Central banks and regulators are still solving for the ghosts of the GFC, even if it’s been only 17years. The classic response to a crisis is to solver for the last one, while its never the same, and certainly not the next time. Basel IV adds to an already over-layered capital structure, and that is a larger challenge for European banks, especially when compared to the US major banks, where regulators have taken on a more pragmatic approach. While its arguable as whether US regulators have been blasé, the reality is that solving for more capital wasn’t the antidote as exemplified in the 2023 Credit Suisse debacle. Paraphrasing and old saying, irrationality can last longer than solvency.

The new framework (expected to be implemented at different dates across jurisdictions), is designed to strengthen financial institutions, appears to be a refined version of the cruder Basel1 framework.

Who Gets Impacted (and Who Doesn’t)

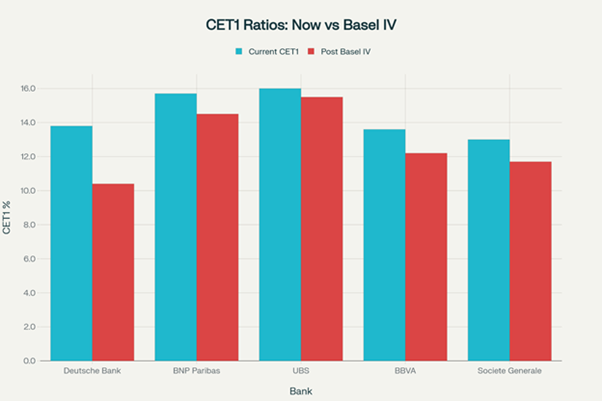

Deutsche Bank appears most impacted amongst major banks given reduced buffers above regulatory minimums and increased risks of coupon suspensions. Deutsche Bank Perpetuals, already not preferred by Lighthouse Canton), are likely to see further spread widening.

- Banks that relied heavily on Internal Risk Models will likely see the largest adverse impact, notably Deutsche Bank with near 4% decline in CET 1,although still a respectable 10%+ post the drop.

- Banks already using Standardized approaches (UBS and BNP) will see a minimal impact.

In summary:

Severe downturns or financial crises will likely magnify Basel IV’s downward pressure on reported CET1 ratios, while sustained economic growth and profitability provide relief.

The degree of capital shortfall and regulatory constraint will depend on both external macroeconomic shocks and the banks’ own adaptive strategies, making Basel IV’s final impact highly conditional on future economic developments.

This puts European banks at a competitive disadvantage relative to its US peers where steps are being taken to improve profitability of the banks although with increased risks.

Basel IV - Summary of Core Recommendations

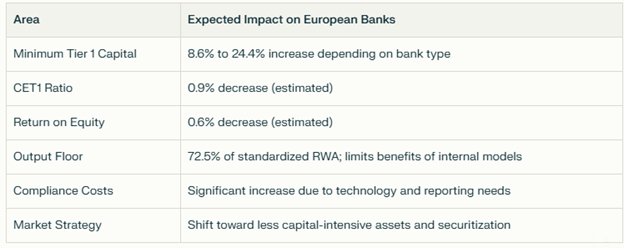

- Risk Weighted Asset Calculations- Floor of 72.5% of capital based on Standardized approach. For individual product categories as well, there are output floors (e.g.,mortgages at 20% - see next). While designed to be more granular and “risk-sensitive”, the framework’s reliance on blunt output floors and minimumsbased on Standardized approach make it appear more “one-size fits all” thangranular.

OutputFloor: A minimum threshold (set at 72.5% of standardized RWAcalculations) prevents banks from using internal models to significantly reducecapital requirements, ensuring consistent capital adequacy across banks.

OperationalRisk Overhaul: Internal models for operational risk are replaced by a single,standardized measurement approach, which factors in banks’ business size andhistorical losses.

MarketRisk and Trading Book: The Fundamental Review of the Trading Book introduces stricterassessment and reporting for trading activities.

Leverageand Buffers: There are new requirements for leverage ratios, especially forsystemically important banks, to reduce excessive risk-taking.

