"Whom the gods would destroy, they first make mad," warned Euripides. Today’s high yield market, with yields compressed to uneasy lows and default rates contained, reflects that same mania—where calm valuations disguise compounding risks beneath the surface.

The risks being- wall of maturity in the coming years, marginal increase in default rates (lower interest rates and assuming an economic slowdown and NOT a full-blown recession in the US), increase in distress ratios and increasing pace of credit downgrades. These come with an eventual outcome in form of widening spreads, with the quantum hinging on the performance of the US economy.

Investors will do well sticking to BB credits with low to negligible refinancing needs.

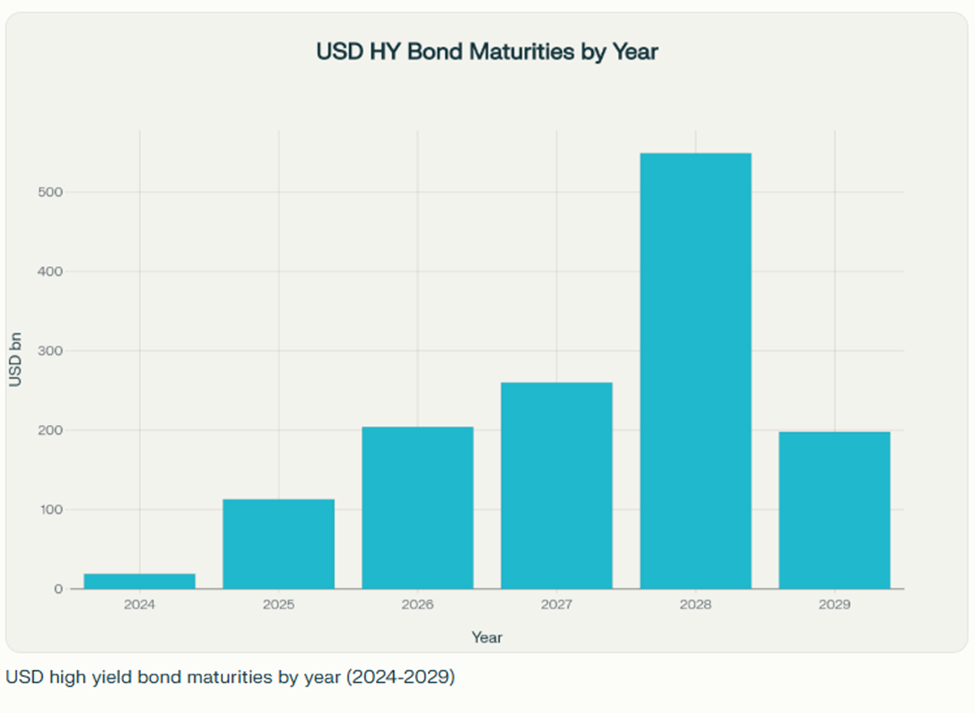

WALL OF MATURITY or WALL OF WORRY?

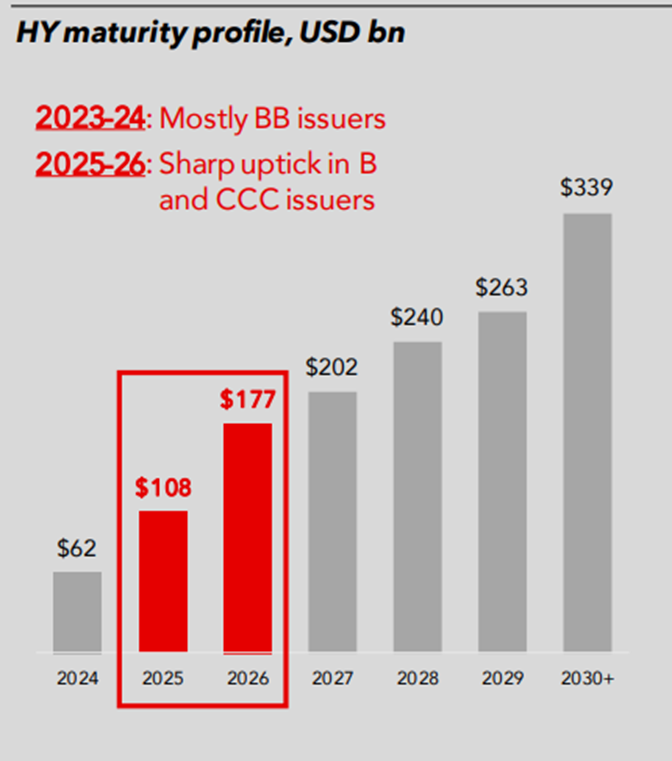

While the chart below depicts the maturities by year, a deeper dive into the segment showcases that the “maturity wall” is most severe from 2026 to 2028, especially for lower-rated issuers (B and CCC in the subsequent chart).

