6.67% BIOCON 2029

Biocon Biologics is a global leader in biosimilars, serving over 5.8 million patients annually across more than 120 countries, with a strong presence in developed markets (U.S., EU, Canada, Japan, Australia) and emerging regions. The company is known for advancing accessibility to life-changing biologic therapies, especially in diabetes, cancer, and autoimmune diseases.

Biosimilars are medicines that are highly similar to existing, approved biological drugs (called reference products), with no clinically meaningful differences in safety, purity, or effectiveness compared to those originals. They are produced from living cells and organisms, making them much more complex than traditional drugs. Biosimilars offer equivalent therapeutic benefits and are approved after rigorous regulatory tests to prove their similarity and safety, often at a lower cost than the reference biologic.

Global Reach and Impact

Biocon Biologics has commercialized 9 biosimilars worldwide, including several firsts like interchangeable insulin products and monoclonal antibodies that received U.S. FDA approval. Its international reach is supported by direct field forces in locations such as the UAE and Saudi Arabia, strategic acquisitions (notably the Viatris global biosimilars business), and regional partnerships that allow tailored market approaches.

Portfolio and Innovation

The biosimilars portfolio includes over 20 products spanning recombinant proteins, insulins, and monoclonal antibodies, covering major therapy areas. Notable market achievements include the World’s 1st Pichia pastoris technology-based recombinant human insulin (rh-Insulin) and several milestone regulatory approvals for biosimilars in the U.S., Europe, Japan, and Australia.

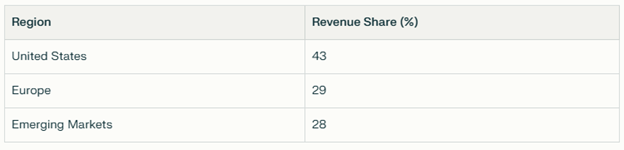

Geographic Revenue Split

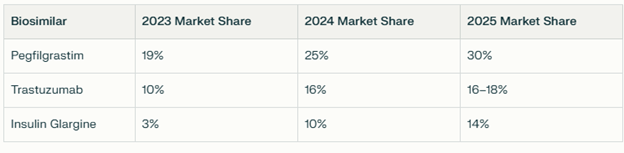

Top Biosimilars by Sales and Market Share

- Pegfilgrastim (Fulphila®): Leading biosimilar for neutropenia, with U.S. market share rising to 30% in the latest annual period.

- Trastuzumab (Ogivri®): Major oncology biosimilar, U.S. share doubling year-on-year to 26%, and strong showing in Europe at 15% market share.

- Insulin Glargine (Semglee®): Best-selling diabetes biosimilar, the world’s first interchangeable insulin glargine approved by the FDA, top market share for insulin among biosimilars globally.

- Bevacizumab (Abevmy®/Jobevne™): Oncology biosimilar with expanding market, European market share at 9%, recent U.S. launch (Jobevne™) expected to further boost presence.

The table below highlights increase in market share in the US market.

Impact of tariffs

Biosimilars exported by Biocon Biologics to the US do not currently attract US tariffs, as the American administration's recent tariff policies explicitly exempt pharmaceutical products—including biosimilars and generics—from both the 25% and 50% levies imposed on other Indian exports in 2025. This exemption exists because pharmaceuticals, including Biocon Biologics' biosimilars, are classified under the broader pharmaceutical category, which US authorities have shielded from trade penalties due to their importance for US healthcare affordability and supply.

Commercial Model and Partnerships

Biocon Biologics has transitioned from a B2B partner-based model to a direct commercial footprint in several markets, strengthening ties with patients, providers, and payors. The acquisition of Viatris’ biosimilars business further integrated Biocon’s reach and operating capabilities globally. Its legacy collaborations with Mylan/Viatris helped establish a long-standing presence and credibility in the biosimilars sector.