BaselIV: Detailed Recommendations

Reinforcingthe standardized approaches for credit risk,credit valuation adjustment (CVA) risk (the pricing of derivative instruments,for which a standardized or basic approach is now required) and operationalrisk, laying out new risk ratings for diverse types of assets, includingcorporate bonds and real estate. The Basel proposals provide for variouschanges that make standardized approaches more risk sensitive by adding moretiers, categories and requirements, thereby making standardized approaches morecomplex.

Restrictingthe use of IRB (Internal Risk Based Models) approaches to calculate capitalrequirements. Banks will have to follow the standardized approach unless theyobtain the supervisor’s approval to use an alternative. Basel IV removes theAdvanced-IRB (A-IRB) approach option for exposures to large corporate andfinancial institutions and removes all IRB approach options for equity.

Introducinga leverage ratio buffer to further limit the leverage of global systemicinstitutions (G-SIBs) by requiring them to keep additional capital in reserve.

Removingthe advanced measurement approach (AMA) forcalculating operational risk and replacing it with a non-modelled standardizedapproach.

Replacingthe existing Basel II output floor with a more risk-sensitive floor,reducing the low levels of internally modelled RWAs and allowing for a bettercomparability between standardized and IRB banks, reflecting the differencebetween the amount of capital that a bank would require to keep based on itsinternal model as opposed to the standardized model.

Thenew rules require banks to hold capital equal to at least 72.5% of the amountindicated by the standardized model, regardless of what their internal modelsuggests.

Underthe IRB approach, some asset classes, like retail mortgages, are currentlyassigned very low risk weights by many banks (about 10% on average). As aresult, IRB banks that are most heavily exposed to retail mortgages will beparticularly hit by the output floor, which will be based on standard riskweights ranking from 20% to 70%. On the other hand, since the output floor iscalculated on a consolidated basis, banks that are more diversified might beable to offset RWA shortfalls on some asset classes by RWAs above the outputfloor on some other classes.

Source:Moody’s

Regulatory and Implementation Timeline

Phased Rollout: The EU willimplement Basel IV reforms from January 2025 (via CRR 3 and CRD 6), withcertain transitions (such as the output floor) phased in until 2030, and someexposures (like mortgage loans) until 2032, giving banks some time to adapttheir strategies.

The United Kingdom has delayed theimplementation of Basel IV (referred to locally as Basel 3.1) regulations. Thelatest official timeline sets the new implementation date for 1 January 2027.Full implementation, including transitional arrangements like the output floor,is expected to be completed by 1 January 2030.

New Reporting Areas

Basel IV introduces stricter reporting foremerging issues such as shadow banking, crypto assets, non-performingexposures, and ESG risks, requiring significant upgrades in data management andtransparency.

ANNEXURE - EVOLUTION OF BASEL FRAMEWORKS

TheConception of Basel IV

Afterthe financial crises of the early 21st century, the Basel Committee on BankingSupervision (BCBS) launched Basel IV. This initiative seeks to correct flaws inthe existing framework and strengthen banking sector stability.

Theaims of Basel IV

ReduceRWA volatility: Basel IV aims to decrease the variability of risk-weightedassets (RWA), thereby enhancing resilience within the banking sector.

Enhancerisk sensitivity: By introducing a more granular approach to risk-weightcalculations, Basel IV promotes a sensitivities-based framework to account forcomplex risk profiles.

Limitdiscretion in internal models: To reduce RWA variability,Basel IV restricts the use of internal models for certain exposures, ensuringmore consistent RWA assessments.

Implementoutput floors: Basel IV sets a minimum threshold for RWAs calculated byinternal models, establishing a stronger base for institutional riskevaluation.

Key Structural Features:

Perpetual instruments with no fixed maturity

Loss-absorption mechanism triggered if CET1 ratio falls below predetermined thresholds (typically 5.125% or 7%). These mechanisms vary across issuers with Permanent write-downs, Temporary write-downs and Equity conversions as options. Recently we have observed a trend with issuers moving from Permanent write-downs to Equity conversions (e.g. UBS AT1s) as well as Temporary write-downs to Equity conversions (e.g. BNP AT1s). Such measures reduce the risk premium that surged post the Credit Suisse AT1 write-off.

