Burnt by an economy that continues to show resilience, most economists and market watchers have given up calling for a recession/ downturn, despite multiple slowdown signs and increased uncertainty. Opinion makers have all but given up on previous cycle markers, ranging from yield curve inversion, Sahm rule etc, amidst the backdrop of an elusive recession, despite the fastest rate raising cycle. Even the FED's knee-jerk rate reaction (on hind sight) in late 2024, in response to weaker labor data, has proven unfounded as yet - no wonder they remain on the side-lines.

We believe that consumer spending, the linchpin of the economy, will remain supported as long as the jobs market does not crack - and that has been super resilient. Of course any agency reporting weakness in labor data risks being fired for cause! Dark humor aside, even as employers have slowed hiring, lay-offs remain contained, supporting consumption - have job, will spend!

In the week ahead, focus will be on inflation (moderate increase/ steady) and retail sales in the US. In China, deflationary woes are persisting China even as credit growth picks up. In India, inflation is expected to have eased further. As for earnings, bulk of reporting is behind us.

Have Job - Will Spend

Retail Sales Have Remained Resilient

.png)

Source: Trading Economics

- Consumption, representing some two-thirds of US GDP, has been a resilient source of strength and is well captured in the retail sales data, continuing to rise at a steady pace. Without a meaningful retrenchment in consumption, its difficult to see a meaningful downdraft in economic activity

- Housing has been weak...Elevated mortgage rates, inflationary pressures, have all contributed to a steady weakness in the housing market. While consumption decisions do get influenced by the wealth effect/ asset prices, ultimately it is future cash flow confidence that drives consumption and investment decisions - jobs thus become the key focus rather than asset prices.

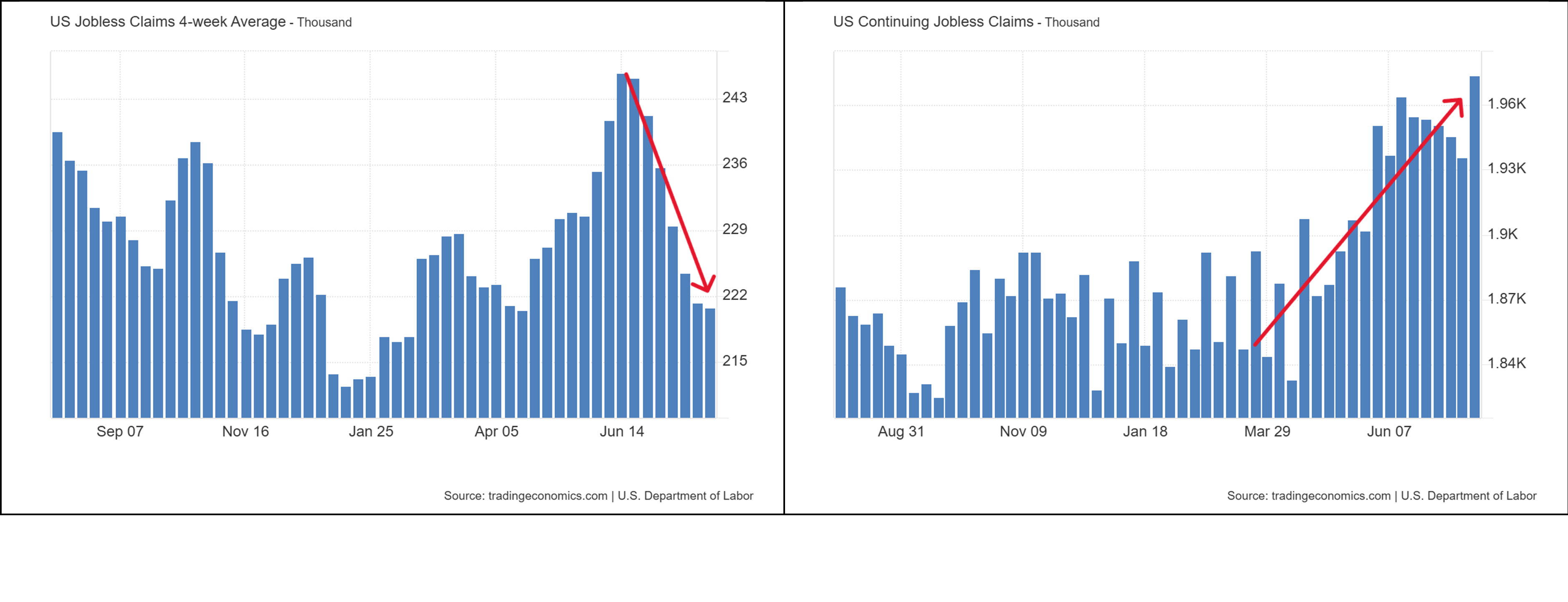

- Jobs - Easing, but only moderately - A steady increase in continuing jobless claims, despite declining initial jobless claims suggests a combination of (a) fewer layoffs (hence fewer initial claims) and (b) difficulty in finding jobs (rising continuing claims). Essentially, whether its uncertainty caused by tariffs or interest rates, employers appear to be reluctant to either fire or to hire.

- What About Revisions? - A substantial (downward) revision to payrolls data spooked markets early August. While revisions, and these have tended to be downward in recent years, have been a common feature, the scale of revisions is clearly a cause for concern. That said, firing the chief of BLS is unlikely to solve what does appear to be a steady, moderate, slowdown in the jobs market.

Initial Jobless Claims Falling even as Continuing Claims are Rising - Fewer Layoffs, BUT, Fewer Hires too

Source: Trading Economics

Unemployment Rates Have Largely Been Steady as a Result

.png)

Source: Trading Economics

Week Ahead in Markets

- US Macro - CPI (Tuesday, 11th Aug) is expected to be steady as is PPI (14th Aug, Friday). Retail sales (Friday, 15th Aug) expected to decelerate slightly after a sharp spike in Jun, but remain elevated vs. recent months. Consumer confidence (Friday, 15th Aug) also expected to remain steady.

- China reported inflation data on the weekend with a slight improvement in CPI (0% vs. 0.15 contraction expected) - month on month figures were more encouraging at 0.4% vs. expectations of 0.3%. However, producer price deflation persist (PPI -3.6%, same as before and worse that then 3.3% expected). Focus will be on credit growth (Thursday, 14th Aug) expected to have risen further to 7.2% (vs. 7.1%) and money supply to have risen in tandem. Friday, 15th Aug will see retail sales data (expected at 5% vs. 4.8%), and house price index, still expected to decline, but at a slower pace.

- India reports inflation data on Tuesday, 12th Aug, expected to report further easing.

Earnings Season - All But Done

- June 2025 earnings season is mostly done with over 90% of companies having reported, trending EPS growth at 11.8% vs. c5% expected as at end Jun, marking a substantial beat and close to the c13% delivered in the March'25 quarter. Similarly, revenue growth accelerated to 6.3%, also much ahead of the 4.2% consensus at the beginning of the reporting season. Margins at 12.8% were also higher vs. 12.2% a year ago. Full year 2025 earnings and revenue growth forecasts have consequently been revised upwards to 10.3% and 5.8% respectively.

- Earnings misses have seen a larger negative impact (vs. positive impact on beats), in a return to the familiar pattern of 2024. That the bar for beats was low, is also likely the reason for this skew.

Earnings Estimates for 2025 Revised Upwards to 10.3% growth

Source: Factset

Earnings Revisions - Trending Upwards

Source: Factset

No items found.

Subscribe to our Insights & Updates

Oops! Something went wrong while submitting the form.

%20(16).png)

.png)