Paul Tudor Jones famously said "nothing good happens below the 200 dma" - and we are sitting right on that Knife Edge.

Fourth week into geopolitical strife. Oil is well above $100. Inflation is reigniting. And the Fed is caught between a rock and a hard place - tighten and add to the misery, or risk repeating the '70s mistake of easing into a supply shock.

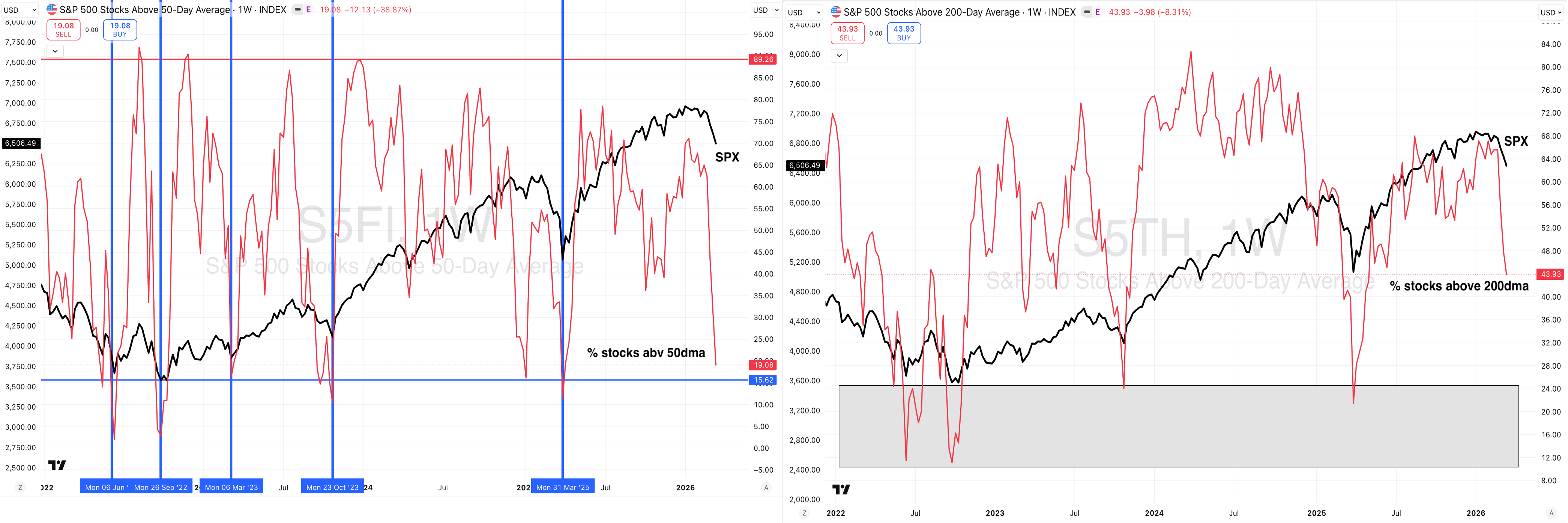

With uncertainty all round, sentiment has deteriorated. Breadth has collapsed. But not quite extreme enough, yet. Even traditional havens such as Gold aren't spared.

