Germany, long known for its fiscal conservatism and strict adherence to budgetary discipline, has taken a decisive turn with its recently announced fiscal spending package. This shift marks a significant departure from the country’s historical aversion to large-scale government stimulus, signaling a new era of economic expansion fueled by infrastructure investment, defense modernization, and industrial renewal.

With the government committing substantial funds to upgrade transportation networks, accelerate the green energy transition, and strengthen national security, key sectors are poised to benefit, creating compelling investment opportunities in the German equity market.

This paradigm shift not only enhances Germany’s long-term growth trajectory but also provides a strong cyclical boost to companies operating in construction, infrastructure, defense, and building materials. As government contracts and public-private partnerships gain momentum, investors should focus on companies best positioned to capitalize on this unprecedented fiscal stimulus.

Several stocks have already started reflecting optimism around this policy change, making it an opportune moment to assess the potential beneficiaries of Germany’s fiscal evolution.

However, the defense theme appears to have largely played out, with stocks like Rheinmetall now trading at extreme valuations - currently at 45x 1-year forward earnings—reflecting much of the anticipated growth. While the sector remains structurally attractive, the risk-reward dynamic at these levels is less compelling.

Instead, we see greater opportunity in infrastructure and building materials stocks, where valuations remain more reasonable despite the strong tailwinds from fiscal spending. These segments offer a more attractive entry point for investors looking to benefit from Germany’s new investment cycle without paying excessive premiums.

That said, while these stocks are still attractively valued, they too have experienced a material run-up and may be susceptible to near-term pullbacks. As such, investors looking for exposure may also consider structured solutions such as fixed coupon notes, which can provide downside protection while allowing participation in the sector’s long-term upside.

Following are our top recommendations :-

Heidelberg Materials (HEI GY) – Intrinsic value estimate of EUR 204 (15% Upside potential)

Company Overview:

- Heidelberg Materials is one of the world’s largest suppliers of cement, aggregates, and ready-mixed concrete, playing a key role in global infrastructure and construction markets.

- The company has a strong presence across Europe, North America, and emerging markets, with a focus on sustainable building materials and CO₂ reduction technologies.

- It is actively transitioning toward a low-carbon future, investing in carbon capture, utilization, and storage (CCUS) solutions and alternative materials.

Past Growth and Performance:

- Revenue Growth: Heidelberg Materials has delivered stable revenue growth, driven by strong demand in infrastructure and residential construction projects.

- Profitability Metrics: The company maintains EBITDA margins in the range of 20-25%, supported by cost optimization and pricing power in key markets.

- Return on Invested Capital (ROIC): ROIC has consistently ranged between 8-12%, reflecting efficient capital allocation and strong cash flow generation.

- Free Cash Flow & Capital Allocation: Strong free cash flow allows for reinvestment in growth initiatives, debt reduction, and shareholder returns through dividends and buybacks.

Future Growth Potential:

- Infrastructure Boom & Fiscal Stimulus: Heidelberg Materials is set to benefit from Germany’s increased fiscal spending on infrastructure, as well as the broader EU’s green energy transition and sustainable construction initiatives.

- Decarbonization & Green Cement: The company is at the forefront of developing low-carbon cement solutions, positioning itself as a leader in sustainable construction materials.

- US & European Market Strength: Demand for aggregates and cement remains strong, particularly in the U.S. and Europe, where government-led investments in public infrastructure are accelerating.

- Digitalization & Efficiency Gains: Adoption of digital tools and AI-driven logistics is enhancing operational efficiency and reducing costs.

Investment Rationale:

- Sector Tailwinds: Well-positioned to benefit from increased infrastructure spending and sustainability-driven construction trends.

- Financial Strength: Strong balance sheet, healthy margins, and consistent cash flow generation.

- Strategic Sustainability Focus: Leadership in decarbonization and innovation in sustainable materials enhances long-term growth prospects.

- Attractive Valuation: Despite the recent rally, Heidelberg Materials remains well-positioned for further upside as infrastructure demand remains robust. The stock currently trades with a free-cashflow yield of 6.9%.

Holcim (HOLN SW) – Intrinsic value estimate of CHF 115 (14%Upside potential)

Company Overview:

- Holcim is a global leader in innovative and sustainable building solutions, specializing in cement, aggregates, and ready-mix concrete.

- The company has been shifting its business model to focus on high-value solutions and sustainability, including green building materials and advanced construction technologies.

- Holcim has a presence in over 70 countries, with a growing emphasis on North America, Europe, and high-growth emerging markets.

Past Growth and Performance:

- Revenue Growth: Holcim has delivered steady revenue expansion, supported by strong demand for construction materials and sustainability-focused solutions.

- Profitability Metrics: The company maintains EBITDA margins in the range of 22-26%, benefiting from pricing discipline and cost efficiency measures.

- Return on Invested Capital (ROIC): Holcim’s ROIC has improved to around 10-14%, reflecting its focus on higher-margin solutions and asset-light growth strategies.

- Free Cash Flow & Capital Allocation: Strong free cash flow generation has supported deleveraging, dividends, and strategic M&A in sustainability-focused businesses.

