Investor sentiment in India’s venture and private equity market is showing signs of revival after three years of turbulence. Later-stage funds are emerging as key beneficiaries, with IPOs and M&A exits helping restore liquidity and confidence in the cycle.

Sohil Chand, Founding Partner and CIO at LC Nueva, said the appetite is clear.

“We are seeing a lot of interest in later-stage deals because investors are closer to liquidity, and that is driving strong buying interest. There are also opportunities because many firms are nearing the end of their fund lives. For the LC Nueva Momentum fund, our role is to work closely with them, help clean up their cap tables and provide the final round of funding before a liquidity event.”

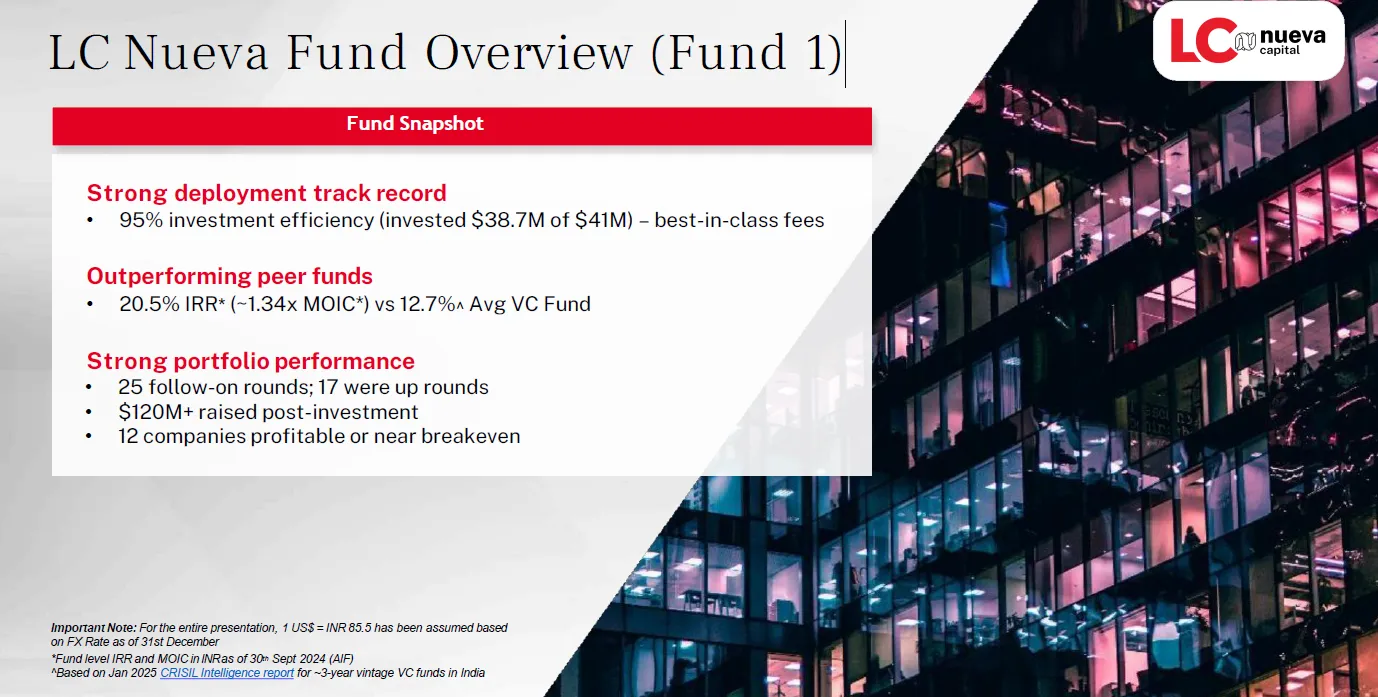

Lighthouse Canton has partnered with Nueva Capital to form LC Nueva Investment Partners. Together they have launched the LC Nueva Fund which has invested in 35 companies, 30 of which were series A and below. USD 41 million was completely deployed as a part of this fund which closed in September 2023 with below performance.