Regulatory capital qualification under Tier 1 requirements

Call dates in these securities provide the issuers with an option to call that bond back. With the exception of few, most issuers call their instruments back as that implies ability to refinance at lower rates and hence credit positive.

European regulators created a specific "resolution" regime for AT1 bonds, distinguishing them from similar instruments in other markets like the US. This unique regulatory approach has shaped the development and characteristics of the European AT1market.

Fundamental Analysis

1. Liquidity Position and Deposit Dynamics

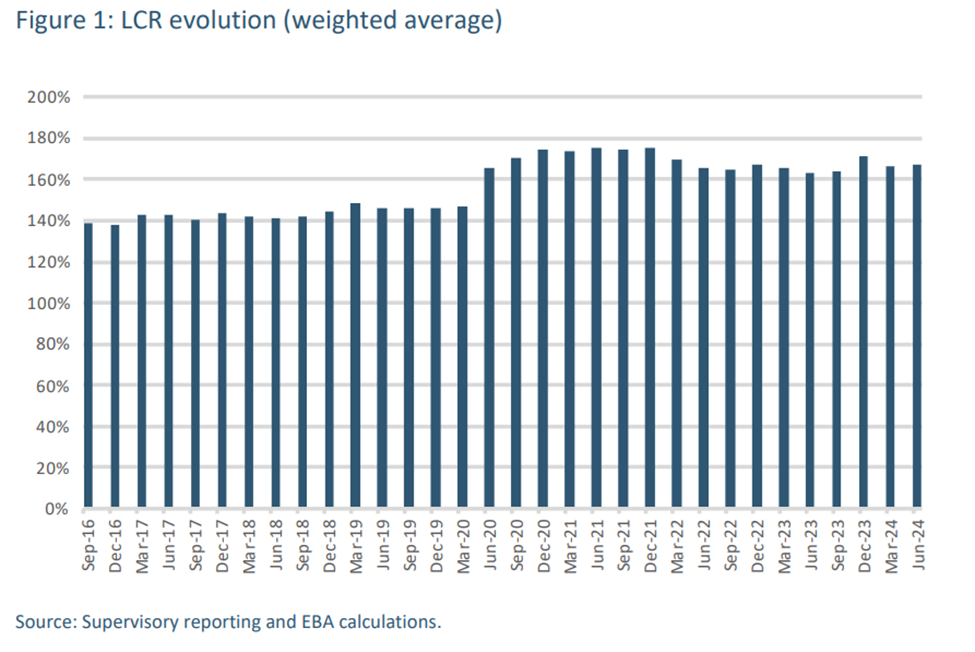

Liquidity coverage requirements are intended to ensure banks’ short-term resilience to potential liquidity disruptions. Banks should hold liquid assets to cover net liquidity outflows over a stress period of 30 calendar days and should maintain an LCR of at least 100%. 9 The LCR minimum requirement was set at 60% on 1October 2015 and it reached 100% at the end of the implementation period on 1January 2018.

LCR values reached 167% in June 2024, up from a level of 164% as of June 2023. Liquid assets increased while net outflows remained stable. All groups of banks increased liquid assets throughout the period under review.

LCR increased for retail-oriented banks, other specialized banks and other banks but decreased for corporate-oriented lenders.

