchment by commercial banks toward only the largest borrowers; tighter regulatory oversight consolidating regional lending; and a growing demand for bespoke, flexible capital across a highly fragmented, 50-jurisdiction market where 90% of deals involve borrowers without private equity backing. The region's infrastructure investment gap alone is estimated at $26 trillion through 2030 – a financing need that bank capital cannot fill alone.

A market historically defined by Australia, Japan and India is now broadening into South Korea, Malaysia, Thailand and Southeast Asia. Major global allocators are taking note: KKR recently closed its second Asia private credit fund at $2.5 billion, roughly doubling its prior regional vehicle. Goldman Sachs Asset Management secured a $1 billion mandate from Abu Dhabi's Mubadala to co-invest in APAC private credit. Singapore's Temasek Holdings is now ranked the world's eleventh largest private credit investor with a $22 billion portfolio.

According to Lighthouse Canton's in-house views, spreads in Asia remain approximately 200 to 300 basis points higher than equivalent Western credit. APAC fund selectors are expected to lift private debt allocations from 9% in 2023 to 39% in 2025 – a shift signalling a transition from niche to core allocation. Private wealth investors are forecast to account for 28% of APAC private credit AUM by 2027, up from 23% in 2020. Credit structures in the region remain more conservative: full covenant packages, leverage rarely exceeding 3 times, and lenders retaining meaningful control rights -none of the structural erosion that competition and capital abundance have driven in the West.

"In Asia the structures are still significantly stronger. You are still lending to top borrowers, often with lower levels of leverage. A lot of the challenges today relate to loans extended to sectors such as software where there are limited hard assets backing the debt – and structures are covenant-light. That places Asia in a relatively favourable position."

