The defining feature for 2026 global markets is not uncertainty, but transition. The investment regime of the past few years, shaped by aggressive rate hikes and liquidity withdrawal, is gradually giving way to a more nuanced environment: one where rates are expected to come down, but slowly, growth persists without broad-based job creation, and inflation settles into a narrow band rather than collapsing outright.

What is emerging is not a synchronised global cycle, but a set of regional divergences that demand far greater selectivity in how capital is deployed.

Against this backdrop, Lighthouse Canton’s core convictions have not shifted. They have strengthened.

“Our conviction has just gone up when it comes to long-term income-generating strategies,” Sanket Sinha said, reflecting on how portfolios are being positioned for the year ahead. While the pace of rate cuts is unlikely to be steep, given that economic growth across most markets has held up, the direction of travel is increasingly clear.

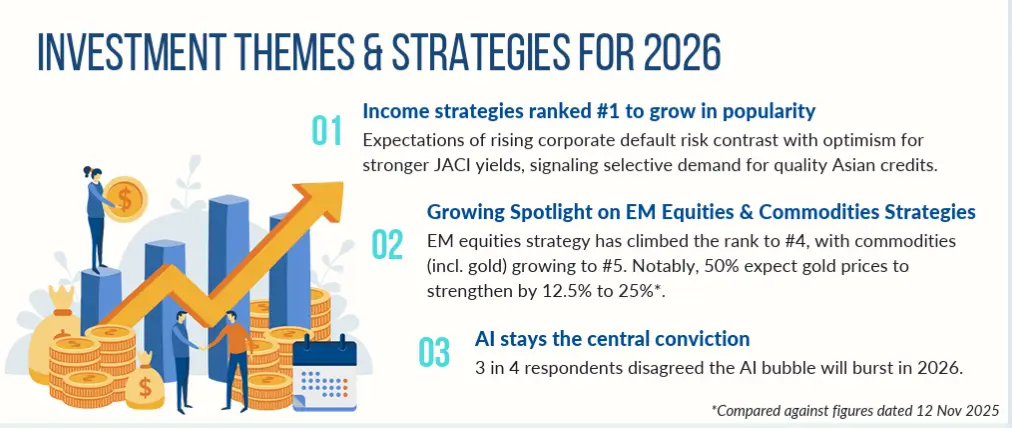

Sinha’s views are in line with the latest survey held by the Investment Management Association of Singapore where income strategies ranked #1 to grow in popularity in the year ahead.

Governments, facing the pressure of uneven employment outcomes, will be compelled to stimulate capacity expansion and investment. Over time, that necessitates lower rates.

At the same time, inflation is unlikely to disappear. Sinha expects a sustained range of 2–3%, creating the possibility of a negative real-rate environment as nominal rates ease. In such conditions, strategies generating high single-digit to low-teen income stand out, not as opportunistic trades, but as structurally attractive allocations.

In such conditions, strategies generating high single-digit to low-teen income stand out, not as tactical opportunities, but as structurally attractive allocations designed to preserve real purchasing power.

“This is not about changing strategy,” he noted. “It’s about higher conviction.”

Why Income Matters More in 2026

The appeal of income-generating strategies is reinforced by a simple asymmetry. As rates fall gradually, capital values across traditional fixed income may see limited upside, while reinvestment risk rises. In contrast, high-yielding private market strategies continue to deliver contractual income, which becomes more valuable as real yields compress elsewhere.

This distinction is particularly important in a late-cycle environment, where volatility in public markets can obscure total return outcomes, while private income streams remain contractually defined.