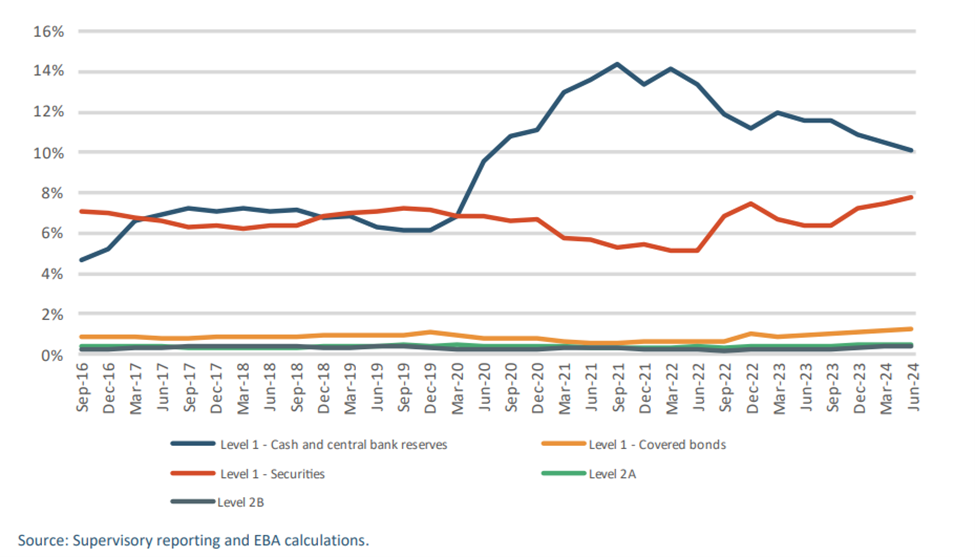

Liquid assets increased between December 2023 and June 2024 (liquid assets represented 20% of total assets as of December 2023 and 20.06% as of June 2024). The increase arises mainly from the securities component, followed by Level 1 covered bonds and Level2 assets. Cash and central bank reserves declined mainly due to the gradual decline of central bank reserves.

Evolution of the composition of liquid assets relative to total assets.

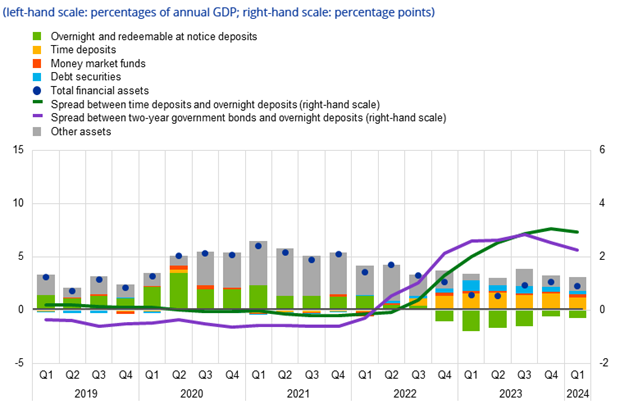

Corporate deposits have shown strong growth. Since 2010, corporate deposits in the European Union have risen by an average of 6.6% annually, outpacing the 3.9% growth in retail deposits. During the COVID-19 pandemic, annual growth in corporate deposits surged to around 20%4.

Deposit competition has intensified. As interest rates increased in 2022-2023, there was a migration toward remunerated and fixed-term deposits. However, this trend largely stopped in the first half of 2024.

The COVID-19 pandemic had a major impact on deposit movements, with more significant shifts observed during this period compared to subsequent events like Russia's invasion of Ukraine or the March 2023 banking turmoil.