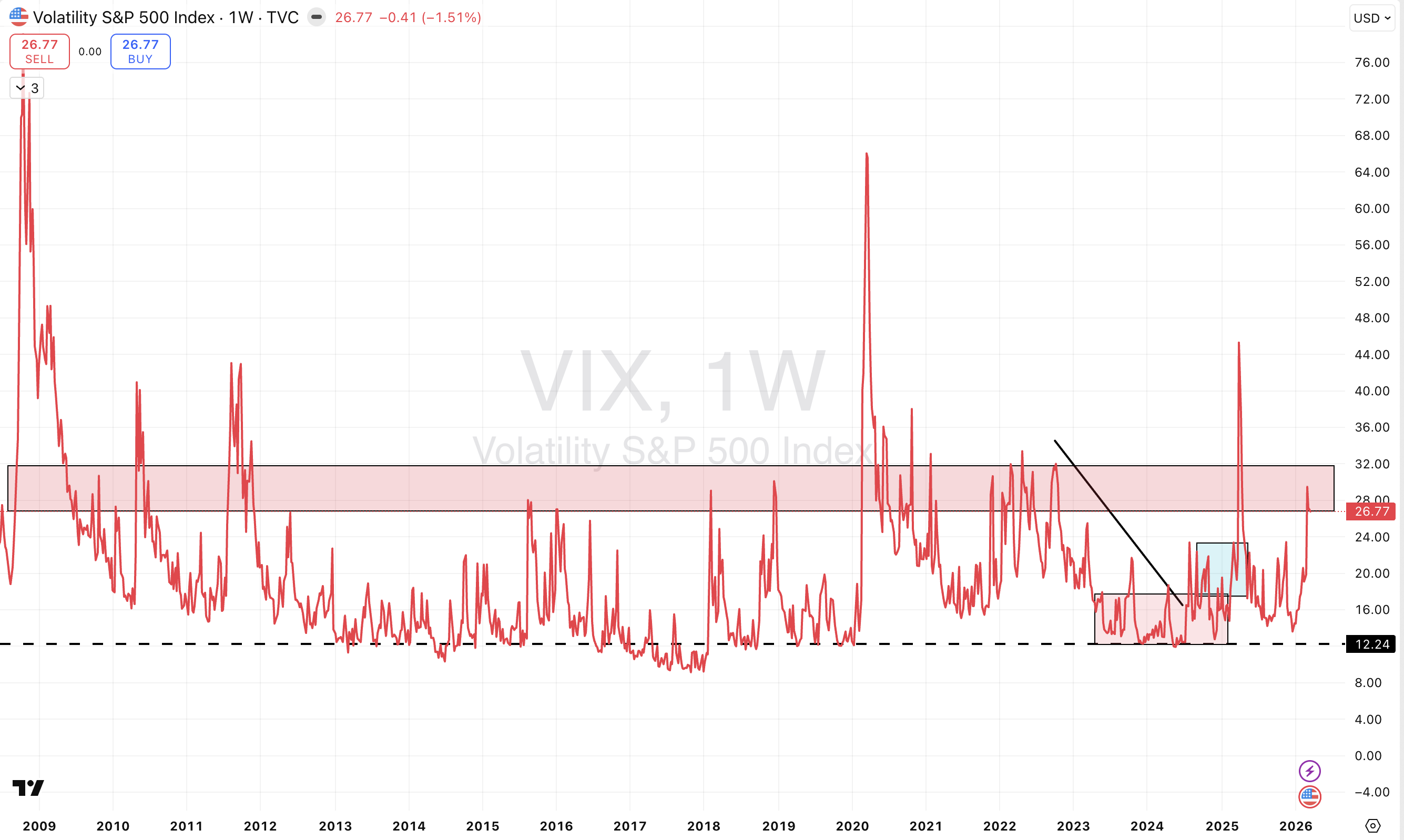

All of this can turn on a dime, and markets can rally viciously from oversold levels, but the risk and bias is to the downside. Aside from the Dollar, the one thing that is elevated is volatility - and that is probably the best opportunity for now.

Positioning:

- Equities: Neutral to underweight. Risk is to the downside until breadth and sentiment reach extremes. US equities positioned better than international equities.

- Bonds: Underweight. Spreads remain expensive and duration is a risk.

- Gold: Attractive via "buy-the-dip" structures, but short-term downside risk to 4200.

- Volatility: Elevated - and that's the opportunity.

The knife edge cuts both ways. Position accordingly.