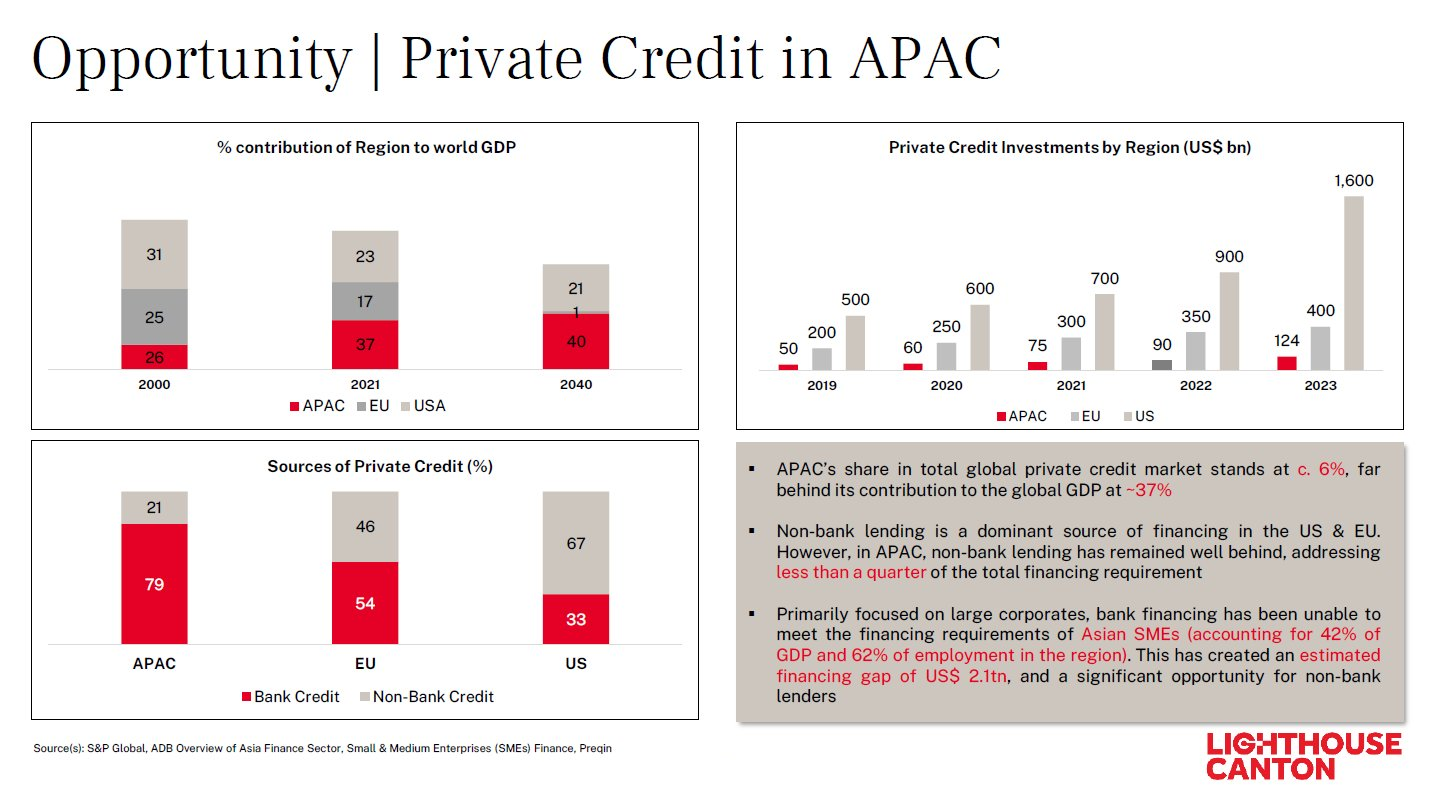

This dynamic is especially relevant in Asia, where private credit spreads remain materially wider than in developed markets. Sinha highlighted that Asian private credit continues to offer 200–300 basis points of additional spread versus developed-market equivalents. While some compression has already occurred, driven by sustained capital inflows, he does not expect full convergence.

“Country risk premium will always exist,” he said. “If it was 300 basis points ten years ago, maybe it becomes 200, it doesn’t disappear.”

Importantly, supply-demand dynamics matter.

Across South and Southeast Asia, select markets are capable of absorbing meaningful institutional capital without the degree of crowding now evident in more mature private credit ecosystems.

While capital flows into parts of Asia can be volatile year to year, the structural trend remains intact. Domestic capital formation has also increased significantly, further deepening the market.

Lighthouse Canton is increasingly focused on identifying opportunities in less crowded regional markets where balance sheets have strengthened and credit penetration remains low.

That said, Sinha is clear that headline spreads do not tell the full story. For international investors, net yields are shaped by local factors, including India’s withholding tax regime. Unlike developed markets where gross and net yields often converge, emerging market returns must be assessed post-tax and post-hedging. Even so, the structural premium remains compelling.

