A single layer of the AI supply chain - advanced semiconductor fabrication and high-bandwidth memory - has reshaped equity index composition in the EM universe to unprecedented levels. History says such concentration amplifies investor risk.

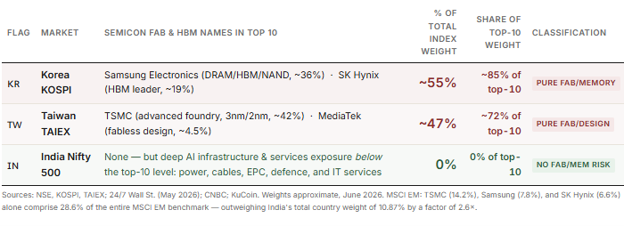

For India, the paradox is clean: India has been penalized by global allocators for lacking the most dangerously concentrated sector exposure in the EM universe. That same absence - of semiconductor and memory risk - is now its most compelling structural attribute. Zero concentration in the most crowded EM trade and at the same time full participation in the next one.

Can global investors continue ignoring this?

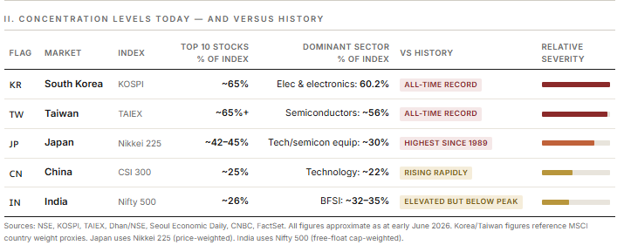

MSCI Emerging market index - A Concentration Without Precedent

In just 24 months, advanced semiconductor fabrication and high-bandwidth memory have reshaped equity markets faster than any theme since the 2000 dot-com peak. Yet, the AI boom is not a broad sector rally; it is concentrated in the two or three companies that manufacture the hardware. Breaking from past cycles like the dot-com boom or China's commodity Supercycle, this phenomenon has uniquely propelled two emerging markets to the forefront: Taiwan dominates advanced fabrication, and Korea leads memory production.

The result is an extraordinary convergence in index concentration metrics. In Korea and Taiwan, the concentration levels are entirely uncharted territory; no comparable precedent exists in any major equity market, anywhere, ever. History shows that such narrow market reliance sharply elevates investor risk.

Let us look at the scale of this concentration in the MSCI Emerging Markets benchmark itself. Just three companies, TSMC, Samsung Electronics, and SK Hynix, now constitute approximately 28% of the entire index: TSMC at 14.2%, Samsung at 7.8%, and SK Hynix at 6.6%. India, the world's fifth-largest equity market, carries a total country weight of 10.87% - a six-year low. Just these three semiconductor and memory fabricators alone outweigh the entirety of India's MSCI EM representation by a factor of 2.6 times.

India - The Advantage of Absence

India's position in the EM universe at this moment appears structurally unique. It is the only major emerging market that simultaneously offers zero concentration in the most crowded semiconductor and memory fabrication trade.

More importantly, India also offers a deep, listed, and largely under-owned set of direct beneficiaries of AI infrastructure that global capital is now increasingly pivoting toward. Global capital is rapidly rotating beyond pure-play AI software and chips into the physical backbone powering the technology: energy, grid equipment, and data center infrastructure.

As data center power constraints intensify globally, the market has realized that the ultimate bottleneck for artificial intelligence is not just computing code, but electricity, cooling and allied infrastructure.

The world has spent two years rewarding the companies that make the chips. It is now beginning to spend on the infrastructure those chips require: data centers, power grids, cooling systems, cables and the enterprise AI transformation services that convert raw compute into economic value. Korea and Taiwan own the first trade. India is exceptionally well-positioned for the second, the AI plus infrastructure ex semiconductors and memory.

Beyond the Chips: India Steps into theAI Infrastructure Spotlight

India's entry point into the AI infrastructure trade presents a highly attractive, asymmetric setup for global investors. The market arrives at this pivot with attractive valuations (MSCI India trades at a substantial discount to its all-time high premium seen two years ago), foreign institutional ownership hovering at a six-year low, and an MSCI EM index weight that has already fully priced in the penalties of missing the initial semiconductor manufacturing cycle. Historically, such convergence - reasonable entry multiples combined with deep institutional under-ownership - has acted as a springboard preceding India's strong period of regional and global outperformance.

%20(16).png)

.png)