The second fund, called LC Nueva Momentum Fund, is currently fundraising

The VC market in India: From boom to bust to reset

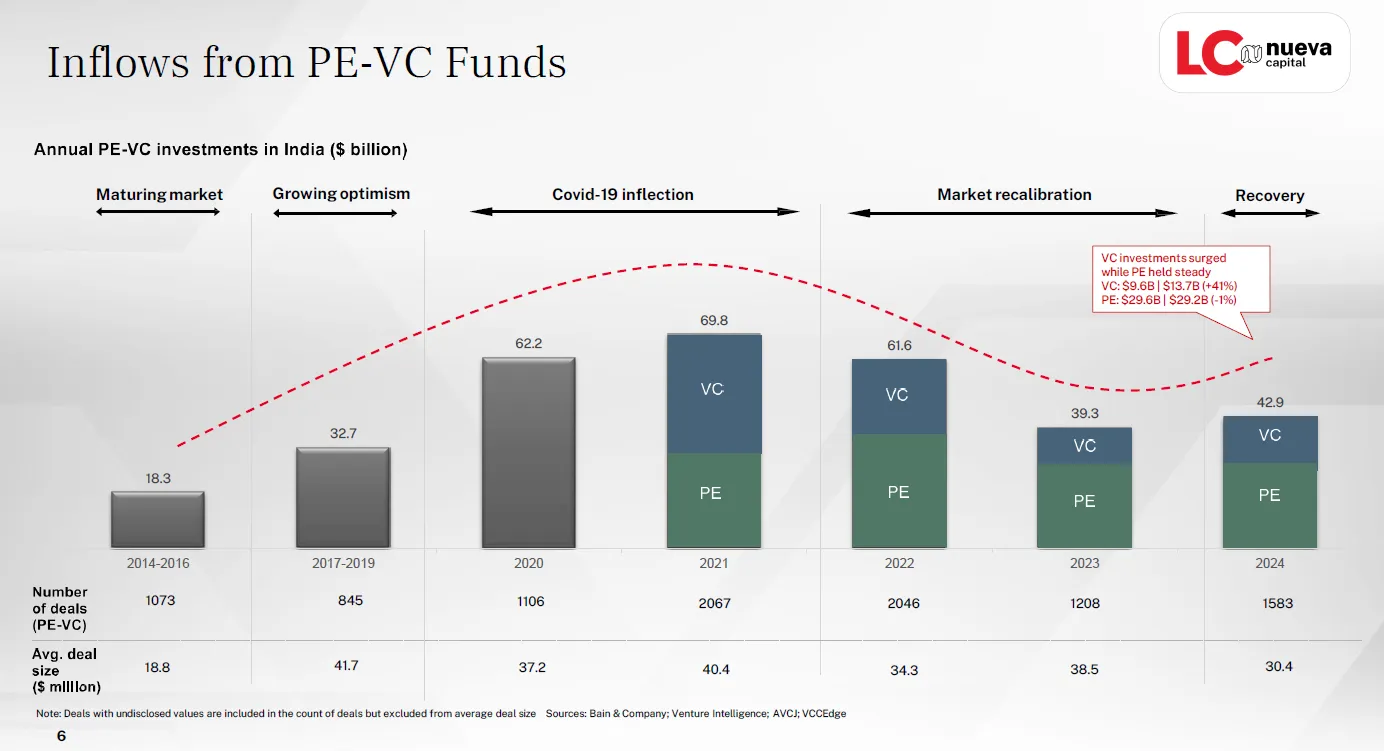

The renewed momentum in the VC market in India comes after a dramatic cycle of excess and correction. Sharing his views on the landscape, Chand traced how the market overheated in the pandemic era before returning to more sustainable ground.

“Investor interest built steadily from the early 2000s, culminating in the post-COVID boom of 2020–21 when deal activity surged. Companies that were not ready for funding raised significant capital, valuations were marked up weekly, and angel investing exploded. But this came with unrealistic expectations, he noted.”

When growth overtook profitability, discipline evaporated.

“There was a massive focus on revenues and growth, with a complete disregard for bottom-line economic principles. Profitability stopped mattering. At some point, larger investors realised this was unsustainable. Without clear exit pathways, they began pulling back commitments, and the entire industry corrected sharply.”