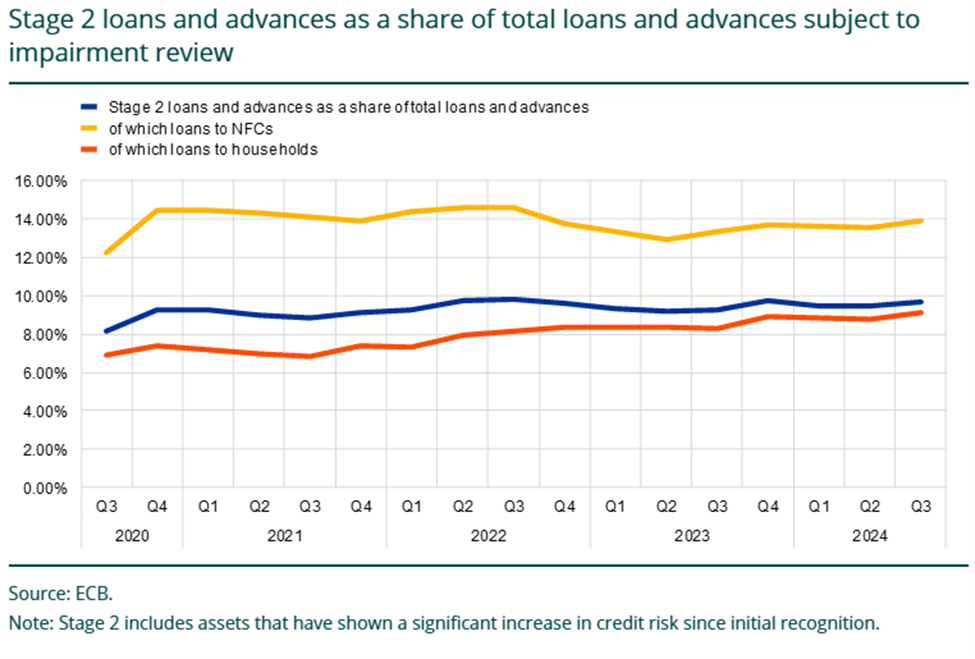

2. Asset Quality

Total eurozone bank lending is forecast to grow 3.1% in 2025 and 4.2% in 2026, up from just 0.2% over 2023 and2024.

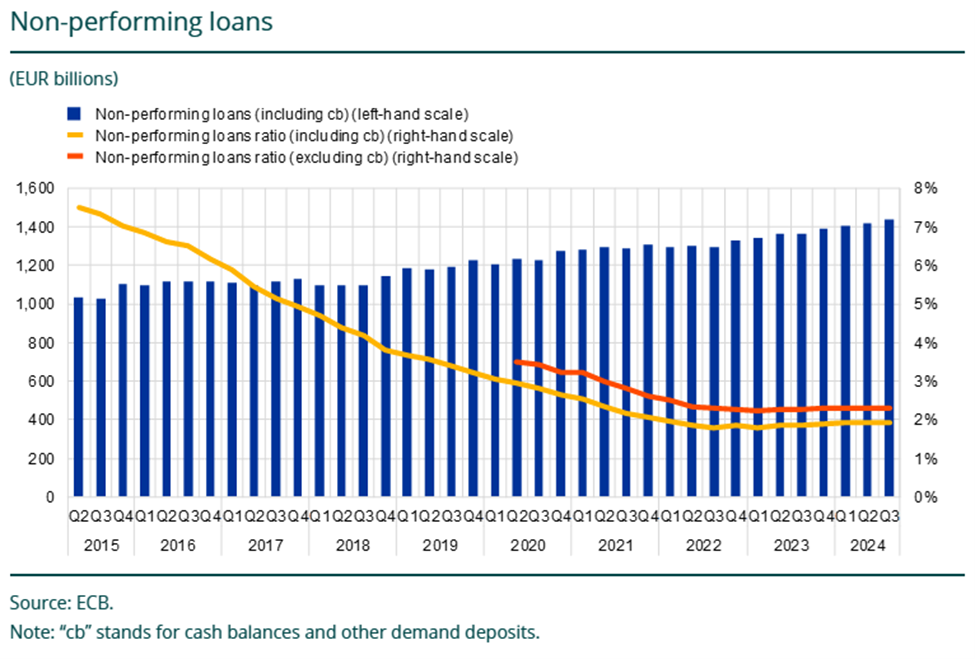

Non-performing loans (NPLs) a share of total loans across the eurozone are forecast to rise to 2.3% in 2025and 2026, up from 2.0% in 2024.

Consumer credit in Europe is forecast to rise 3.0% in 2025, 4.2% in 2026, and 3.9% in 2027.

Commercial real estate (CRE)loans account for around 10% of overall bank lending in Europe.

The euro area banking sector maintained solid capital and liquidity positions in 2024, well above regulatory requirements, thanks to the tighter lending standards and reduced bank appetite.

Large European banks' commercial real estate (CRE) loan books are diversified, which helps mitigate CRE risk.