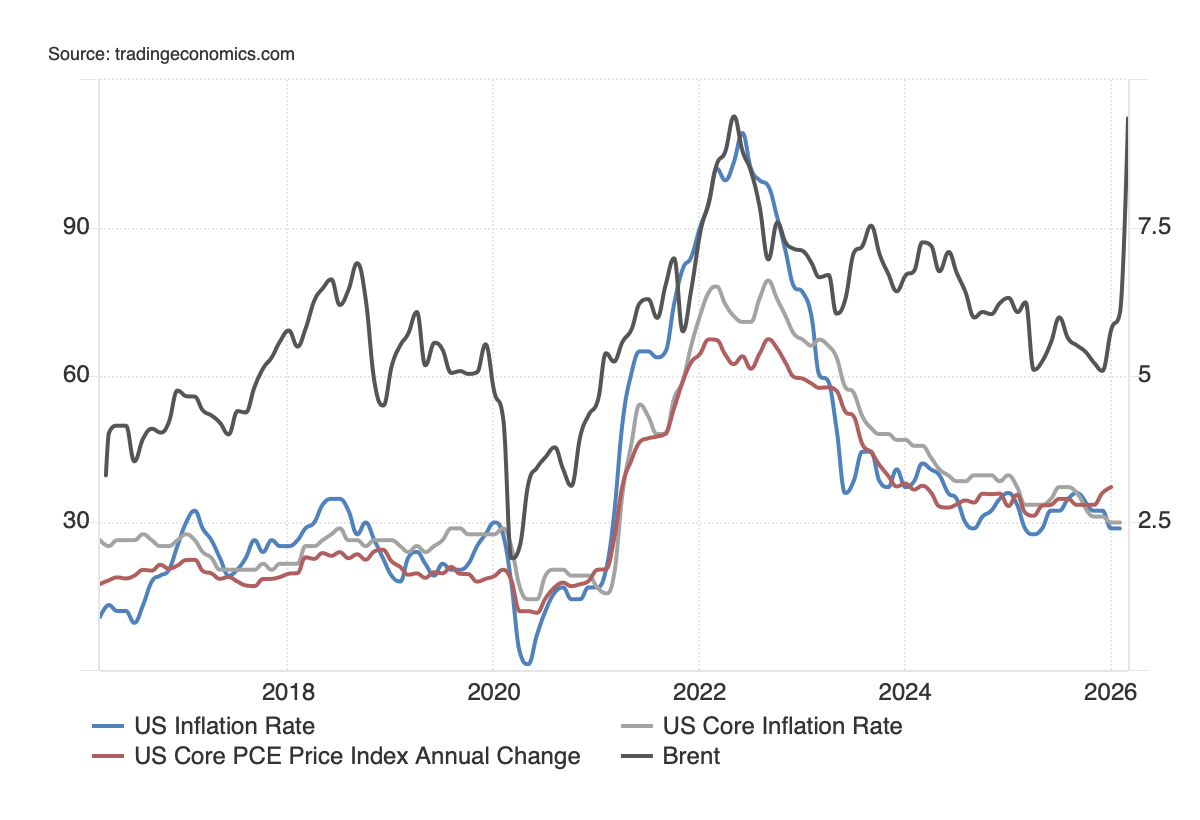

- Oil & Inflation - While central bankers exclude "volatile" energy and food price trends from core measures of inflation, sustained increases in commodity prices feed through into all forms of inflation. While any progress on peace will likely drive a sharp reversal in energy prices, the supply damage will take many months to normalize. Inflation was our number one macro concern at the start of the year, and is absolutely the key variable to watch.