Exits drive a new upcycle

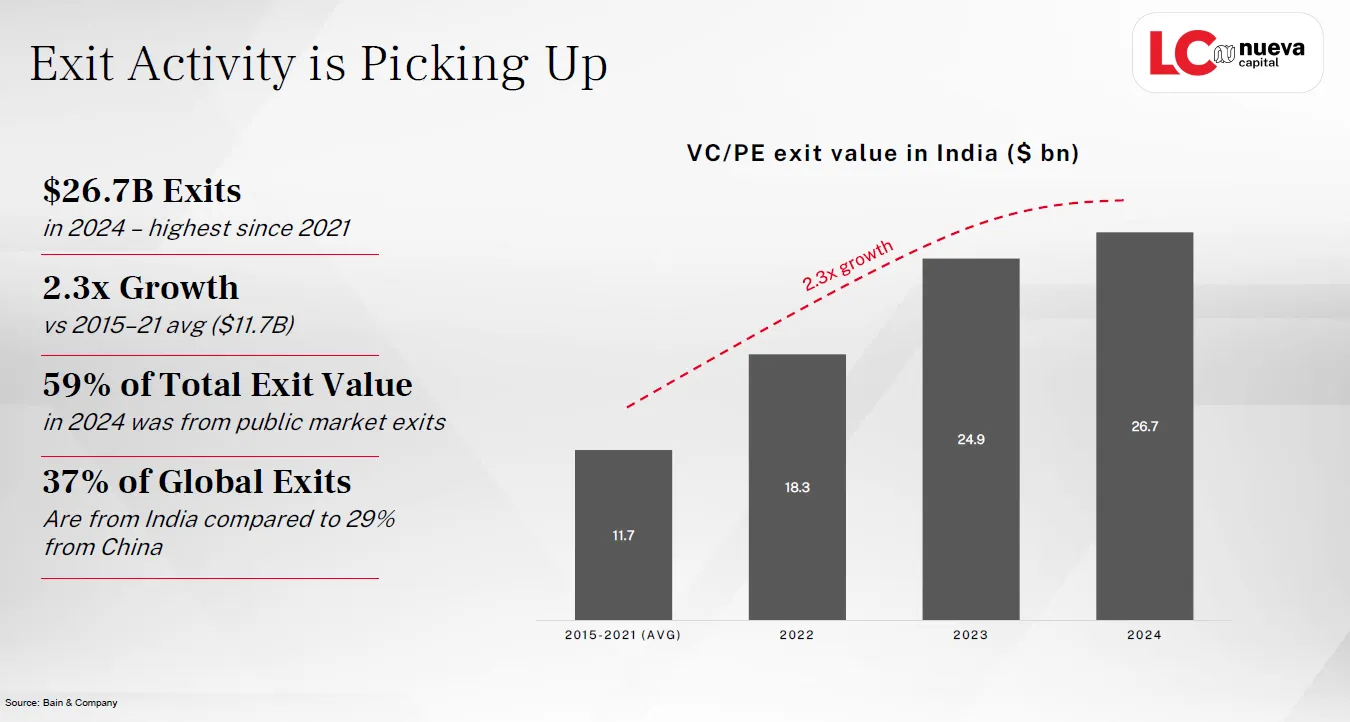

If the 2020–23 downturn was marked by a capital drought, 2024 signalled recovery, led by exits.

Chand pointed to the change in tone: “In 2024 a wave of IPOs renewed investor enthusiasm. Companies such as Zomato, Swiggy and Oyo Electric captured market attention, and venture-backed businesses became attractive again.”

That enthusiasm is borne out by data. Exit value in India hit $26.7 billion in 2024, the highest since 2021 and more than twice the 2015–21 average. Nearly 60% of exit proceeds came from IPOs, with the rest spread across secondary sales and M&A.

Chand believes exits are set to multiply. “We expect exits through both IPOs and M&A, similar to trends in the US. Large, listed companies now have the capacity to make acquisitions. This will create a strong exit environment and fuel the next round of startup activity.”

That pipeline is critical for sustaining the investment cycle. “We are entering a good cycle. Over the next five years, momentum for both new investments and exits will strengthen considerably,” Chand said.

Pre-IPO trades versus long-horizon funds

As optimism returns, competition for capital has sharpened — particularly from pre-IPO deals.

“The main competition we face is from investors weighing whether to participate in pre-IPO situations. Our fund has a four to five-year horizon, while pre-IPO plays offer a shorter one- to two-year cycle.”

But Chand argued that short-term gains are limited. “You are not going to make three to five times your money in a pre-IPO. These deals are typically priced at fair value. Investors may get a small pop at listing, but they are then locked in for six months. Returns are incremental, not transformative.”

In his view, pre-IPO allocations should be seen as extensions of public-market strategies rather than substitutes for private equity.

“Pre-IPO positions should come from an investor’s public market allocation because the risk-return profile is similar. Yet many families still view them as part of their private market bucket, often telling us they can either put money in a fund or into a specific pre-IPO opportunity.”

Global flows underpin India’s growth story

While India’s domestic market is large and growing, international capital continues to anchor its private markets.

“The US has always been the largest source of capital for India. Most funds here are backed by American endowments, pension funds, institutional investors, and family offices. Some European family offices participate, and Asia, particularly non-resident Indians, also plays a meaningful role.”

Chand noted that Japanese investors are beginning to show interest, but restrictions mean Chinese capital remains limited.

“China has not historically been a large investor in India due to regulatory barriers and the state of bilateral relations. If the market were open, we would likely see more flows, but today it is more neutral markets such as Japan and Korea that are assessing allocations between China, India and the US.”

For LC Nueva, however, the immediate focus is closer to home.

That Asia-first strategy reflects pragmatism as well as positioning. With exits rebounding and later-stage funding in demand, Chand sees momentum building in India and Asia itself. “The bottom of the cycle is behind us. We are in a new upcycle that will strengthen over time. The outlook is steadily improving, making us focus the fund within the region”

%20(16).png)

.png)