3. Profitability

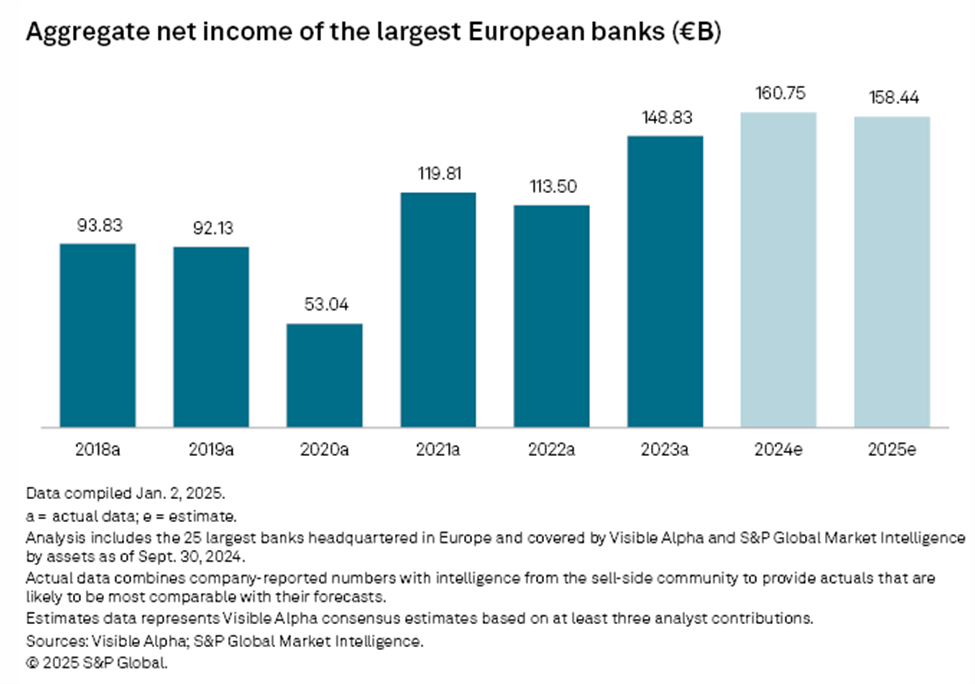

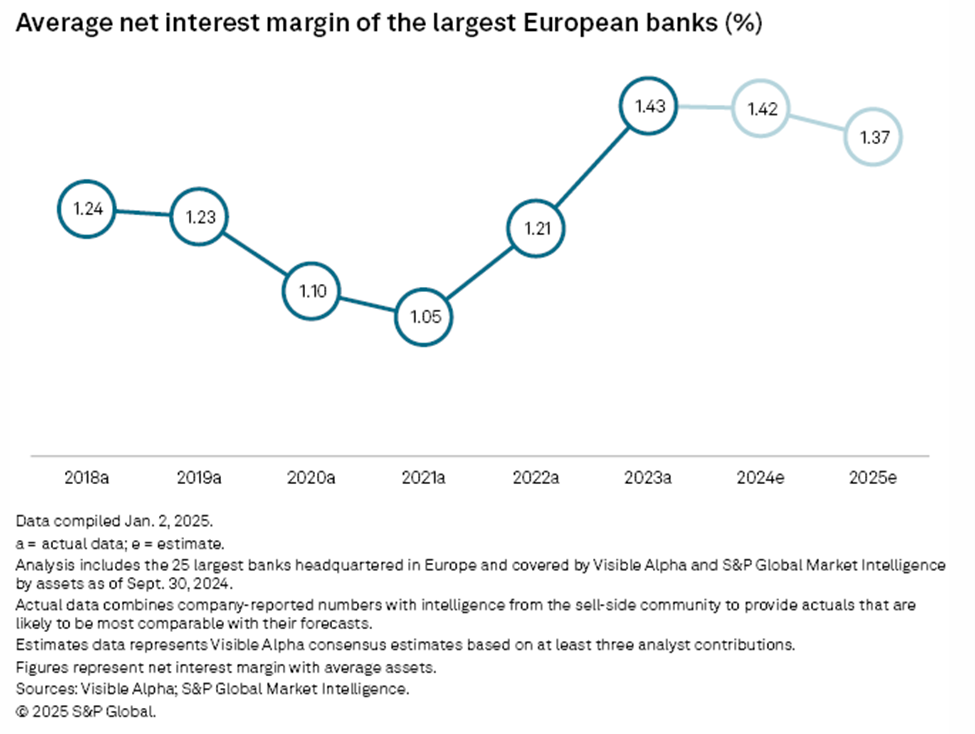

Europe's largest banks could lose out on profit of at least €2.3 billion in 2025 as they grapple with headwinds from a lower-interest-rate environment, S&P Global Market Intelligence estimates indicate.