Since late 2022, proactive refinancing has helped reduce near-term maturities by about 26%, but market participants remain focused on refinancing risk as rates stay elevated and capital market access is tighter for weaker credits.

Companies with maturities in these peak years must secure refinancing well in advance, particularly those with strained credit profiles or floating-rate debt exposure.

Key takeaways

- Elevated refinancing requirements, especially in 2028 (almost 50% of the total USD HY debt outstanding), will be a key risk factor for US high yield bond investors.

- Vigilant credit selection is advised, as lower-quality credits face significantly greater refinancing challenges over the next five years.

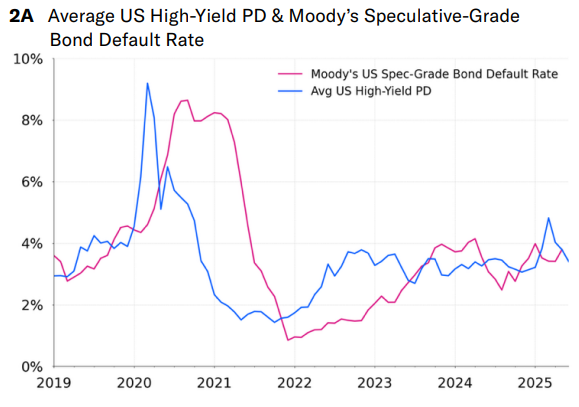

Default Rates

The volatile macro-credit environment calls for a cautious stance: anticipate challenges and setbacks but remain open to the possibility that things might turn out better than expected. Moody’s Analytics updated baseline economic forecast sketches out a tug-of-war between the inflationary pressures resulting from trade frictions, and the knock to economic growth that such frictions may cause. Despite better than expected 3% GDP growth in Q2, Moody’s Analytics’ baseline forecast is for GDP growth of 1.3% in 2025 and 1.5% in 2026.

A recession, as defined by the National Bureau of Economic Research, is not a prerequisite for higher default rates, but sufficiently weak economic growth often is. There is a growth “stall speed” below which the pace of credit events starts to notably pick up. When GDP growth falls below about 1.5% per annum, you start to see a higher pace of credit events historically.

High-yield bond issuers are projected to see a realized default rate of 3.2% for calendar year 2025, rising to above 4% by Q1 2026.

While Moody’s forecast points to a higher future default rate for high-yield companies in a year’s time, the forecast is still below the 4.5% historical average annual default rate since 1996.

Key takeaways

- 2025: Consensus expects USD high yield default rates to rise to around 4–5%, up from recent lows, with some one-off large defaults accounting for a sizable share.

- 2026: Default rates are likely to climb slightly higher (above 4%) as more refinancings approach and as riskier credits face growing pressure.

- 2027–2029: Provided there is no sharp economic downturn, rates are projected to normalize around the long-run historical average (4–4.5%); volatility may increase if macro conditions deteriorate.

- Credit rating agencies note that a surge to pandemic-type default levels is not base case unless major external shocks arise.

Overall, the near-term USD HY default outlook is for a modest increase, but sustained spikes above 5% are not broadly forecast without a deep recession or credit market dislocation.

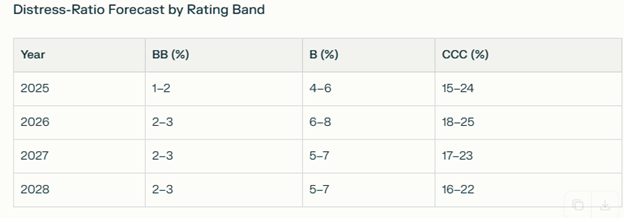

Distress Ratios

Forecasts for distress ratios (defined as spreads above 1000 bps) in the USD high yield market by rating band (BB/B/CCC) show material differences in risk profiles. Distress ratios are far higher for CCC-rated bonds, while BB remains relatively insulated with the key annual outlooks:

Key takeaways

- BB distress ratios are forecasted to hover in the low single digits, reflecting the relative resilience and higher quality of this rating band in high yield compared to others. BB is less vulnerable to economic or sector shocks and is more likely to refinance successfully than lower-rated peers.