Structural Safety as a Differentiator

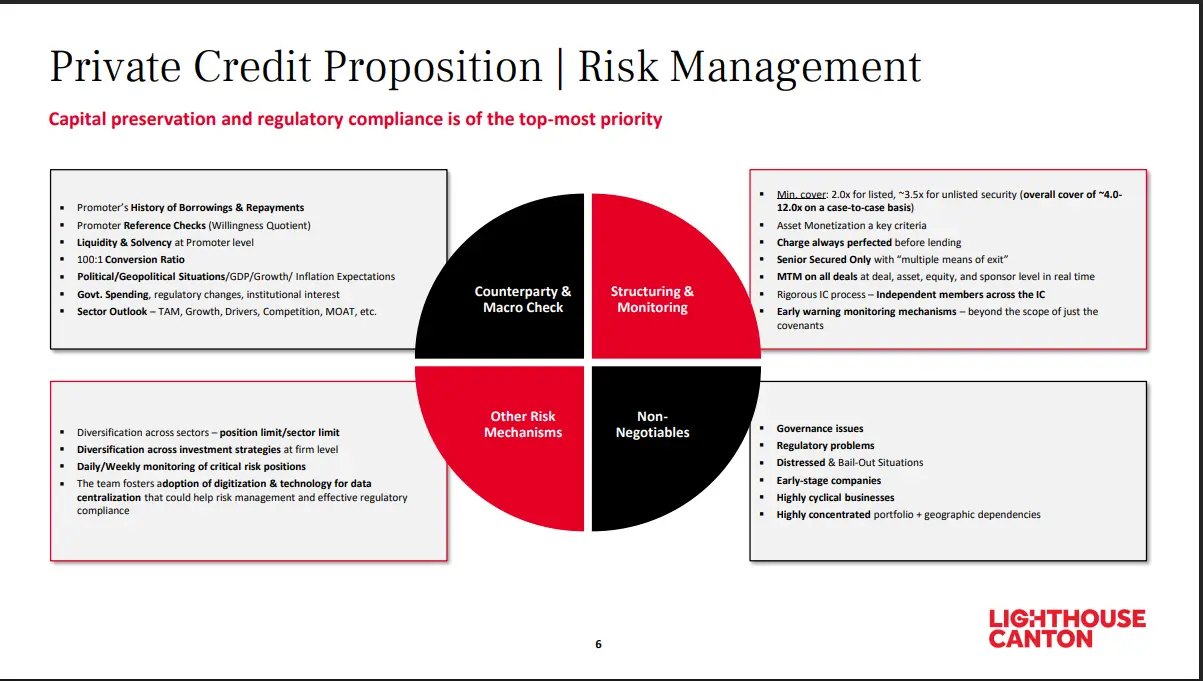

Crucially, the hunt for yield in 2026 cannot come at the expense of structure.

While Western private credit markets increasingly drift toward ‘covenant-lite’ deals with leverage ratios stretching to 6–7x, Sinha highlighted Lighthouse Canton’s approach in Asia remains rooted in structural conservatism.

“We differentiate our portfolios by maintaining bank-like rigour, enforcing strict maintenance covenants, keeping loan-to-value (LTV) ratios low, and prioritising asset-backed security over pure cash-flow lending,” he noted.

This ‘governance premium’ allows investors to access high-growth emerging market yields while operating within a risk architecture that is paradoxically safer and less levered than the crowded middle markets of the developed world.

Diversification Beyond the AI Trade

Another defining feature of global markets today is concentration.

Across the US, China, and parts of Asia, public markets are increasingly driven by a single theme: AI.

In the US, AI-led mega-cap stocks have underpinned index performance. In China, a new wave of AI-focused companies has begun listing in Hong Kong.

India, however, presents a different profile.

“India is not just an AI play,” Sanket said. Besides offering rich opportunities in the field of AI, the country also has many opportunities in its traditional economy, which is consumption-led, infrastructure-led, and capacity-expansion-led.

In this context, India functions less as a thematic bet and more as a portfolio stabiliser, offering diversification at a time when global equity indices are increasingly exposed to a single narrative.

Following a period of strong performance, Indian public markets have undergone a time correction, delivering mid-single-digit returns over the past year while valuations normalised. This has enhanced India’s role as a diversifier within global portfolios, particularly if the AI super-trend pauses or corrects after its sharp rally.

More broadly, the investment opportunity in Asia is shifting away from AI model builders only toward companies applying technology pragmatically to improve productivity, logistics, healthcare delivery, and industrial efficiency. This is where Lighthouse Canton is focusing as well.

Broadening the Regional Lens

While India remains central, Lighthouse Canton’s asset management outlook for 2026 is not India-only.

The GCC is emerging as a key focus area. Historically an outbound capital market driven by oil-linked wealth creation, the region is undergoing a structural shift.

The UAE and Saudi Arabia are actively diversifying toward technology, infrastructure, real estate, and non-oil sectors. At the same time, inbound institutional capital from North American pensions and global private equity is increasing.

This creates a dual opportunity: participating in the region’s domestic transformation while positioning capital alongside global allocators entering the market.

China, too, is re-entering the frame, but selectively. After several years of price and time correction, Chinese technology has begun to show signs of renewal, particularly in AI. While first-generation AI companies are already public, Sinha highlighted growing interest in second- and third-generation players—companies applying AI within traditional sectors such as logistics, healthcare, robotics, and life sciences.

“These are not model builders,” he noted. “These are businesses applying AI to real-world problems.” Lighthouse Canton is looking to generate opportunities across India, the GCC, and North Asia for its investor base in 2026 and beyond, Sinha confirmed.

Specialisation Over Geographies

A key philosophical difference for Lighthouse Canton lies in how capital is structured and deployed.

Rather than running mega-sized regional funds, the firm prioritises specialised, market-specific strategies. Sinha emphasised that accountability increases when managers focus on discrete geographies rather than blended regional exposures.

“China is different from India. GCC is different from Southeast Asia,” he said. “Specialisation matters.”

This approach underpins the asset manager’s preference for India-focused, GCC-focused, or market-specific vehicles rather than broad Asia funds, where performance dispersion can be masked.

Setting the Context for 2026

Taken together, Sanket’s macro overlay frames 2026 as a year defined by:

- A gradual shift toward lower rates, not a sharp pivot

- Persistent inflation creating negative real-rate conditions

- Rising appeal of long-term income strategies

- Regional divergence, not convergence

- The importance of specialisation, structure, and net returns

.png)

%20(16).png)

.png)