Oil and All forms of Inflation Are Directionally Correlated

source: Trading Economics

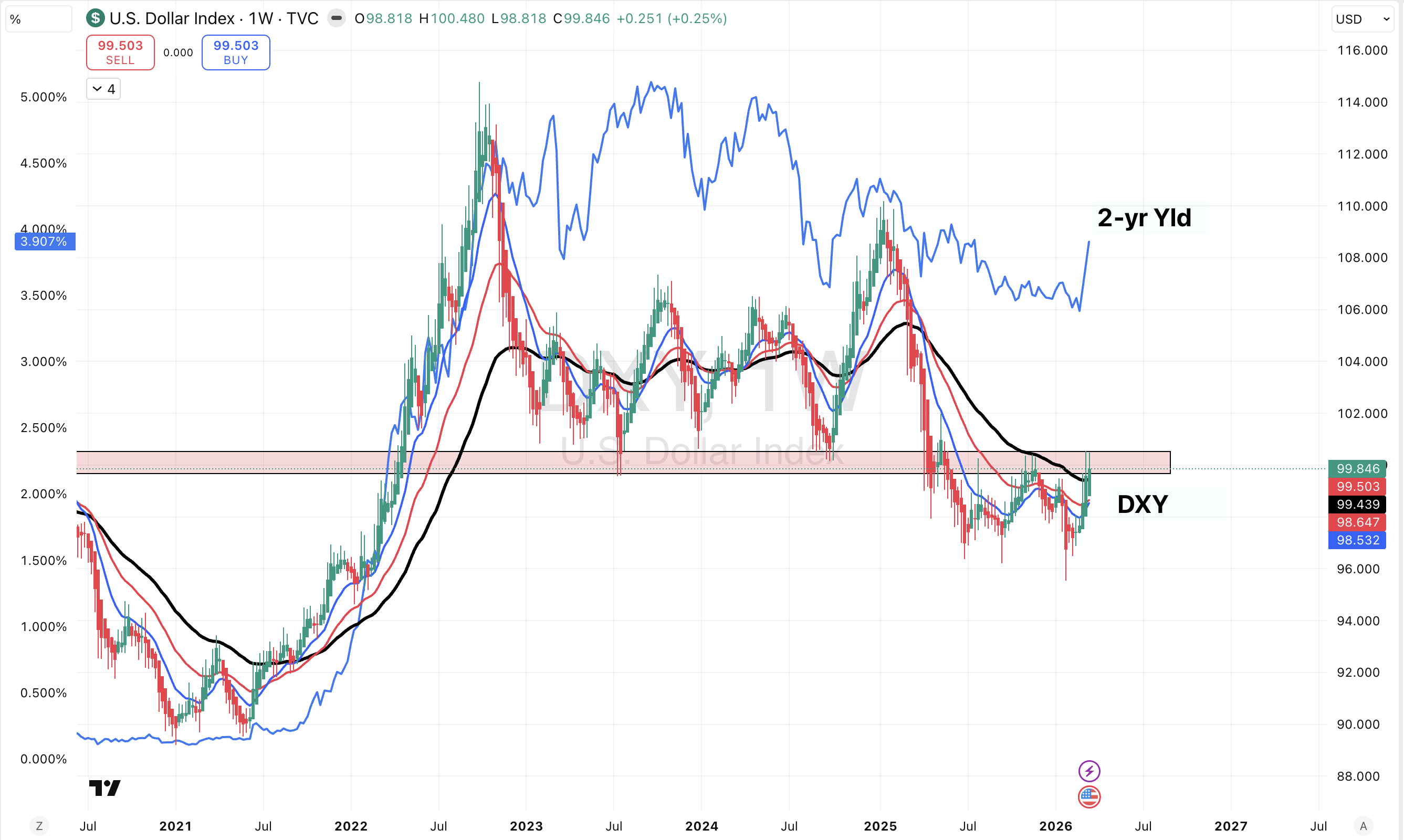

- The Fed's Dilemma - While politicians want lower interest rates, the FED's dilemma - a softer labor market (rising unemployment) and yet sticky inflation, is further exacerbated through trade friction and now the oil shock. With 2-year yields already above the FED Funds rate, a reversal into a tightening cycle (Australia is already on that path) would threaten growth, while any attempt to ease risks the '70s style stagflationary policy mistake.

Rising Interest Rates - What Does The FED Do?

