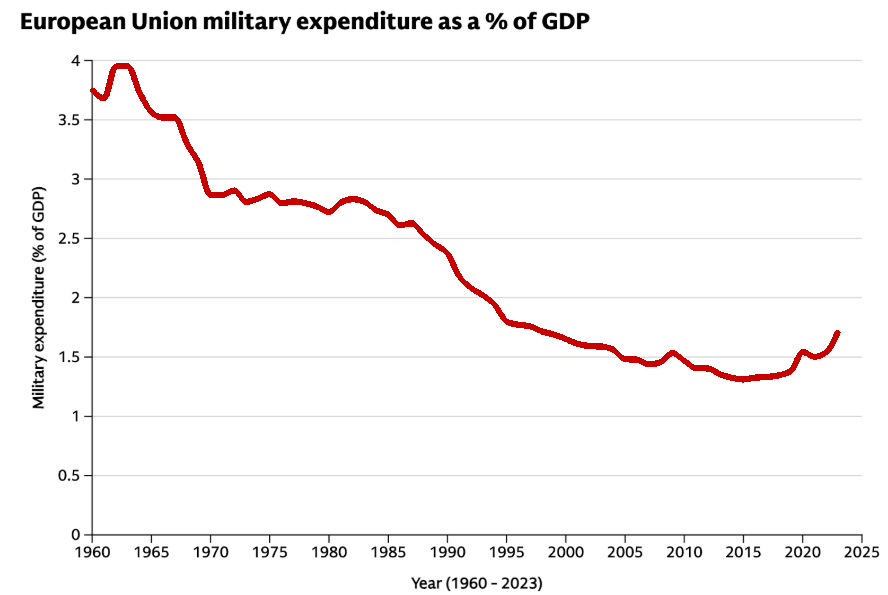

Defense has emerged as one of the most important secular themes in global markets today. The Russian invasion of Ukraine has permanently altered European defense policy, leading to an unprecedented commitment to rearmament across the continent. Germany, long criticized for underinvesting in defense, has now pledged to meet and maintain the NATO target of spending 2% of GDP on defense—translating to over €100 billion in incremental spending through the coming years.

Meanwhile, the European Union has committed to launching a series of joint defense procurement initiatives, aimed at strengthening regional interoperability and reducing reliance on external powers. These developments signal the start of a long-term capital cycle for defense infrastructure, equipment, and technology.

Further, at the 2025 NATO Summit in the Hague, member states agreed to a 5% target by 2035, including 1.5% for defense-related matters like cyber security and infrastructure, which provides additional signs that this is a market that is likely to keep growing at a solid pace for many years to come.

.png)

2035E: Baseline 2% of GDP, assuming GDP remains stable (Black) + Extra 3% of GDP needed to reach the 5% Target set at the NATO Summit (Grey)

Crucially, this realignment is not limited to the continent. The United Kingdom recently signed a landmark trade agreement with the European Union, the first of its kind since Brexit, which allows UK-based defense firms to bid on EU-led projects. This creates a new strategic bridge between UK industrial capacity and European defense ambitions.

In this piece, we highlight four companies that are positioned to benefit from this structural re-rating of defense budgets and policy coordination:

- From the UK: Rolls-Royce Holdings and BAE Systems

- From Continental Europe: MTU Aero Engines and Airbus

Each of these names provides differentiated exposure to the buildout—across aerospace, propulsion, systems integration, and next-gen defense platforms—while still offering relative valuation appeal compared to the more crowded German defense complex.

UK Defense: New Opportunity in the Post-Brexit Era

The recently signed trade agreement between the United Kingdom and the European Union, the first such deal since Brexit, opens up an important new avenue: UK-based defense firms can now bid for large EU-led defense projects, a development that significantly enhances their addressable market.

Two standout names in this context are:

- Rolls-Royce Holdings (RR/ LN): Best known for its civil aerospace business, Rolls-Royce is also a critical player in the defense engine and propulsion space. The potential to expand into EU contracts complements the company’s restructuring and operating leverage story.

- BAE Systems (BA/ LN): The UK’s largest defense contractor is already a beneficiary of rising global defense budgets. The new trade agreement boosts its relevance further, giving it the ability to tap into European defense projects while retaining strong ties with U.S. and Middle Eastern clients.

These names offer investors exposure to a sector with rising budget allocations and high visibility, but without the valuation stretch currently visible in the German defense complex.

Continental Europe: MTU Aero Engines & Airbus

- MTU Aero Engines (MTX GY): MTU plays a crucial role in the European defense ecosystem as the lead developer of the EuroJet fighter’s propulsion system. It is well-positioned to benefit from greater pan-European coordination in defense R&D and procurement. Meanwhile, its commercial R&M business provides a solid annuity-like stream of cash flows that smooths earnings volatility.

- Airbus (AIR FP): While Airbus is best known for its commercial aviation segment, which is underpinned by a backlog of over 7,000 A320 aircraft, its Defense & Space segment is turning into an increasingly strategic asset. With profitability expected to improve in the coming years, this segment could become a more meaningful contributor to earnings and help narrow the valuation gap versus U.S. peers.

Together, these companies represent a compelling way to participate in the European rearmament theme without simply following consensus trades. With rising geopolitical risks and strong political will across NATO and the EU, we believe the next leg of defense outperformance could come from these under-owned yet strategically important players.

%20(16).png)

.png)