Section 02 | Issues Western Private Credit Players Are Dealing

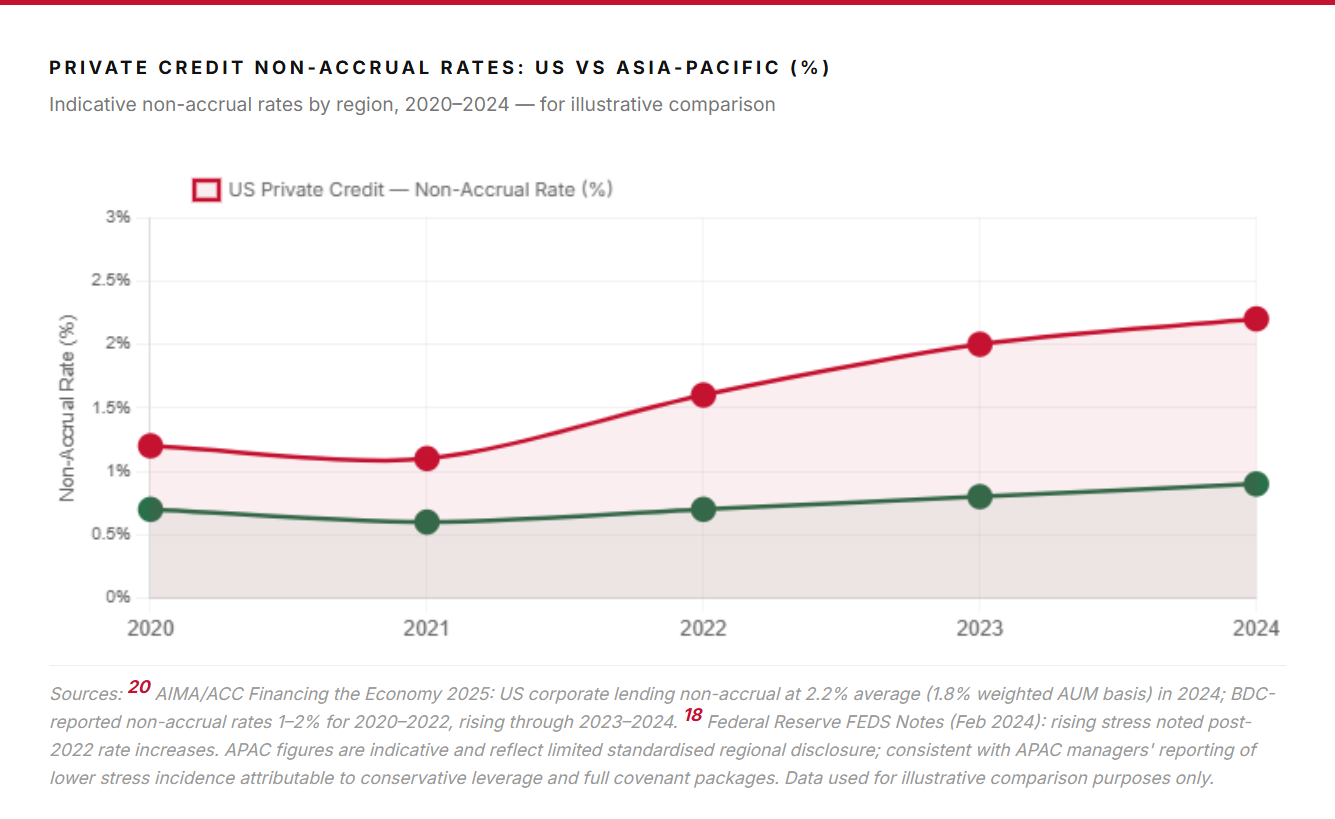

The current period of stress in Western private credit is not the product of a single cause. It reflects three distinct but interconnected structural failures – each rooted in decisions made during the years of abundant capital and compressed risk premiums. Taken together, they explain why the headlines are concentrated in the US and Europe, and why they are unlikely to resolve quickly.

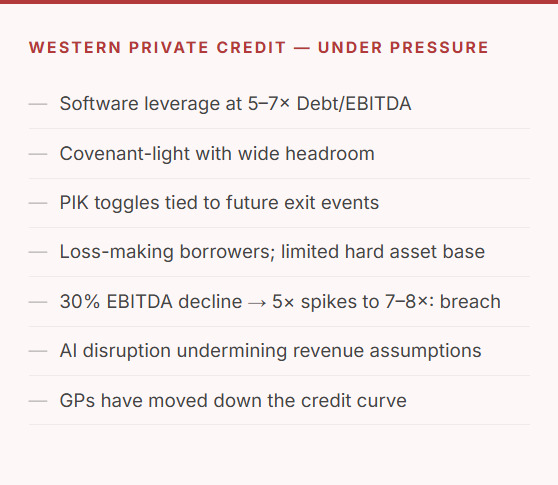

Issue 01 | Software Credit and the AI Disruption

How a decade of aggressive SaaS underwriting meets a structural break

Over the past five years, a significant portion of US and European private credit flowed into software and SaaS companies – businesses whose subscription-based revenue models were believed to provide the predictability required to service high debt loads at leverage multiples frequently exceeding 5 to 7 times EBITDA. Many of these companies secured loans with payment-in-kind (PIK) features, or with repayment mechanisms tied to future IPO events or strategic monetisations. In numerous cases, the borrower was loss-making at the time of financing, with repayment predicated on future equity valuations rather than current operating cash flows.

"The risk emerges when such companies remain loss-making and repayment expectations depend on future valuations rather than current cash flows. With the rapid advance of artificial intelligence beginning to disrupt parts of the software landscape, some of those valuation assumptions are now being fundamentally reassessed by investors and lenders alike."

Generative AI has broken the central underwriting assumption. Entire categories of software are being commoditised or replaced by AI-native alternatives. The net revenue retention rates and churn assumptions embedded in 2021–2023 vintage underwriting models are no longer reliable. When revenue projections are revised downward, leverage ratios that appeared manageable at 5 to 7 times EBITDA spike sharply on a deteriorating EBITDA base. PIK toggles are triggered. What was structured as a stable cash-flow credit has become an equity-risk exposure – sitting inside a debt vehicle with no upside participation.

According to Lighthouse Canton's in-house views, APAC lenders have underwritten software-adjacent companies at conservative leverage – meaning the same EBITDA deterioration leaves credit structures intact and actionable. Asia's private credit focus has remained on mid-market companies with more durable cash flows, more tangible collateral, and considerably less exposure to the AI disruption risk driving concern in Western markets.

"In credit investing, the upside is capped by the contractual return. But in the event of a default, the downside can be significant depending on the level of security and expected recovery."