Future Growth Potential:

- Spin-Off of North American Business: Holcim is preparing to spin off its North American operations, unlocking value and allowing for a more focused growth strategy in this high-margin, fast-growing market.

- Decarbonization & Circular Construction: Holcim is a leader in low-carbon cement, green concrete, and recycling technologies, positioning itself well for the shift toward sustainable construction.

- Infrastructure Spending & Urbanization: Increased infrastructure investments in the U.S., Canada, and Europe are driving demand for Holcim’s construction materials.

- Portfolio Optimization & M&A: The company continues to divest non-core assets and expand into high-margin, sustainability-driven solutions, enhancing profitability and growth prospects.

Investment Rationale:

- Structural Growth Drivers: Positioned to capitalize on sustainability trends, infrastructure investment, and urbanization.

- Strong Financials: Healthy margins, improving ROIC, and robust free cash flow provide financial flexibility.

- Value Creation from Spin-Off: The planned North American spin-off could unlock significant shareholder value and allow Holcim to focus on high-growth segments.

- Attractive Valuation: Despite recent share price appreciation, Holcim remains a compelling investment given its transformation strategy and leadership in sustainable building materials and its consistent free-cashflow generation. The stock currently trades with a free-cashflow yield of 6.3% and we are reasonably confident in sustained future growth in free-cashflow.

- Dividend: The stock trades with an indicative dividend yield of 3.1%.

Vinci S.A. (DG FP) – Intrinsic value estimate of EUR 139.5 (17%Upside potential)

Company Overview:

- Vinci is a global leader in concessions and construction, operating one of the largest infrastructure businesses in Europe. The company manages toll roads, airports, and energy infrastructure while also being a key player in construction, civil engineering, and real estate development.

- Vinci’s business is divided into two main segments: Concessions, which include toll roads, airports, and public infrastructure contracts, and Contracting, which covers construction, energy, and engineering services.

- The company benefits from stable, long-term revenue streams from its infrastructure concessions, complemented by cyclical but high-margin contracting operations.

Past Growth and Performance:

- Revenue Growth: Vinci has delivered consistent top-line growth, driven by both organic expansion and strategic acquisitions. Over the past five years, the company has maintained a mid-single-digit revenue CAGR.

- Profitability Metrics: Vinci’s operating margins have been stable, with the Concessions segment delivering margins of 45-50%, while the Contracting segment operates at lower but stable margins of 5-7%.

- Return on Invested Capital (ROIC): The company generates a solid ROIC of around 10-12%, underpinned by its asset-heavy concessions business and disciplined capital allocation.

- Free Cash Flow & Capital Allocation: Vinci generates significant free cash flow, which has been used for dividend payments, share buybacks, and reinvestment in infrastructure projects.

Future Growth Potential:

- Infrastructure Spending Boom: Vinci is well-positioned to benefit from increased government spending on infrastructure in Europe and beyond, particularly in transportation and energy projects.

- Airport & Toll Road Expansion: As global travel rebounds post-pandemic, Vinci’s airport operations are set to recover further, while road traffic remains a long-term growth driver.

- Renewable Energy & Electrification: Vinci is expanding its energy infrastructure capabilities, benefiting from Europe’s push toward decarbonization and grid modernization.

- Mergers & Acquisitions: The company has a history of strategic acquisitions that strengthen its global presence, particularly in transport infrastructure and energy services.

Investment Rationale:

- Strong Business Model: Vinci’s combination of stable, high-margin concessions and growth-oriented contracting businesses provides a well-balanced portfolio.

- Secular Growth Drivers: Infrastructure spending, urbanization, and green energy transition provide long-term tailwinds.

- Resilient Financials: Strong cash flow generation, disciplined capital allocation, and a solid balance sheet.

- Attractive Valuation: Despite its recent rally, Vinci still trades at reasonable valuation levels compared to historical averages, offering an appealing entry point (free-cashflow yield of 7.3%).

- Dividend: The stock trades with an indicative dividend yield of 4%

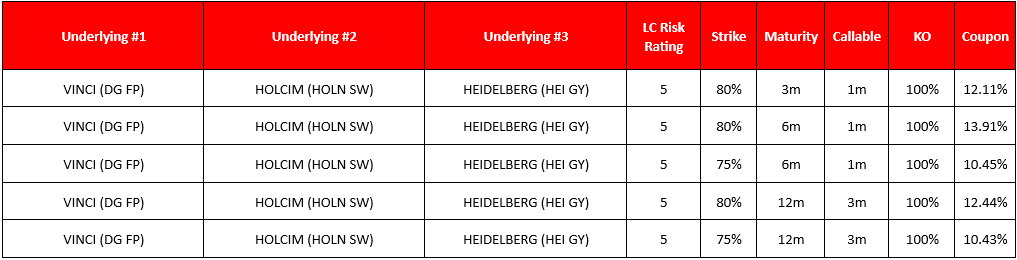

FCN Ideas on the stocks mentioned above :-

%20(16).png)

.png)