Central banks around the world have somehow converged to a seemingly “magical” 2% inflation target. Western nations, struggling in recent years with sticky/ high inflation want it contained around 2% while some of the deflationary economies– Japan in the past and China currently, also want 2% (India is also below 2%)– why this obsession? Is this even valid any more? Especially with protectionism on the rise?

We are not value judging protectionism (leave that to the voters) BUT, we do believe that when facts change, so should views – and this is the basis for challenging, or at least rethinking this 2% inflation obsession – central banks need to be, at the minimum, not oblivious to shifting sands. We posit that not only does a more insular world require a revisit of current inflation targets, “ranges” are a more pragmatic approach rather than singe point inflation targets.

Shorter-term, the dilemma facing the FED is whether to cut at the Sep FOMC – their inflation obsession prevents a cut, and political pressure aside, jobs weakness warrants easing. Markets are polarized in expecting a 25bp cut at the next FOMC (mid-Sep), although we don’t see enough evidence of economic weakness to warrant a cut – the real shocker will be if the FED stands pat!

Historical Context - US

US Inflation Wasn't Always 2%

.png)

source: Trading Economics

Evolution of Inflation Regimes in The US

In a historical context, the 2% target was formalized by the Bernanke led FED, only as recently as 2012 – an era of peace and peak globalization. Bernanke’s learned predecessor, Greenspan preferred to deal, pragmatically we think, in ranges, rather than a single hard number.

While the FED may still be haunted by the ghosts of the 1970s, winds of globalization, initially under GATT (Global Agreement on Trade & Tariffs) and later under WTO (especially since China joined in 2001), had substantially boosted trade flows (and services), all with disinflationary outcomes. A 2% target made sense then – but does it now?

Historical Context -Eurozone

Eurozone's Real Problem is Deflation!

source: Trading Economics

- 2% inflation target as part of the price stability mandate

- Formally confirmed in 2003 – “keep inflation low, but close to 2% over the medium-term”.

While the ECB has been far more focused on inflation, due in part for currency stability, the Eurozone and its flirtations with deflation are an area that perhaps merits even more attention.

Is Inflation Always Bad?

Ask Japan! Dealing with deflationary trends for over three decades, inflation is actually welcome and perhaps explains why the BOJ has remained hesitant in raising interest rates.

The important point here is that excessive inflation is damaging to growth but deflation is worse. Empirical evidence also suggests that it’s the severity and persistence of of inflation that is more important than the level itself. While deflation is easier to define, what is “excessive” is harder to evaluate, further making the case for inflation targeting to be in ranges and environment sensitive.

Inflation is Not Always Bad

.png)

source: Trading Economics

Sources of Inflation Also Critical

Demand Pull Inflation needs a very different antidote when compared to Cost Push Inflation – with monetary policy playing a far more critical role in the former and arguably ineffective in the latter case. While its true that supply side pressures, if sustained, will eventually seep through to core inflation, whether monetary policy can tackle this, is debatable.

Is 2% a Viable Number in Today’s World?

Fast forward to today – protectionist tendencies have been building up for awhile – and its not just tariffs on goods trade. Labor mobility has been as much a part of growth and disinflation trends, as has been the globalization of services. Rising nationalism and the convenient political rhetoric of “keeping jobs at home” now threatens both globalization of services and labor mobility – shed a tear for that fateful Jun 2016 Brexit referendum! And now of course we have tariffs and full blown trade protectionism at play.

Our aim is not to value judge protectionist trends – while we have views on this, it is ultimately the voters in respective countries that make that call. Our aim however is to challenge the 2% inflation obsession – paraphrasing the old Keynesian saying “when facts change, views can and must change” – central banks appear oblivious to an environment that makes the 2% inflation target somewhat obsolete.

What about central bank credibility – after all moving goal posts mid-way in a game is akin to match fixing– we get that – BUT, we aren’t talking about a trading approach to inflation targets – rather a pragmatic admission of structural changes that warrant are-adjustment. And while they are at it, move a range based approach than a single number plucked out of the air.

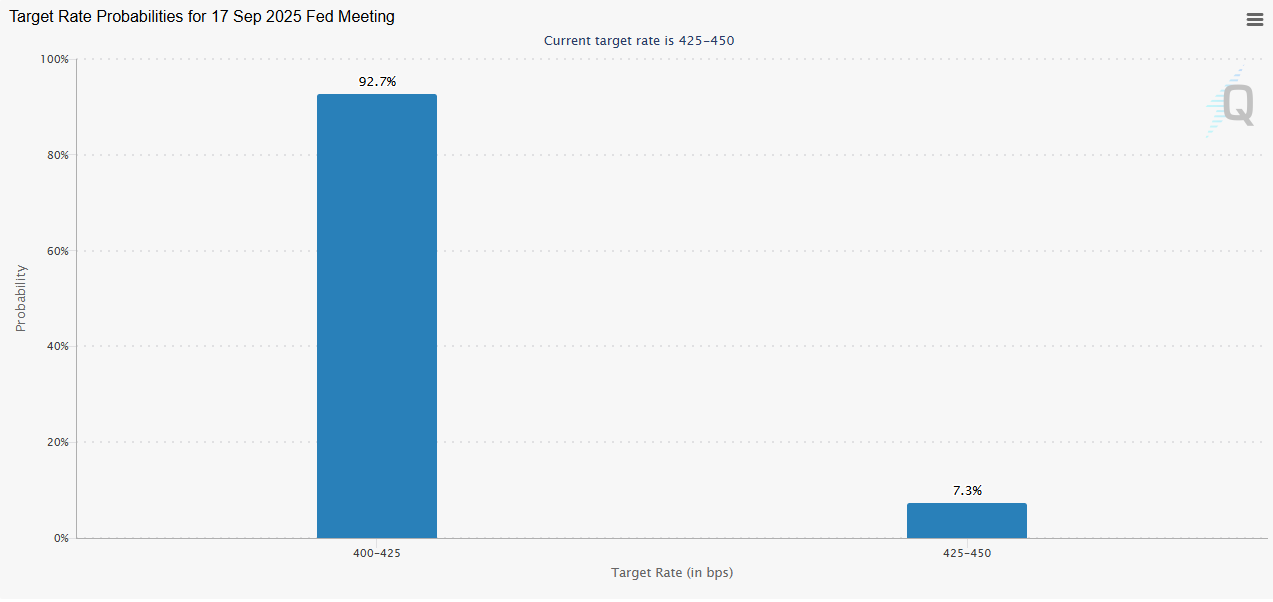

Should The FED Cut in September?

A shorter term consideration for both the FED and the market is whether the Sep’25 FOMC will lead to a rate cut. Politicians of course not only want “a rate cut” but a much bigger one. Within the FED, the “doves” are adding up in numbers, perhaps with an eye towards the upcoming leadership role. Yet, there are enough “hawks” who worry about inflation.

Futures meantime are pricing in a near certain rate cut – BUT – should they cut? Even as we are proponents of revisiting inflation targets, we just don’t see enough economic weakness to warrant a move to an accommodative (from currently neutral) stance – now that will be a true shocker!

FED Funds Futures Imply a "Near Certain@" Rate Cut in Sep

source: CME

.png)

%20(16).png)

.png)