Over the last few weeks, software has sold off on the notion that generative AI will commoditise application layers, crush seat-based pricing, and pull budgets toward infrastructure and models. Headlines amplified that view, and the tape obliged.

But the operating data tell a different story: the large enterprise platforms remain deeply entrenched, are growing contractual backlogs, and are converting more of those backlogs into cash—even as they re-package AI to expand SKU count and deal sizes. The “death of SaaS” narrative is neat and scary; it’s also incomplete.

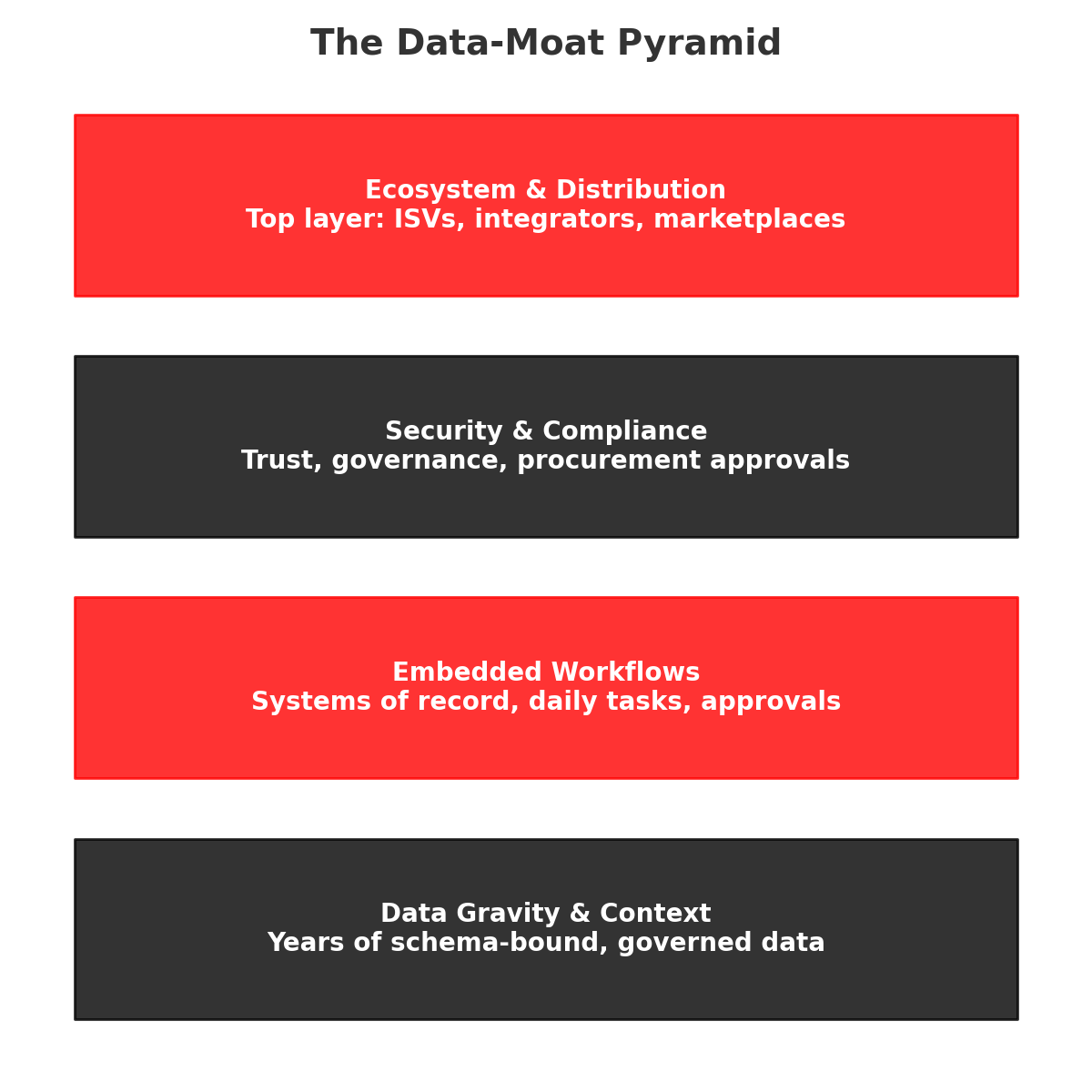

Why AI strengthens, not weakens, the incumbents

Enterprise apps are not generic chatbots—they’re systems of record, workflow engines, and compliance surfaces sitting on years of customer-specific data. That data—transaction logs, HR events, customer interactions, tickets, financial postings—are schema-bound, access-controlled, and riddled with edge-cases that only the incumbent platform “knows.” Incumbents therefore possess:

- Data gravity & context (clean, permissioned history to ground AI)

- Embedded workflows (where agents can actually do things, not just draft text)

- Distribution & trust (procurement, security reviews, SOC2/ISO, data residency)

- Ecosystems (ISV marketplaces, integrators) to scale new AI features quickly.