source: Trading View

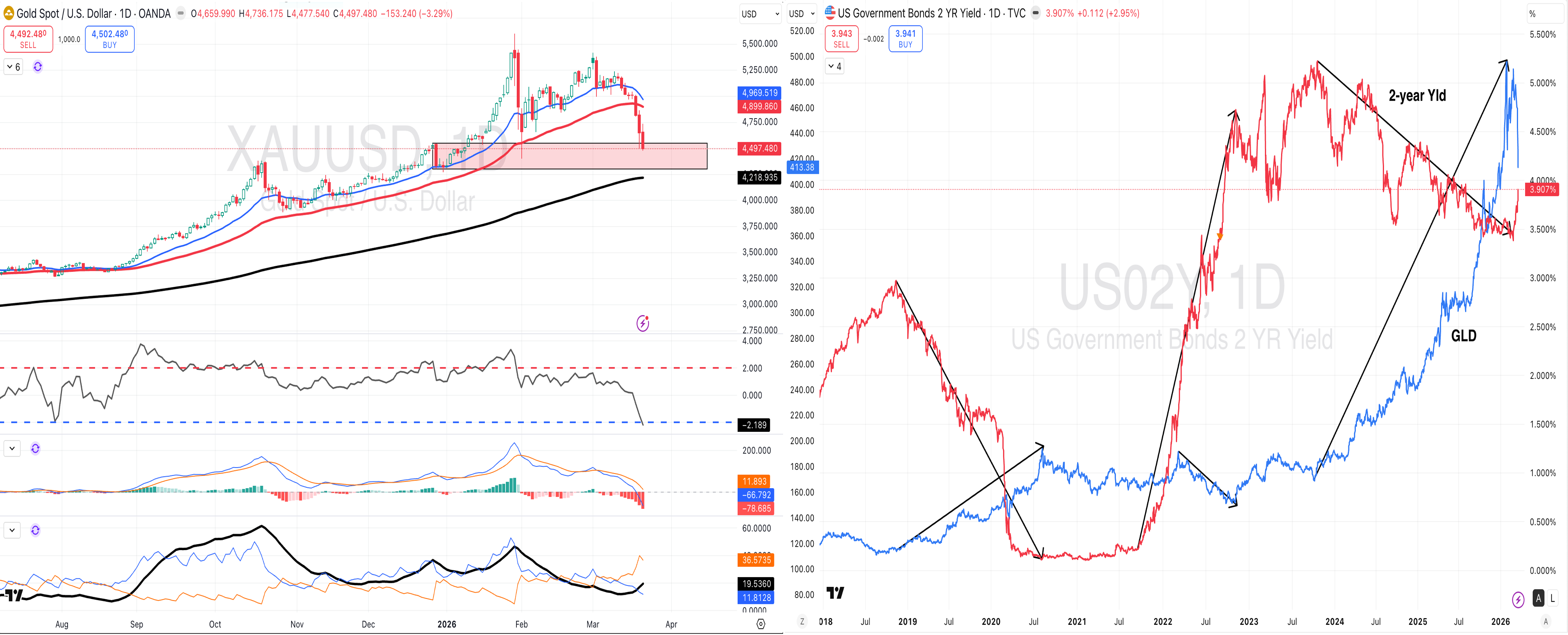

- Gold - A Currency, not an Asset - Many market watchers have been surprised by the sharp decline in precious metals, especially gold - after all, isn't gold supposed to be a "flight to safety haven"? We believe the answer lies in higher interest rates - and as rates rise, all currencies weaken against the dollar - Gold is not immune to this trend. DXY strength, is pervasive for now and while Gold has attractive long-term fundamentals, short-term risks remain to the downside. Sitting in a critical support zone, Gold has downside risk to the 4200 area - however, higher volatility is an opportunity to position through "buy-the-dip" structures.

Gold - Not Immune to Rising Rates; "Buy-The-Dip" structures are attractive

source: Trading View

Higher Yields, Stronger Dollar, Weaker Gold

source: Trading View

- What About Bonds? - While bonds have also retrenched, relative to equities, these have held up reasonably well and surprisingly, more recently, treasuries have suffered more, largely due to their longer duration. While wider spreads (High Yield spreads up 60bp off lows) may appear attractive, these remain low in a historical context. Besides, spiking yields are a risk to duration trades and spreads. We have been, and remain underweight bonds.

