In what was expected to be a “quiet” summer month, August has started with a bang, skidding on labor data weakness, renewed sabre rattling with Russia and more posturing on tariffs. Investor skittishness is evident in skewed reactions to earnings, after one of the fastest “V-Shaped” recoveries on record – is it a case of “bought expectation/ selling fact”? Perhaps. While major indices are still holding above a critical breakout threshold, the rejection of an all-time high breakout for the “Mag-7” is coincident with proprietary model signalling “take profits” - a trigger for adding hedges.

With two-thirds of S&P companies already having reported (growth trending at 10%, ahead of5% consensus), and a relatively light macro data week, there are limited catalysts although geopolitics and tariff shenanigans have the capacity to lift volatility from its somnolence.

While higher volatility will provide opportunities, for now, derivative strategies are attractive to lock in gains. Gold remains stuck in a range – watch for any decisive breakouts above 3450. Meantime, treasuries preferred over corporate bonds.

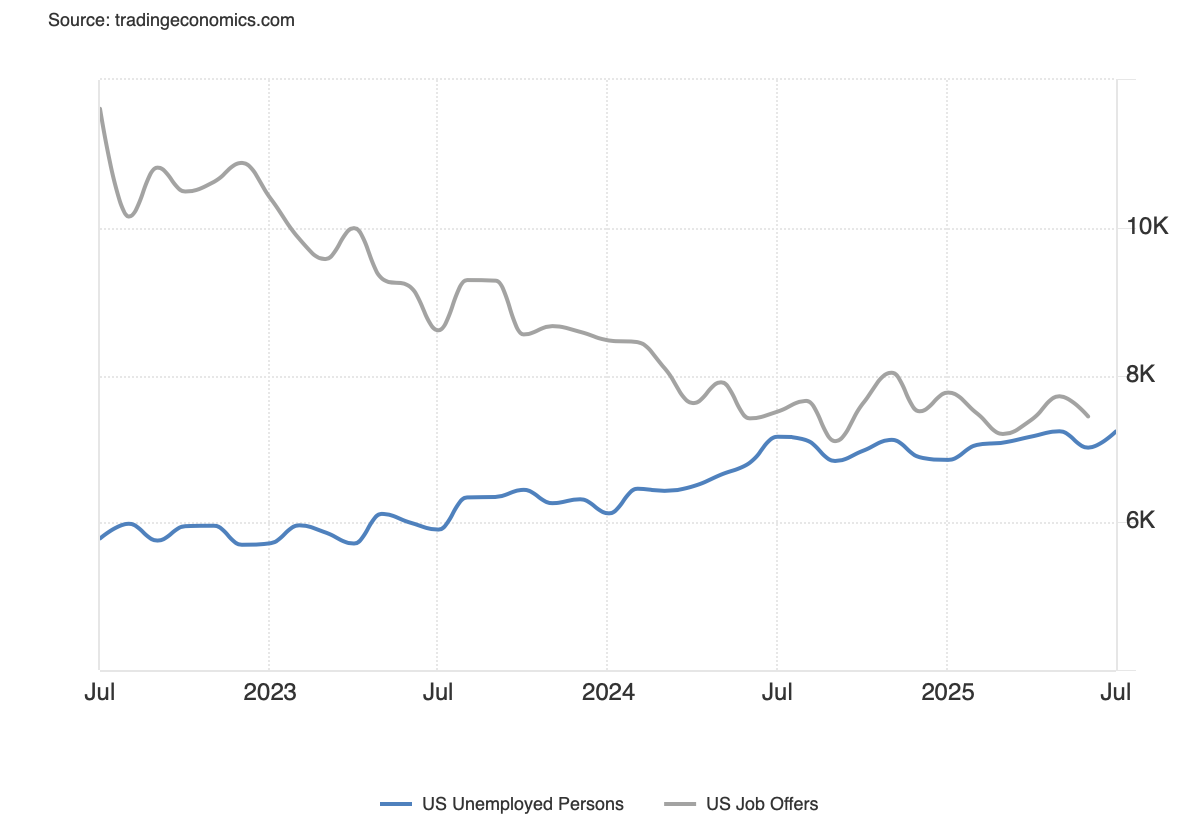

Jobs – the Last Nail?Eventually, but Not Yet

Narrowing gap between unemployed persons and job openings

Source:Trading Economics

Signs of a slowing economy – weaker housing, consumption, business activity, have thus far been stitched together by a resilient labor market. No surprise then that a weak payrolls release acted a final straw for a market already unnerved by tariff and geopolitical uncertainties.

The big question for investors will be whether this is the final data point that breaks the economy and the market? While we have long held, and still do, that labor markets hold the key, and no doubt the trajectory is weakening, evidence thus far is of a graduated easing rather than air pockets.

