Lighthouse Canton is launching a systematic, rules-based model portfolio, designed to deliver long-term outperformance vs. S&P 500 with lower drawdowns and higher absolute and risk-adjusted returns.

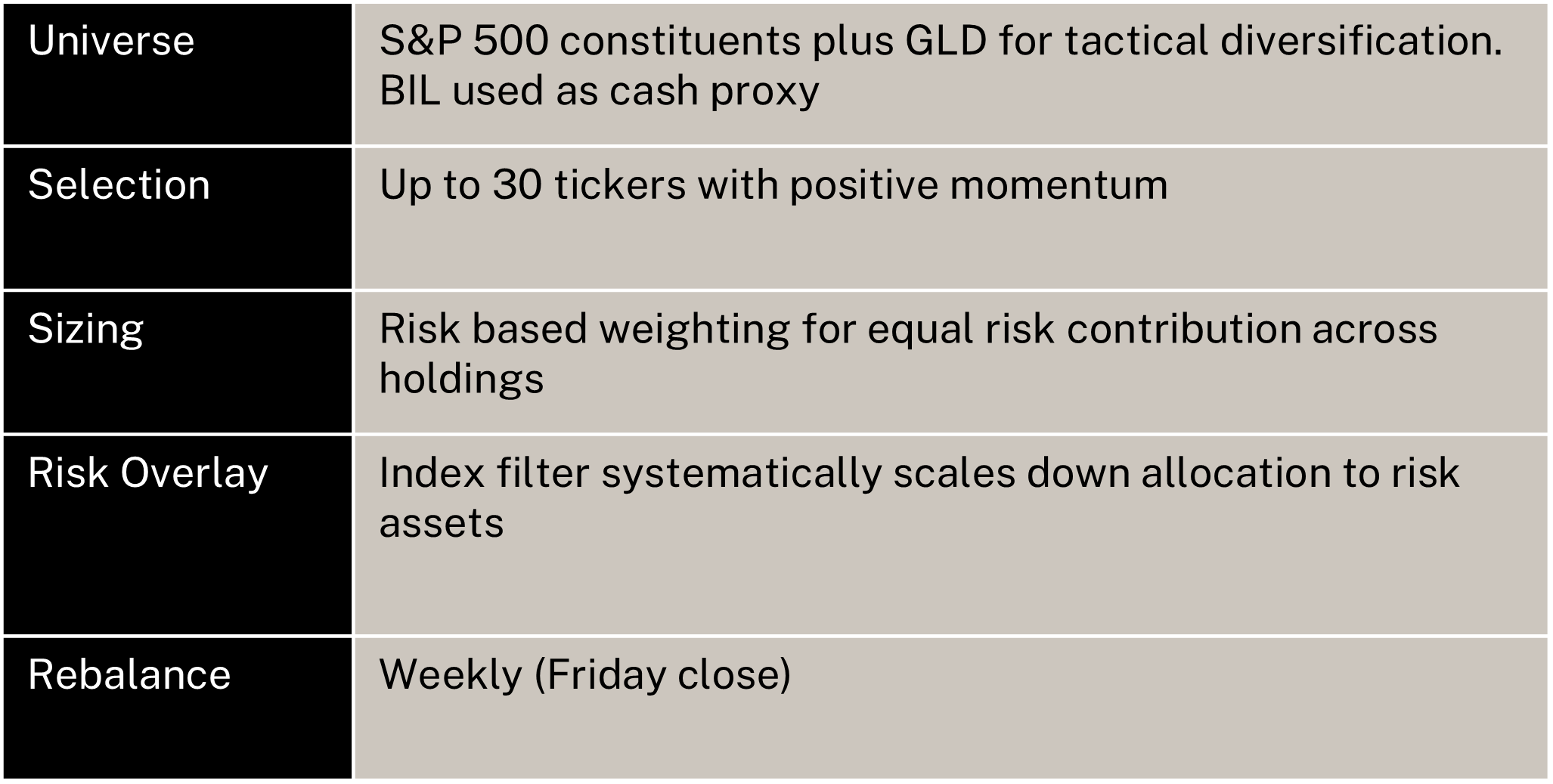

A long-only strategy, investing in up to 30 stocks in the S&P 500, the strategy’s ability to hold cash proxies (BIL) and tactical diversifiers (GLD) makes this an all-weather portfolio where allocations are based on risk rather than market cap. A key feature of the strategy is managing downside risk through regime filters as well as position sizing.