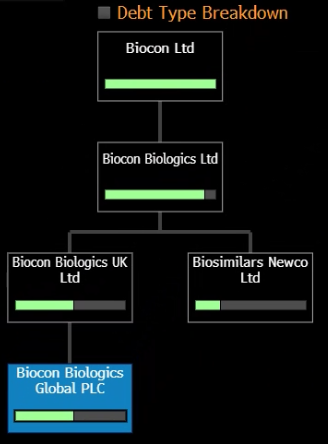

Corporate Structure

Biocon Biologics Global Plc is registered in the UK as part of its broader international expansion and access to capital markets.

1st Lien structure

The 6.67% 2029 bond issued by Biocon Biologics Global plc is guaranteed by Biocon Biologics Limited (BBL), which is the direct parent company. Biocon Limited, the Indian listed parent, is not itself a guarantor of the bond. The guarantee structure involves BBL as the “Parent Guarantor,” as well as certain key operating subsidiaries. Biocon Limited (India) owns BBL, but guarantees are furnished at the Biocon Biologics Limited level, not directly by Biocon Limited (India).

The guarantee from Biocon Biologics Limited is substantial and capped at 100% of the principal outstanding until April 30, 2025, then rises to 110% of the principal after that date. There is no direct full guarantee from Biocon Limited, the Indian parent, for these bonds

The security package for Biocon Biologics Global plc’s 6.67% 2029 Senior Secured Notes consists primarily of a first-priority pledge over the capital stock (shares) of several key operating subsidiaries within the Biocon Biologics group:

- All capital stock of the Issuer (Biocon Biologics Global plc) held by Biocon UK.

- All capital stock of BCIL (Biocon Biologics Canada Inc.) held by Biocon UK.

- All capital stock of BNCL (Biocon Biologics North Carolina LLC) held by Biocon Biologics Limited (parent guarantor) and Biocon UK.

This security package does not include fixed assets, receivables, or intellectual property directly; it is primarily an equity pledge structure. The pledged shares serve as collateral for the benefit of noteholders and provide direct recourse to ownership interests in the core operating subsidiaries.

Credit outlook

The outlook for the 6.67% Biocon Biologics Global Plc (2029) bond by rating agencies—including Fitch, S&P, and ICRA—is currently “Stable,” and the bond holds a long-term rating at the BB level by both Fitch and S&P.

Key Points from the Rating Agencies

- Fitch: Affirms a ‘BB’ rating (senior secured) on the USD 800 million 6.67% notes due 2029, with a Stable Outlook as of September 2025. Fitch notes Biocon’s growing scale, global biosimilar market position, robust product pipeline, and strong parent backing, but highlights high leverage and some margin pressure as constraints.

- S&P: Assigns a ‘BB’ rating with Stable Outlook, reflecting Biocon Biologics’ integral role as the primary earnings engine for the Biocon group. S&P expects solid group cash flow generation and long-term parental support, while observing risks from competitive biosimilar pricing and debt-funded growth.

Outlook Triggers and Risks

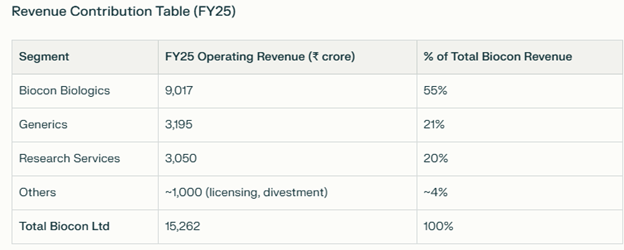

Ratings could be upgraded with faster-than-expected deleveraging and higher operating margins. Downside triggers include margin compression below 20%, persistent high leverage (net debt/EBITDA above 3.5x), or negative regulatory events. All agencies see Biocon Biologics as strategically important to the Biocon group and expect continued financial and operational support from the parent (contributed almost 55% of consolidated revenue as below).

%20(16).png)

.png)

.png)