Net income at the continent's 25 biggest banks by assets will reach an estimated €160.75 billion for 2024, a figure projected to fall by close to 1.44% in 2025.

A "moderate decline "in European banks' pre-provision income is "inevitable" in 2025 and2026 because of lower deposit margins as short-term interest rates decline, according to an S&P Global Ratings report.

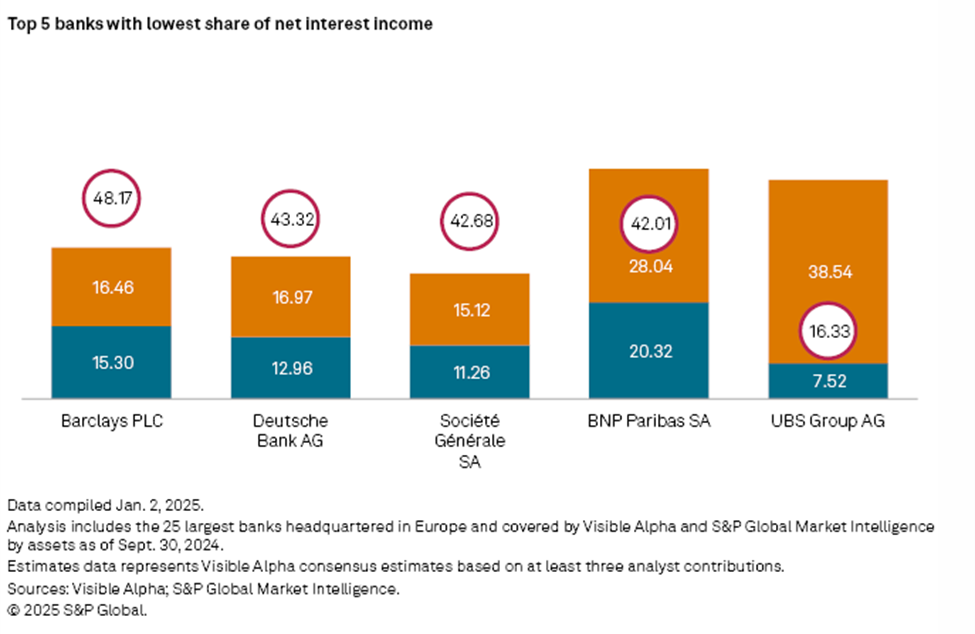

With lower rates, banks less reliant on NII are better off.