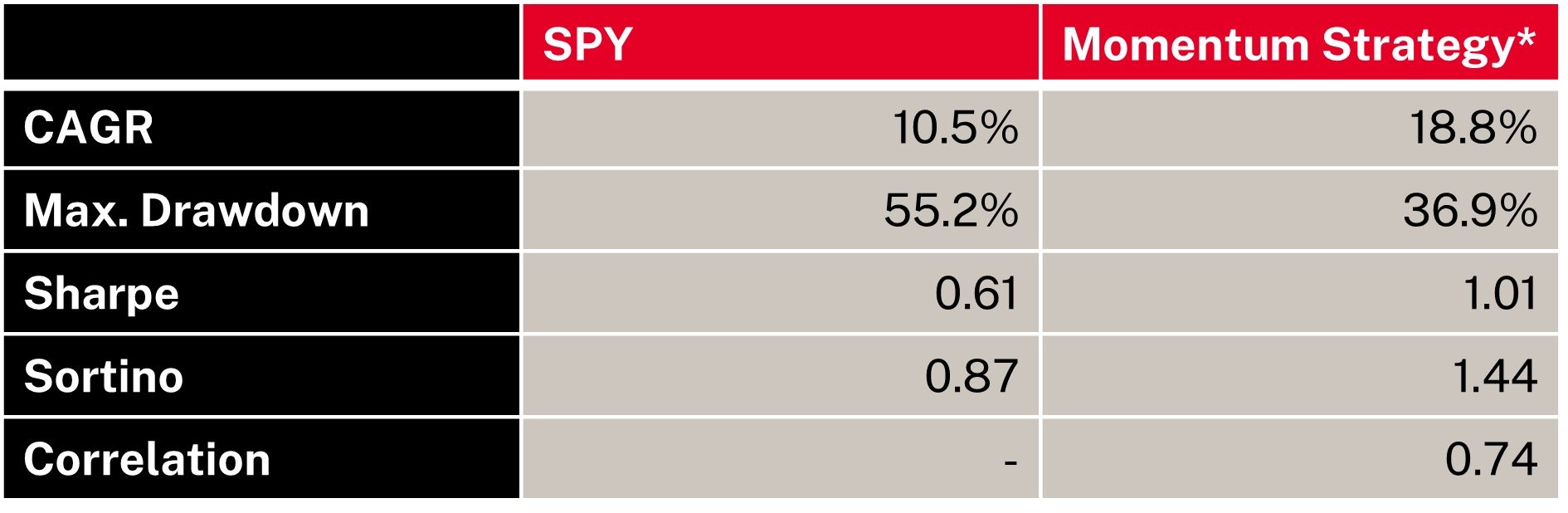

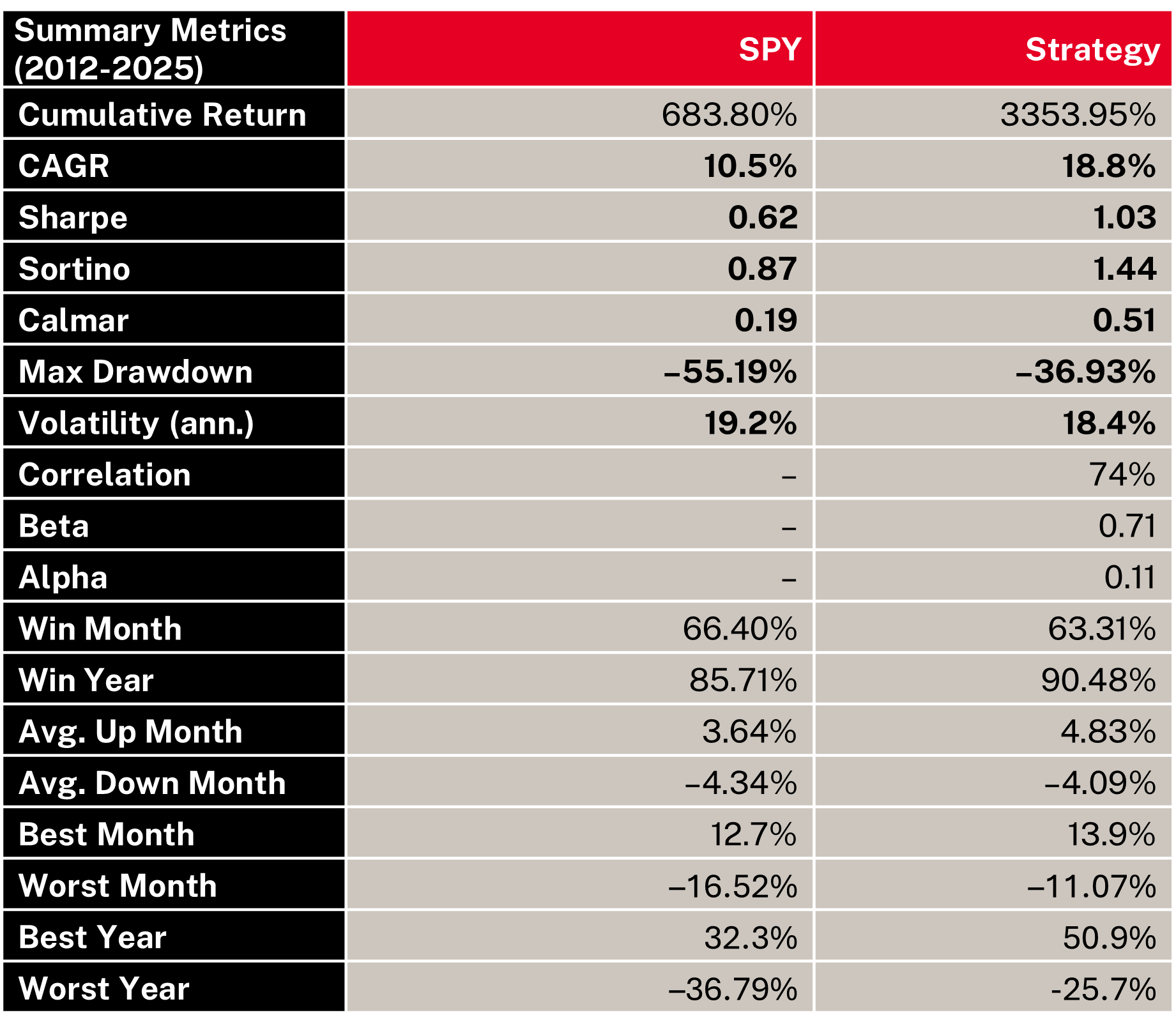

Our extensive back-tests* show a 18.8% CAGR (vs. 10.5% for S&P) with a lower max. drawdown of 37% (vs. 55% for S&P), delivering superior Sharpe and Sortino ratios.

Historical Performance

Historical Drawdowns

Investment Rationale, Strategy & Portfolio Framework

Leveraging the well-known “Dual Momentum” framework (selection based on absolute and relative momentum),this enhanced version uses a wider array of investments (up to 30stocks from the S&P 500 universe). A regime adaptive overlay augments the strategy through a rotation into defensive assets (Cash & Gold) when overall market conditions deteriorate. Risk based position sizing and allocation helps reduce overall volatility and drawdowns.

Research shows that equities exhibiting strong relative performance over the intermediate term (3–12 months)tend to continue outperforming. The strategy operationalizes this “momentum anomaly” in a liquid, transparent, risk-controlled format.

- Objective: Deliver consistent, risk-adjusted outperformance of the S&P 500 by systematically rotating into the strongest-trending large-cap equities while maintaining strict risk controls.

- Structure: Long-only.

- Systematic: No discretionary overrides; fully transparent and repeatable.

- Regime-Adaptive: Index-level filters curtail exposure when market momentum turns negative.

- Edge: Combines long-term momentum with systematic portfolio construction and risk management to reduce drawdowns and volatility.

All-Weather, Adaptive Design

Unlike passive buy-and-hold portfolios or traditional ETFs, this strategy is designed to be regime-aware and risk-weighted, not market-cap weighted. By actively adjusting exposure and embracing tactical diversification, it functions as an “all-weather” portfolio.