Issue 02 | Semi-Liquid Fund Gating – Structure, Not Crisis

What actually happened, and why media framing amplified the impact

Much of the recent redemption activity has centred on evergreen, open-ended fund structures – vehicles designed to give investors periodic liquidity, typically quarterly windows of up to 5% of NAV, while investing in fundamentally illiquid private loans with 3 to 5 year maturities. As macro anxiety increased in late 2025 and early 2026, redemption requests clustered and exceeded disclosed quarterly thresholds. Gates were triggered automatically per the funds' prospectuses – not a malfunction or a sign of underlying asset stress, but the structure operating exactly as documented.

"When gates are implemented, the narrative often becomes that the manager cannot meet redemptions. But in reality those provisions were always part of the structure. One headline can quickly create panic – investors begin to assume there is something fundamentally wrong with private credit as an asset class, when the issue is far more specific."

Once gates became public, further redemption requests followed from investors seeking to exit before queues lengthened – a classic run dynamic. The situation is precisely characterised as a product-design constraint meeting investor expectations misalignment, not an asset-quality crisis. Notably, 80% of private credit committed capital globally is held in closed-ended rather than semi-liquid structures – the gating events are concentrated in a specific minority segment of the market, though the headline risk they generate is disproportionate to their structural significance.

"Private credit, infrastructure, and private equity are asset classes best suited to closed-end structures. Any vehicle that tries to paper over the illiquidity constraint will show its limits when tested. Investors earn a premium precisely because they are allocating to assets that are inherently illiquid."

← Scroll to see full table →

| Feature | Semi-Liquid / Evergreen (Affected Structures) | Closed-End Fund (Best Practice) |

|---|---|---|

| Structure | Open-ended / evergreen | Closed-end, fixed fund life |

| Liquidity offered | Quarterly (up to 5% of NAV) | None - capital committed to maturity |

| Gate risk | Triggered when requests exceed threshold | Structurally inapplicable |

| Run dynamic | Possible once gates become public | No mechanism for a run to occur |

| Asset-liability match | Mismatch exposed under stress | Assets and liabilities fully matched |

Issue 03 | Hidden Back-Leverage and Bank Interconnection

The systemic risk that disclosure statements did not adequately convey

A less-discussed but structurally important issue is the degree to which private credit funds in the US and Europe have become dependent on bank-provided leverage to amplify returns. A fund underwrites a corporate loan at 5 to 6 times debt-to-EBITDA, then pledges that loan as collateral with a bank – via a subscription credit facility, NAV facility, or repo line – borrowing against it at 1.3 to 1.5 times. The effective leverage in the system is therefore not the headline 5 to 6 times reported to investors, but closer to 7 to 8 times on the underlying business.

As underlying credit quality has deteriorated, banks have tightened these lines or called them entirely, forcing fund managers to sell assets at distressed prices. Bank loans to private credit intermediaries in the US have doubled from $500 billion in January 2019 to over $1 trillion in January 2024 – creating a direct and growing interconnection between bank balance sheets and private credit portfolio stress. The IMF and Moody's have flagged this as a potential contagion channel: stress in private credit portfolios can now transmit to bank balance sheets, and vice versa.

← Scroll to see full table →

| Leverage Layer | Typical Western Structure | Impact on LP |

|---|---|---|

| Borrower leverage | 5–6× Debt/EBITDA (disclosed) | Base risk layer |

| Fund-level leverage | 1.3–1.5× via NAV/repo lines | Effective leverage → 7–8× on underlying |

| Investor disclosure | Borrower-level only; bank leverage often opaque | LP materially underestimates true system risk |

| Stress transmission | Bank tightening → forced asset sales → losses | Contagion channel to and from bank sector |

Section 03 | What Investors Should Focus On

The current headlines have prompted a binary reaction from some investors – a blanket reassessment of private credit as an asset class. That response conflates structurally different risks operating in different geographies, in different fund structures, with different borrowers. The correct response is more surgical: to evaluate private credit exposure not at the level of geography or headline, but at the level of the individual borrower, the fund structure, the actual leverage in the system.

"LPs need to look beyond country or geographic risk. The real assessment has to be done at the borrower level. That is where quality, security, and the path to repayment are either present or they are not."

