Executive Summary

TSMC’s Q4 2025 earnings and forward guidance mark a clear inflection point where AI-driven demand is no longer cyclical or speculative, but structural and accelerating. Gross margins north of 60% with guidance trending toward ~64%, combined with an unusually aggressive early-year revenue growth outlook (>30%) and a sharply higher capex envelope, strongly reinforce the view that TSMC has entered a monopoly-like phase in advanced AI manufacturing. Crucially, this is not just positive for TSMC itself—it validates massive forward demand visibility for AI chip designers and confirms a multi-year investment runway for advanced wafer-fab and test equipment suppliers.

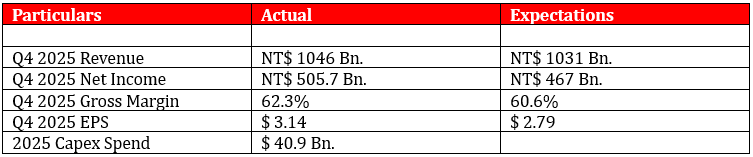

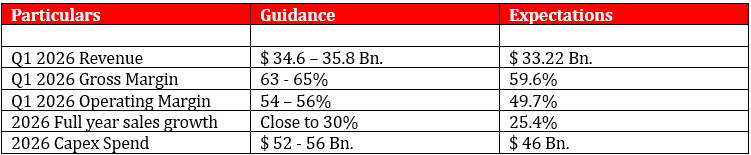

1. Key figures

Q4 2025

Q1 2026 & Full year Guidance

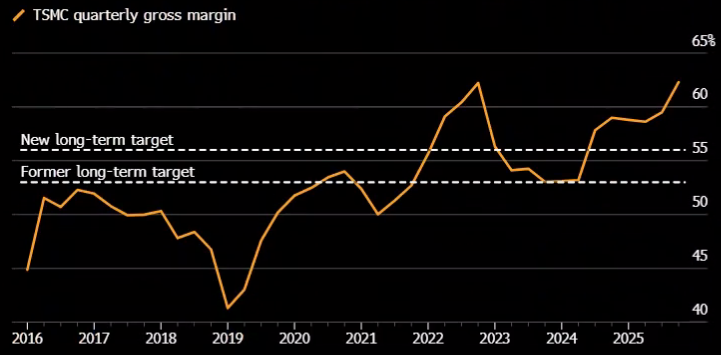

2. Monopoly Economics Are Now Explicit, Not Implied

TSMC has long been described as a “strategic bottleneck” in semiconductors, but Q4 2025 confirms that this bottleneck is now translating into true monopoly-style economics:

- Sustained gross margins above 60%, with further expansion guided into Q1 2026, indicate pricing power, not just utilization leverage.

- Advanced node scarcity (5nm, 3nm and below) combined with customer concentration in AI accelerators gives TSMC asymmetric negotiating power versus even the largest chip designers.

- This margin profile is historically unprecedented for a capital-intensive foundry business and reflects structural rent extraction, not peak-cycle behavior.

In effect, TSMC has moved from being a “best-in-class manufacturer” to a de facto monopoly supplier of advanced AI compute capacity.

3. Conservative Guidance + Early-Year Aggression = Demand Visibility Is Exceptional

One of the most important signals from this print is not the absolute numbers, but when and how they are being communicated.

TSMC has a decades-long reputation for conservative guidance. Against that backdrop:

- >30% revenue growth guidance issued at the start of the year is highly unusual and strongly suggests order books and long-term capacity reservations are already locked in.

- The ~US$54bn capex guide (≈30% YoY increase) reinforces that management is not reacting tactically, but building for sustained, multi-year demand.

- This implies AI demand is not merely extending—but potentially accelerating from an already large base, rather than rolling over after initial hyperscaler deployments.

This materially weakens the bear case around a near-term AI digestion phase.

4. Clear Read-Across to AI Chip Designers: Demand Is Being “Pulled Forward”

The most underappreciated implication of TSMC’s commentary is what it says about AI chip producers themselves.

Leading designers such as NVIDIA and Advanced Micro Devices do not commit capacity lightly—especially at advanced nodes with long lead times and heavy pre-payments. TSMC’s confidence strongly suggests:

- Large, binding purchase commitments are already in place, extending well beyond the next few quarters.

- AI chip vendors are planning for continued volume growth, not merely replacing or refreshing existing deployments.

- The demand signal is broadening beyond training into inference, networking, and system-level scale-out, requiring sustained wafer starts.

In other words, TSMC’s results effectively validate the revenue visibility and backlog strength of AI chip leaders, reducing uncertainty around medium-term growth expectations for NVIDIA, AMD, and other advanced-node customers.

5. Second-Order Winners: Wafer-Fab, Packaging & Test Equipment

The scale and timing of TSMC’s capex plans have important second-order effects:

Wafer-Fab Equipment (Advanced Nodes)

- ASML remains indispensable for EUV scaling, and TSMC’s spend trajectory reinforces sustained demand for both EUV and supporting DUV systems.

- Advanced logic scaling keeps process intensity high, benefiting tool suppliers across lithography, deposition, and metrology.

Advanced Packaging & Back-End

- AI chips increasingly rely on advanced packaging, chiplets, and heterogeneous integration, areas where capex intensity per wafer continues to rise.

- BE Semiconductor Industries is particularly well positioned given its exposure to advanced packaging and hybrid bonding.

Test & Inspection

- Higher-value, higher-complexity AI devices drive increased testing and yield-management requirements.

- This bodes well for KLA Corporation, Advantest, and Hon Hai Precision Industry across inspection, testing, and system-level validation.

6. Bigger Picture: The AI Cycle Is Becoming Infrastructure-Like

Stepping back, TSMC’s Q4 print reinforces a crucial shift in how AI should be framed:

- This is no longer a discretionary tech cycle, but an infrastructure build-out, analogous to cloud computing or mobile broadband.

- Capacity is being added ahead of demand, not in response to short-term spikes.

- Profit pools are increasingly concentrating at structural choke points—with TSMC at the very center.

For investors, TSMC’s results and forward investment plans strengthen the case that AI-related spending is becoming increasingly embedded in long-term capital allocation decisions, rather than being driven solely by near-term momentum.

.png)

%20(14).png)

.png)