Historical Performance*

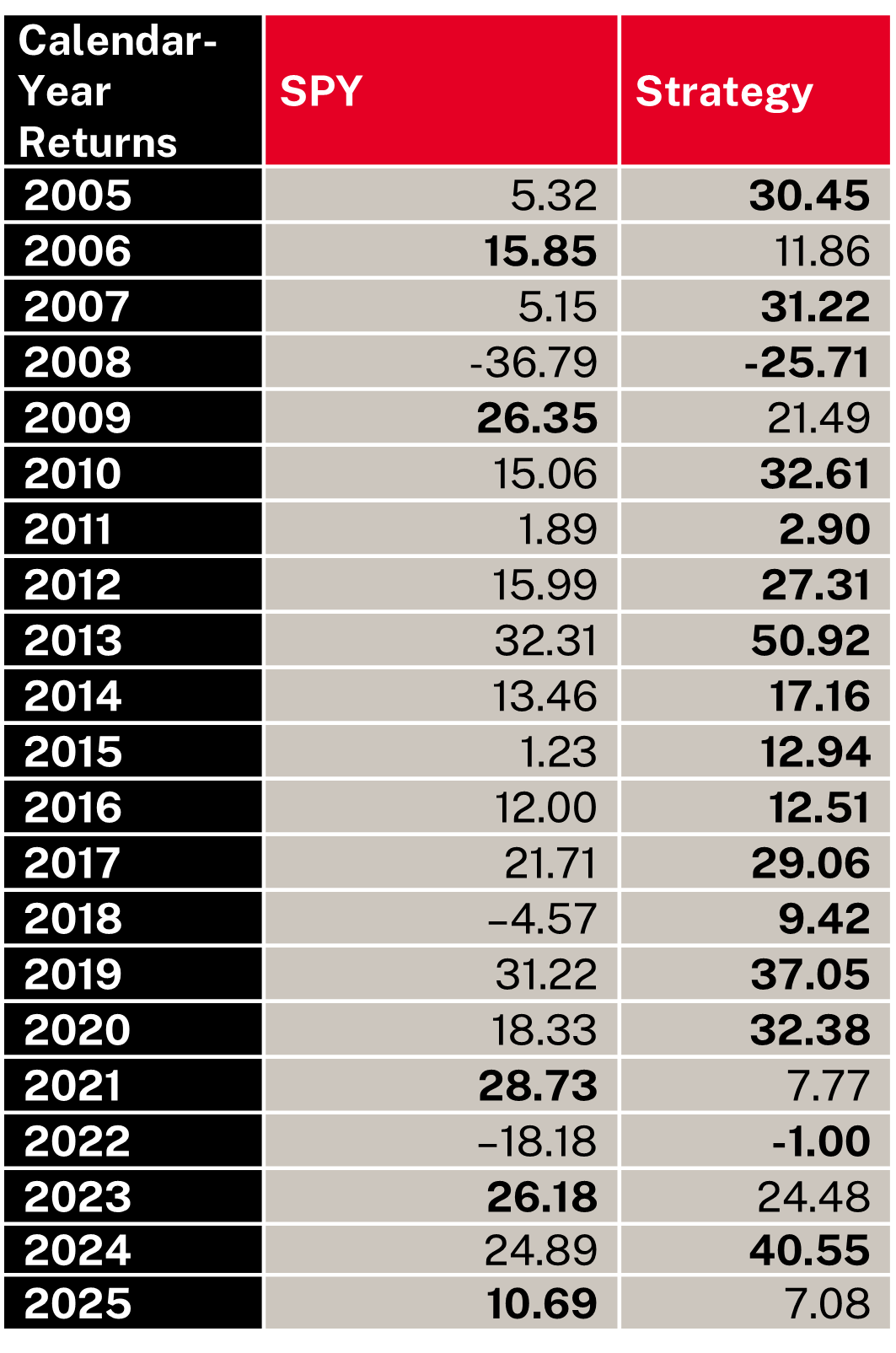

- Consistent Outperformance: Strategy beats SPY in 16 of 21 calendar years.

- Crash Resilience: Q12020 drawdown limited to –27% versus –34% for SPY.

- Lower Beta: Realized Beta to SPY averages 0.71 despite being long-only.