← Scroll to see full table →

| Dimension | Key Question | Warning Sign |

|---|---|---|

| Borrower | Is the business cash-flow generative today? What hard assets back the debt? | Loss-making; repayment contingent on future exit events |

| Leverage | What is the actual Debt/EBITDA at borrower and fund level? | Headline 5-6x masking 7-8x effective via NAV/repo lines |

| Covenants | Are full covenant packages in place with meaningful early-trigger protections? | Covenant-light; wide headroom; minimal lender controls |

| Structure | Closed-end or open-ended? Is periodic liquidity offered against illiquid assets? | Evergreen/semi-liquid funds holding 3-5 year illiquid loans |

| Bank Exposure | Are subscription credit, NAV or repo lines used to amplify returns? | Undisclosed bank leverage; forced-sale risk if lines are called |

| Market Stage | Is the geography early or late in its private credit development cycle? | Overcrowded markets; compressed spreads; structural deterioration |

Private credit remains a compelling asset class, offering investors access to a genuine illiquidity premium and the opportunity to benefit from active credit selection in markets where pricing inefficiencies persist. However, realising these benefits demands a clear-eyed understanding of the asset class's defining characteristics. Illiquidity is not a risk to be engineered away – it is the very source of incremental return, and investors must be positioned to honour it. Rigorous credit analysis sits at the core of value creation; without it, yield becomes a mirage. Leverage, when employed thoughtfully and only where the underlying risk profile genuinely justifies it, can enhance outcomes – but it must never be used to compensate for credit weakness or to manufacture returns the assets themselves do not support.

Investors who appreciate these dynamics, and partner with managers who embody them, are best placed to capture what private credit, at its best, has to offer.

References & Sources

1. Alternative Credit Council & Houlihan Lokey. (2025). Financing the economy 2025. AIMA.

2. Alternative Credit Council, Broadridge, EY, & Simmons & Simmons. (2025). Private credit in Asia 2.0. AIMA Alternative Credit Council.

3. OECD. "Emerging Asia Accounts for 60% of Global Economic Growth." Statista, 2025.

4. Equities First. "Private Credit in Asia Isn't Just Getting Bigger, It's Becoming More Diverse." EquitiesFirst.com, 2025.

5. Global Finance Magazine. "Private Credit: Poised For Growth." GFMag.com, February 2026.

6. Sinha, Sanket. "How Is the Geography of Global Capital Shifting in 2026?" Lighthouse Canton Insights, February 3, 2026.

7. Investment Executive. "Global Private Credit Market Reaches US$3.5 Trillion AUM Threshold: Report." InvestmentExecutive.com, December 2025.

8. Board of Governors of the Federal Reserve System (US). "Loans to Nondepository Financial Institutions, All Commercial Banks." Federal Reserve Bank of St. Louis, retrieved March 2026.

Data Notice: All market data, statistics, and numerical figures referenced in this communication have been sourced from publicly available information and third-party estimates. Lighthouse Canton Pte. Ltd. has not independently verified the accuracy, completeness, or timeliness of such data and makes no representation or warranty, express or implied, with respect thereto. Investors should not place undue reliance on these figures and are advised to independently verify all data before making any investment decision. Lighthouse Canton Pte. Ltd. accepts no liability for any loss or damage arising from reliance on such figures.

Disclaimer:The contents of this document are confidential and are meant for the intended recipient only. If you are not the intended recipient, please delete all copies of this document and notify the sender immediately.

This document, provided as a general commentary, is for informational purposes only and is not to be construed as an offer to sell or solicit an offer to buy any financial instruments in any jurisdiction. This does not constitute any form of regulated financial advice, and your independent financial advisor should be consulted prior to taking any investment decision(s). This document is based on information from sources which are reliable but has not been independently verified by Lighthouse Canton Pte. Ltd. or its affiliates ("LC"). LC has taken reasonable steps to verify the contents of this document and accepts no liability for any loss arising from the use of any information contained herein. Please also note that past performances are not indicative of future performance.

Information contained herein are those of the author(s) and does not represent views held by other parties. LC is also under no obligation to update you on any changes made to this document.This document is prepared by Lighthouse Canton Pte. Ltd.and its affiliate company, Lighthouse Canton Capital (DIFC) Pte. Ltd., which are regulated by the Monetary Authority of Singapore ("MAS") and Dubai Financial Services Authority ("DFSA") respectively. The contents of this document and/or other associated documents have not been reviewed by the MAS or the DFSA. The contents of this document may not be reproduced or referenced, either in part or in full, without prior written permission from LC.

This document is only intended for Accredited Investors and/or Professional Clients,as defined by MAS and DFSA respectively.

.png)

%20(14).png)

.png)