The result: AI features are being used to deepen moats - reducing low-value clicks, surfacing insights from owned data, and automating cross-app tasks—rather than to undercut the platforms that already run those tasks. Pricing is evolving (more usage/“assist” units on top of seats), but that evolution aligns revenue with value delivered rather than capping it.

Salesforce: bigger backlogs, cash engine intact, AI packaged for upsell

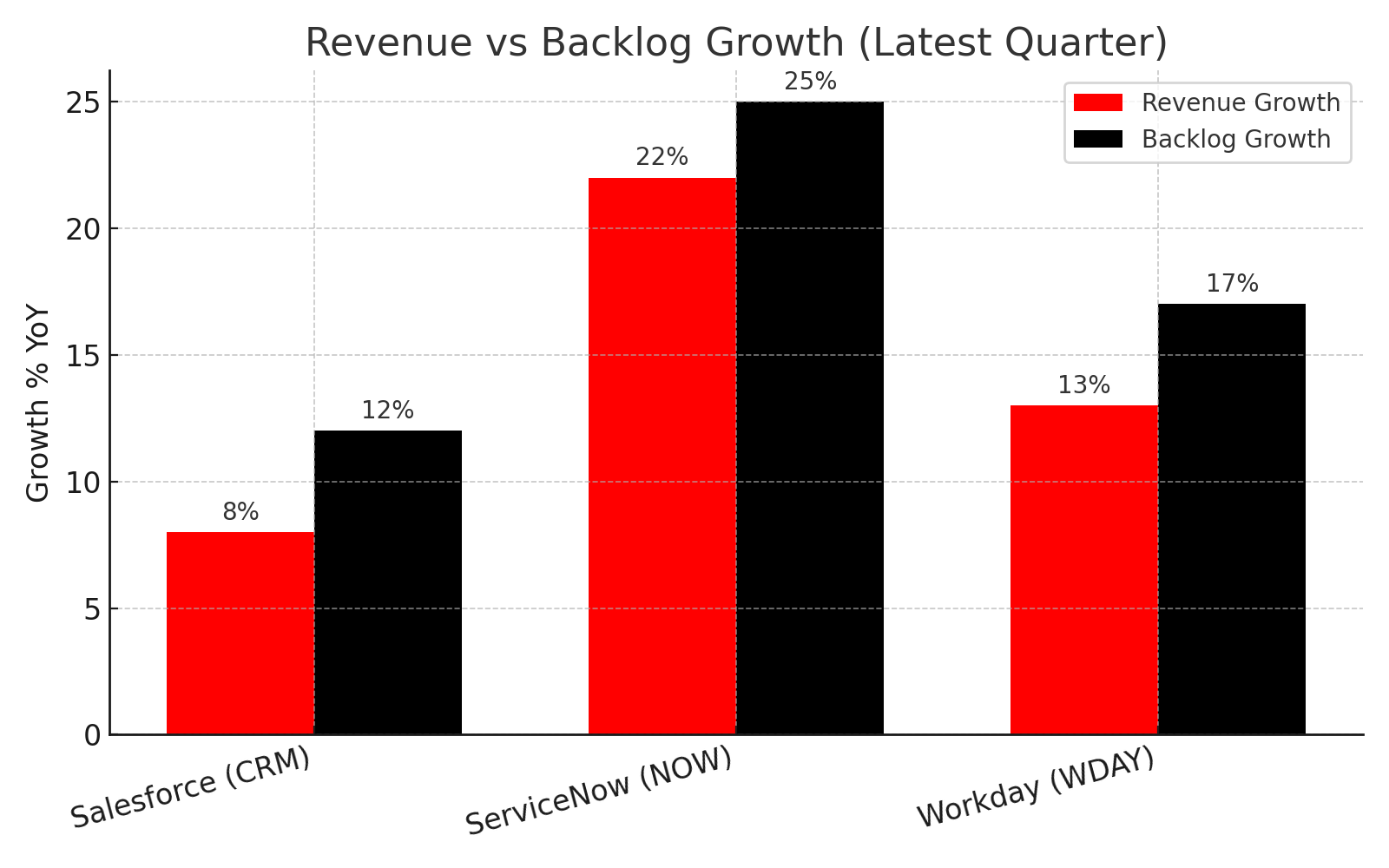

Salesforce’s latest print shows the core engine humming while AI is being monetised through Agentforce. Q1 FY26 delivered $9.8bn revenue (+8% y/y), current RPO of $29.6bn (+12% y/y), and $6.3bn FCF, plus $3.1bn returned to shareholders—all while holding mid-30s non-GAAP operating margins. That is not a business being hollowed out. On packaging, Salesforce introduced Agentforce add-ons from $125/user/month, with premium “Agentforce 1” editions starting at $550/user/month, a clear path to price/mix uplift as agent workloads expand across Sales, Service and Field Service. Early deployments also support consumption elements (per-interaction economics) layered on top of seats—a lever for ARPU as usage scales.