Calendar-Year Returns

EOY Returns

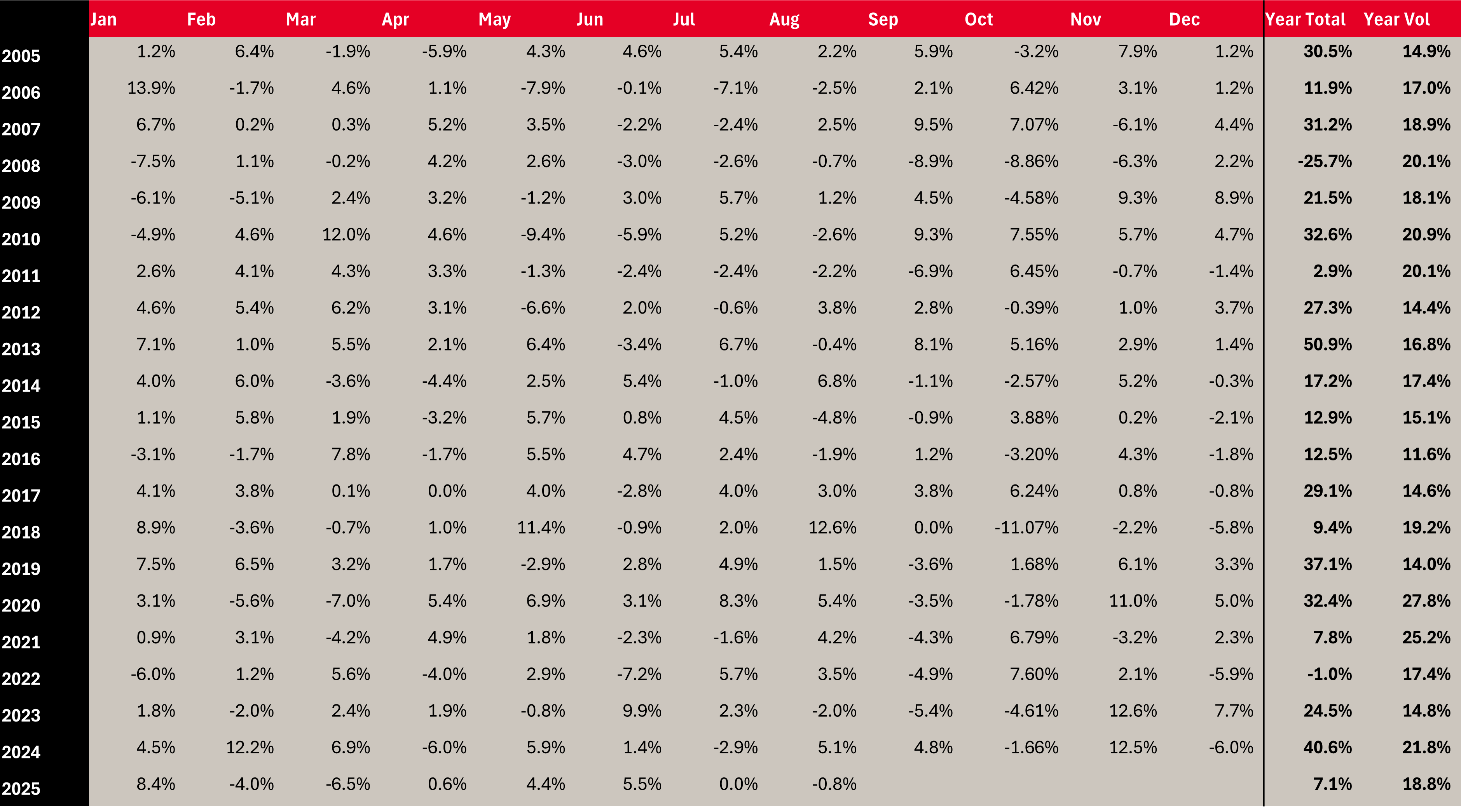

Strategy Monthly Returns

Investment Team

|  |

| Devansh Bhatt Analyst, Investments | Sunil Garg, CMT Managing Director Chief Investment Officer |

Disclaimer

This document provides a general overview of Lighthouse Canton S&P 500 Momentum Strategy, a Model Portfolio for which Lighthouse Canton (the "Manager") is the Investment Manager. It is not to be construed as an offer to sell or solicit an offer to buy any financial instruments in any jurisdiction. The contents of this document may not be reproduced or referenced, either in part or in full, without prior written permission from the Manager.

Information contained herein is qualified in its entirety by reference to the Memorandum, Associated Documents and Subscription Agreement relating to the purchase of interests in the fund, and these documents should be reviewed carefully prior to taking any investment decision(s). It may include any data and projections based on underlying assumptions, management forecasts, information analysis and views of the author(s), which are subjected to change. Neither the Fund nor the Manager are under any obligation to update you on any changes made to this document.

This document is prepared by Lighthouse Canton Pte. Ltd. and its affiliate company, Lighthouse Canton Capital (DIFC) Pte. Ltd., which are regulated by Monetary Authority of Singapore ("MAS") and Dubai Financial Services Authority ("DFSA") respectively. MAS and DFSA have no responsibility for reviewing, verifying and approving the contents of this document and/or other associated documents. The contents of this document may not be reproduced or referenced, either in part or in full, without prior written permission from LC.

This document is based on information from sources which are reliable, but has not been independently verified by Lighthouse Canton Pte Ltd or its affiliates ("LC"). LC has taken the reasonable steps to verify the contents of this document, and accept no liability for any loss arising from the use of any information contained herein. Please also note that past performances are not indicative of future performance.

This document is only intended for Accredited Investors and/or Professional Clients, as defined by MAS and DFSA.

Information contained herein are those of the author(s) and does not represent the views held by other parties. LC is also under no obligation to update you on any changes made to this document.

%20(16).png)

.png)