- B distress ratios are notably higher, ranging from 4–8% across the period. This group faces more refinancing and sector risk, with stress linked to rising maturity walls and higher volatility.

- CCC distress ratios are materially elevated, with forecasts calling for 15–25% over the next three years. The CCC segment bears the brunt of distressed trading, cyclical sector stress, and liability management exercises. This band is most exposed to market shocks and pivot points in macro conditions.

The overall market distress ratio remains in the 6–8% range, but most of the distress is contained within the CCC bucket, which has seen increased negative sector momentum in telecom, healthcare, and capital goods.

Pace of Downgrades

The pace of downgrades in the USD high yield market accelerated in 2025, with ratings agencies projecting continued negative rating pressure and a rising number of issuers with negative outlooks going into 2026.

2025 Downgrade Count and Trends

- As of mid-2025, negative rating actions outpaced positive ones, with around 20% of high yield credits experiencing downgrades or negative rating migration, compared to 15% with upgrades.

- Major agencies such as Fitch revised the North American corporates outlook to "deteriorating" from "neutral," highlighting increased downgrade activity and a shrinking cushion under leverage tests for more than half of rated issuers.

- The percentage of HY issuers with a negative outlook reached approximately 17% by end-2024 and in H1 2025, compared to just 11% with positive outlooks, per Scope Ratings and AXA IM.

- The ratings migration trend is notably weaker in HY versus IG, with BB/B/CCC names in cyclical sectors and highly leveraged structures representing most of the negative outlook cohort

2025 Forecast for Downgrades & Negative Outlooks

- Sell-side consensus and agency forecasts indicate that downward pressure will likely persist into 2026, with downgrade rates of 18–21% forecast for speculative-grade credits.

- Fitch expects more than half of rated North American HY issuers to have less than 0.5x cushion under negative leverage tests by year-end, suggesting high vulnerability to further downgrades if macro stress intensifies.

- Ratings agencies caution that persistent inflation, high refinancing costs, and sector-specific headwinds (retail, chemicals, media, energy) will drive a renewed cycle of negative ratings migration and new fallen angels through 2026.

Key Takeaways

- In 2025, downgrade pace and negative outlook prevalence hit multi-year highs, with sector concentration in cyclical and highly levered names.

- Forecasts indicate further elevated downgrade activity through early 2026 unless macro conditions improve significantly, with negative outlooks remaining above historical averages.

These trends reflect a challenging landscape for USD high yield credits, characterized by heightened rating risk and sector-specific vulnerability to further downgrades

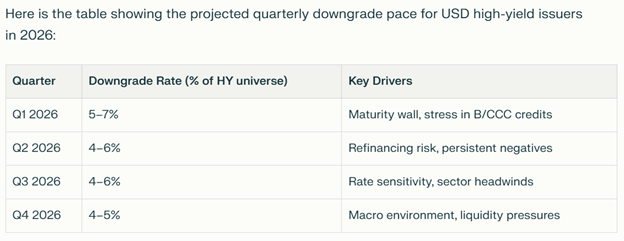

Downgrade Rate Forecast 2026

- Downgrade rates for speculative-grade issuers are expected to be between 18% and 21% for 2026, staying high as refinancing and rating migration risks remain prominent.

- Ratings agencies highlight elevated numbers of issuers with negative outlooks heading into 2026, especially in cyclical and highly leveraged sectors.

- More than 50% of North American high-yield issuers are likely to operate with less than a 0.5x cushion under leverage tests by end-2025, signalling high vulnerability to additional downgrades in 2026 as per Fitch Ratings.

To conclude, the USD High Yield bond market faces heightened risks over the coming years from persistent inflation, policy rate uncertainty, and the threat of recession or stagflation. Key risk drivers include rising corporate default rates (especially in sectors with weak fundamentals), refinancing pressure as maturities cluster in a higher-rate environment, potential for widening spread amid global shocks, and growing dispersion between issuers. Continued geopolitical tensions and elevated tariffs further challenge corporate earnings and credit quality, demanding vigilant credit selection and nimble risk management approaches.

%20(16).png)

.png)