4. Balance Sheet Health

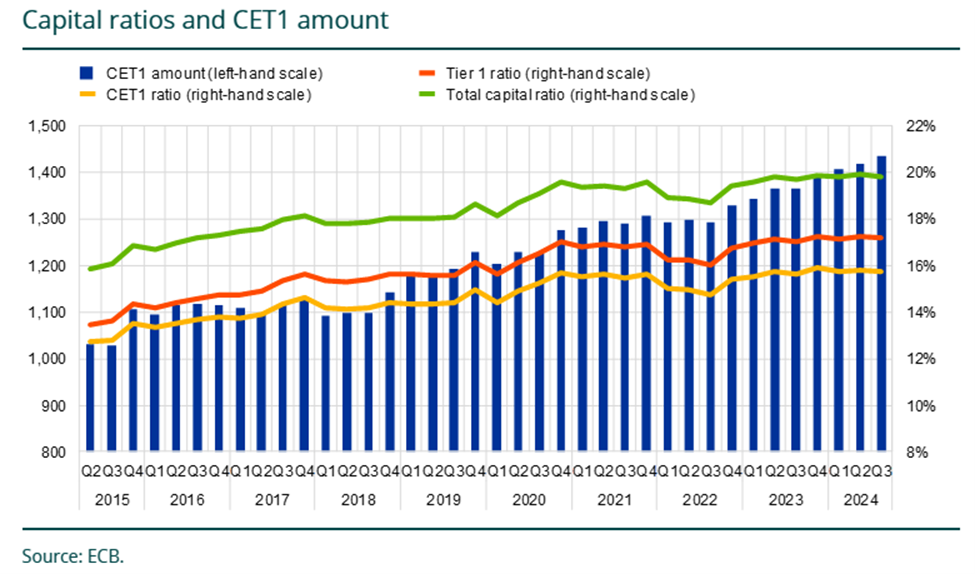

European banks' balance sheet health, as reflected in their AT1 (Additional Tier 1) instruments, remains robust in early 2025. This is characterized by Strong Capital Positions (Common Equity Tier 1 -CET1) ratio for euro area banks improved to 15.8% in mid-2024, well above regulatory requirements.

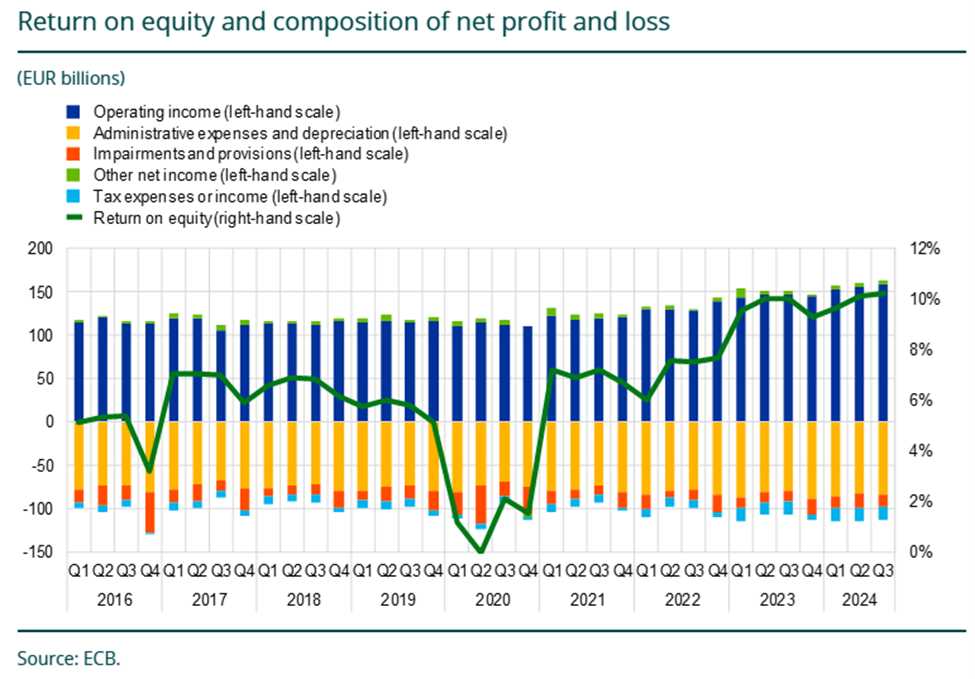

Along with-it corporate profitability has remained strong post-pandemic, contributing to the overall health of bank balance sheets.

In conclusion, European Bank AT1s continue to play a crucial role in banks' capital structures as we enter 2025. Despite facing challenges in 2024, the market has shown resilience and adaptability.

Key points to consider:

- Robust issuance: BBVA's recent $1 billion AT1 issuance with a 7.75% coupon demonstrates an ongoing investor appetite for these instruments.

- Regulatory support: European regulators have reaffirmed the importance of AT1s in bank funding structures, providing clarity on loss-absorption mechanisms.

- Upcoming redemptions: €15 billion AT1 bonds are set to mature in 2025, potentially driving new issuances.

- Market outlook: Expectations of lower interest rates in 2025 and banks' strong balance sheets are likely to support continued investor demand for AT1s.

- As the European banking sector navigates economic uncertainties, AT1s remain a vital tool for capital management, offering both challenges and opportunities for issuers and investors alike.

All investments carry risk, for more important information please read this disclaimer.

.png)

%20(16).png)

.png)