Read-through: Salesforce isn’t ceding the app layer to open models; it’s bundling agents inside governed workflows (case resolution, quote-to-cash, service deflection) where it controls the data, actions, and audit trail—i.e., the value.

ServiceNow: AI “assists” drive platform consolidation and larger deals

ServiceNow’s Q2-25 was a textbook “beat and raise”: subscription revenue +22.5% y/y to $3.11bn and cRPO +24.5% y/y to $10.9bn. Management explicitly tied momentum to AI-assisted workflows (“Now Assist”) that let customers consolidate point tools into the Now platform. Importantly, Now’s generative features are sold with seat-plus-usage constructs (assist capacity packs) that scale as automation expands across IT, HR and Customer workflows. This is the opposite of commoditisation; it’s platform share-gain.

Read-through: ServiceNow’s moat is execution in cross-department workflows and compliance-first automation. AI sits inside those controls, which is precisely where enterprises want it.

Workday: backlog compounding; AI agents formalised into the system of record

Workday’s latest quarter showed 12-month subscription backlog up 16.4% y/y to $7.91bn and total subscription backlog up 17.6% to $25.37bn, alongside double-digit revenue and EPS growth—even as near-term guidance looked conservative and the stock wobbled. Strategically, Workday has moved beyond “AI features” into an Agent System of Record—a governance layer to onboard, secure, meter and audit AI agents next to the human workforce—and just announced a deal to acquire Paradox, an AI recruiter, to deepen hiring and onboarding. That’s not being disrupted by agents; it’s managing them.

Read-through: If agents become ubiquitous, the vendor that governs agents inside HR/finance controls the budget conversation. Workday is angling to be that control plane.

Adjacent leaders reinforce the same pattern

- Datadog (observability/security) printed Q2-25 revenue +28% y/y to $827m, continued expansion in $100k+ customers (~3,850), and guided to low-20s growth—evidence that “AI infra” doesn’t just help chip vendors; it also lifts the software that monitors AI-heavy stacks.

- Atlassian is pushing Rovo—agents + search across the “teamwork graph”—while still growing mid-to-high teens at scale (FY25 total revenue growth guidance ~18%, cloud ~21%). Embedding agents into Jira/Confluence workflows is a classic incumbent-advantage play: existing data, permissions, and daily active use.

- CrowdStrike & Palo Alto Networks (security platforms) aren’t “classic SaaS” the way CRM/HCM are, but they’re instructive: both highlight rising ARR/RPO and “platformisation,” with AI detection/response engines increasing attach rates and deal sizes—another case of AI expanding, not compressing, application value.

Pricing is evolving, but the model is not broken

Yes, AI tilts vendors toward hybrid pricing—seats + usage (tokens/assists/requests)—to match compute costs and value delivered. Investors worry that usage adds volatility to ARR. In practice, the shift creates more monetisation surfaces (per-agent, per-assist, per-workflow) layered on top of existing enterprise agreements. Salesforce’s Agentforce tiers (add-on from $125/user/month; premium editions starting $550) and ServiceNow’s “assist” capacity packs are concrete examples of this repackaging—designed to scale with adoption while keeping procurement simple.

The market’s fear vs the numbers

Breakingviews framed the core bear case crisply: SaaS index growth has slowed from >20% to high-single digits, and AI specialists can undercut incumbents. But that view often assumes customers will rip out deep workflows to save on point features. In reality, the data above show backlogs compounding (CRM/WDAY/NOW), double-digit subscription growth, and robust FCF—exactly the metrics that matter when evaluating durability through platform transitions. The selloff looks driven less by collapsing fundamentals than by multiple compression and guide-conservatism in a jittery tape.

What to watch next (to test the thesis)

- Backlog vs conversion: cRPO/12-month backlog growth needs to keep outpacing revenue—so far, it is at CRM/NOW/WDAY.

- AI attach: Look for disclosures on agent seats, assist consumption, and AI-SKU penetration (Salesforce Agentforce, Now Assist packs, Workday agents).

- Margin guardrails: AI opex and inference costs should be offset by consolidation wins and higher-mix SKUs; note how CRM maintained >30% non-GAAP OM while ramping AI.

- Procurement pattern: Consolidation beats bricolage. ServiceNow’s deal sizes and Datadog’s $100k+ cohort growth are the tells.

Conclusion

AI is not killing enterprise software; it’s giving the category new ways to monetise the data and workflows they already own. The platforms with the best data context, governance, and distribution—Salesforce, ServiceNow, Workday, and select adjacencies—are using AI to entrench themselves further. As fear cools and disclosures around AI attach build, the gap between narrative and numbers should narrow.

%20(16).png)

.png)

.png)