Bonds - Spreads Have Widened - BUT- Remain Expensive

source: Trading View

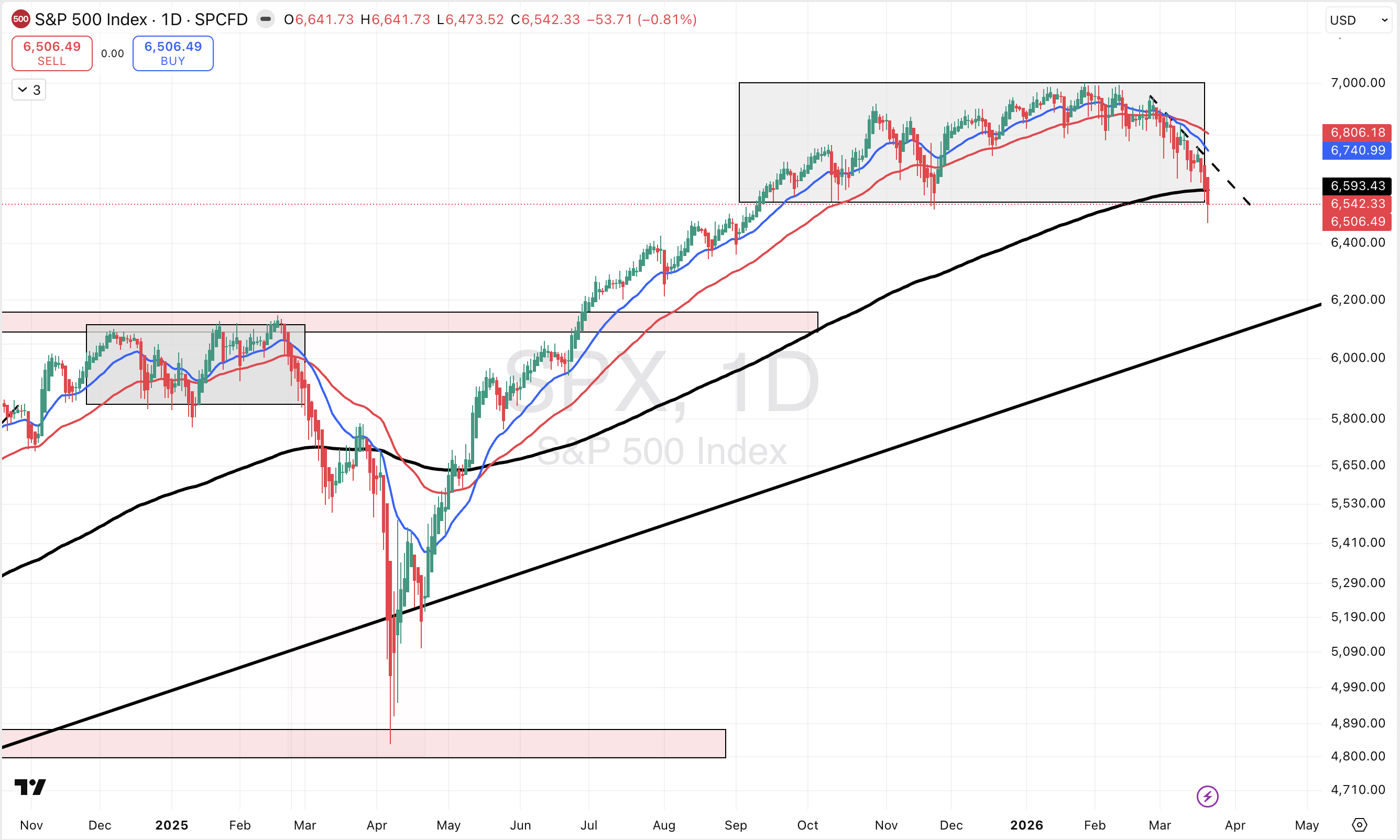

- Equities, Not Yet At Extreme Fear - With equities in a broad-based downtrend, the question is whether these are oversold enough to facilitate a bounce? With both S&P and Nasdaq trading some 2 std-dev below averages, the set up does augur well for a bounce - but the risk is of a dead-cat-bounce rather than a sustained reversal. Sentiment and breadth have retrenched substantially, but are not yet quite at extreme levels. Importantly, major indices are sitting on and testing critical 200dma, and breaks below risks deeper declines. Our proprietary Market Signals Model is now in bearish territory.

- US Sectors Still lead - In a downtrend, relative trades matter - and in the current context, despite the downtrend, it's US sectors that are leading while international markets remain in a tough spot, as do commodities (other than oil, of course).

US Equities Lead International Equities; Commodities (ex-Oil) Weak

source: Lighthouse Canton

Lighthouse Canton Proprietary Market Signals Model - In Bearish Territory

source: Trading View, Lighthouse Canton

S&P - Poised on a Knife Edge - A 200dma break risks deeper declines

source: Trading View

Nasdaq 100 - Smilar Knife Edge Positioning

source: Trading View

VIX - Higher Volatility is an Opportunity

source: Trading View

Breadth - Weak - BUT - Not Weak Enough

source: Trading View

Sentiment - Weak - BUT Not Yet Turned

source: Macro Micro

No items found.

Subscribe to our Insights & Updates

Oops! Something went wrong while submitting the form.

.png)

%20(14).png)

.png)