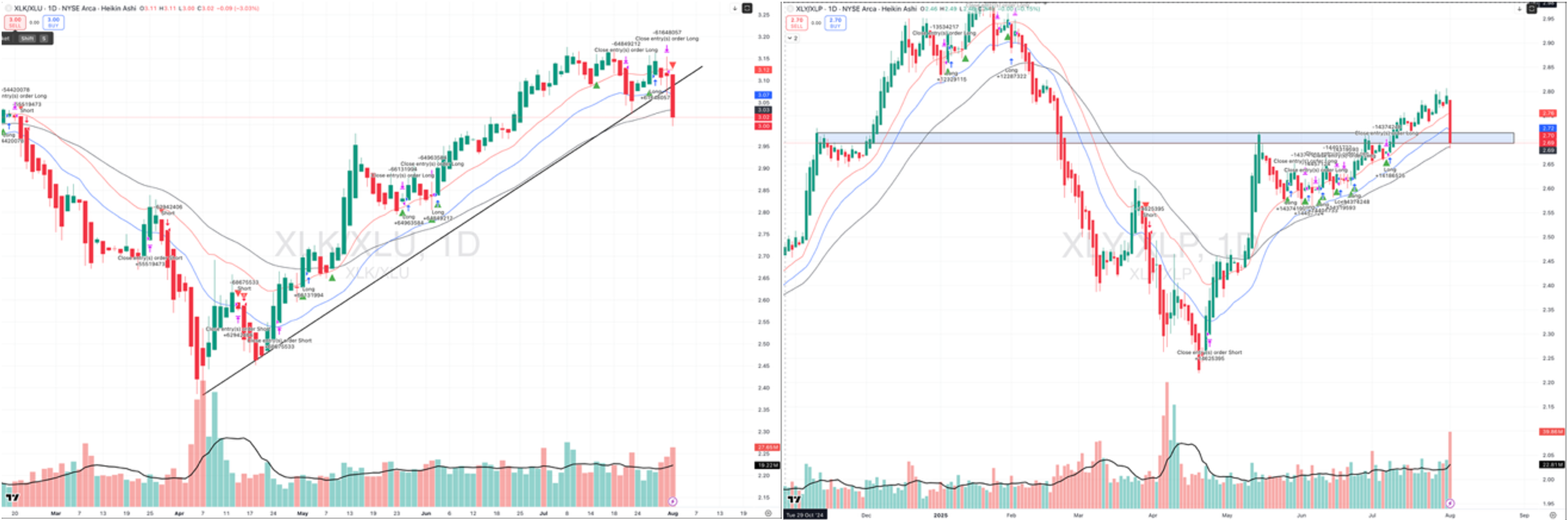

“Take Profits”Signalled

The proprietary model has triggered a “take profits” signal

Source:Trading View

Our proprietary market signals model has largely been in a “buy” mode over the last three months but has now triggered a “close long positions” signal. The same signal is evident on 10 of 11 GICS sectors, absolute and relative, with Utilities being an exception. Amongst major sector indices, notable cracks are evident in tech, the linchpin of the “V-shaped” recover since April lows. The shift to a defensive stance combined with weakness in the bellwether growth sectors is a cause for concern for the bull market. Despite the latest wobble, major indices are still holding above recent breakout levels (6150 for SPX) – defending these will be critical for the bull market agenda.

Tech vs.Utilities and Discretionary vs. Staples – Rolling Over…

Source:Trading View

Week Ahead in Markets

MacroData

- US – PMI data (5th Aug) expected to show a pick up.

- UK & Europe – UK Rates decision (7th Aug) expected to be for a further 25bp cut to 4% in BOE base rate. In Europe, watch for PPI (5th Aug) for a small pick up and retail sales (6th Aug) rebound.

- China releases PMI (services expected to pick up) on5th Aug and inflation data (deflationary trends) on 9th Aug.

- India also releases PMI (moderate easing) on 5th Aug and RBI rate decision (unchanged) on 6th Aug.

Earnings

- Earnings Thus Far – 66% of S&P companies have reported with over 80% beating consensus. EPS growth is trending at 10.3% vs.5% expected at the start of reporting season. With margins continuing to rise, consensus for 3Q and the full year has seen an upward revision to 7.6% (vs. 7.3%) and9.9% (vs. 9.1%) respectively. source: Factset

- The Week Ahead – Over 100 S&P constituents are expected to report in the week of 4th Aug. While market heavy-weights have reported (except NVDA), there is significant reporting yet to come. Of the 58 major companies reporting next week, positive earnings expected from 64% of these names and positive revenue trends from nearly 75%. While Monday, 6th Aug will be most impactful from a market cap perspective, Thursday will be critical for healthcare companies, having recently borne the brunt of regulatory pressures.

Source: Trading Economics

%20(16).png)

.png)