"The world is full of magic things, patiently waiting for our senses to grow sharper." — W. B. Yeats aptly encapsulates the spirit driving hyperscaler capex today.

Hyperscaler capex is reshaping credit markets, with top firms demonstrating resilience through solid balance sheets and strong market positions. However, the supercharged AI-driven investment cycle is testing the limits of traditional credit models, elevating risk awareness around leverage expansion, returns on invested capital, and the durability of funding market support.

Their aggressive capex spend is a leap of faith in next generation technological potential: deep learning, artificial intelligence, quantum computing, and global connectivity, which hold transformative promise but require enormous financial commitment to materialize. Just as Yeats suggests that hidden wonders await recognition, hyperscalers are investing in platforms and compute power in anticipation of exceptional breakthroughs, while monetization is still evolutionary.

Lighthouse Canton View on Hyperscaler credits

- Oracle: We do not prefer Oracle credits largely owing to a single customer concentration (Open AI is at least 2/3 of Oracle’s RPO- Remaining Performance Obligation). Its net leverage is at 3.86x prior to the recent debt issue of US$ 18Bn in September with more issuance expected in the coming 3 years. It runs a high risk of being downgraded.

- Meta: We do not prefer META credits largely owing to its outsized US$ 30bn bond issuance on the heels of the recent US$ 27bn off -balance sheet META JV bond deal. Total expenses are expected to grow significantly faster as will be the “notably larger” capex in 2026 as announced in the earnings call making it susceptible to meaningful spreads widening.

- Alphabet: This remains our top pick amongst Hyperscaler credits and that is largely owing to the massive -ve net debt (Cash > Total Debt) with its recurring annual FCF far exceeding total debt outstanding in any of those years. High Quality assets (Search, YouTube, Android and Gmail) are additional positives.

- Amazon: We continue to like the lease adjusted debt reduction that partially offsets its debt fueled capex. Furthermore, we believe that AMZN will be able to transform itself given the breadth of its cloud business, custom silicon (Trainium and Inferentia) and its Bedrock platform. Regulatory scrutiny and its proclivity to large M&A (US$ 14bn acquisition of Whole foods) in the wake of tougher regulations tone our view on its credit to NEUTRAL.

- Microsoft: It is seeing surging capex and a healthy return on shareholder capital (almost 100% of FCF this year) however the operating trends have been exceptional. Revenue growth (+39% in Azure and double digit overall) coupled with robust balance sheet (net leverage of 0.1x as of Sept 2025.). Microsoft has not issued any bonds (except for exchange offers) since 2017 and remains only one of the two AAA rated corporates out of the US. We prefer the back end/long end of MSFT credits given their moderate spreads over the front/belly of the curve (extreme tight spreads).

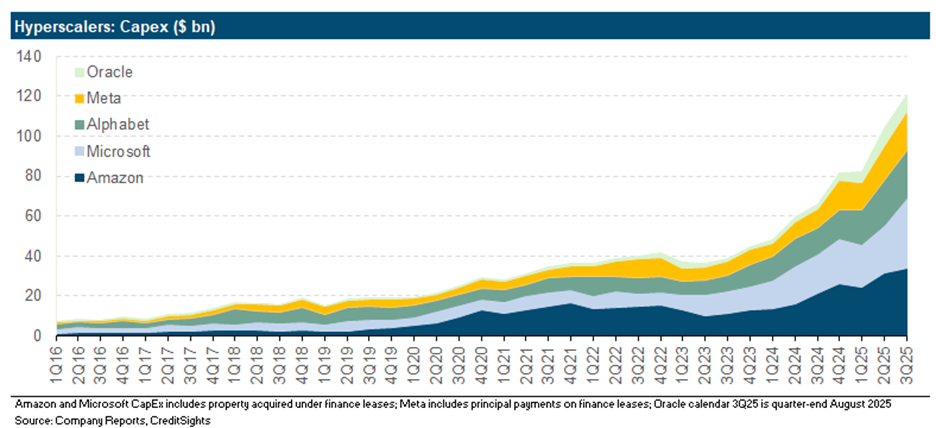

Hyperscaler capital expenditure (capex) surges to unprecedented levels in 2025-2026, with profound implications for credit quality and risk profiles across the sector. Leading firms (Amazon, Microsoft, Alphabet, Meta, Oracle) are projected to increase aggregate capex from around $256 billion in 2024 to $443 billion in 2025 and potentially surpass $600 billion in 2026, mostly directed toward AI infrastructure buildouts. This uptrend marks a structural commitment but also represents a major transformation in capital intensity and funding strategy.

Key Credit Implications

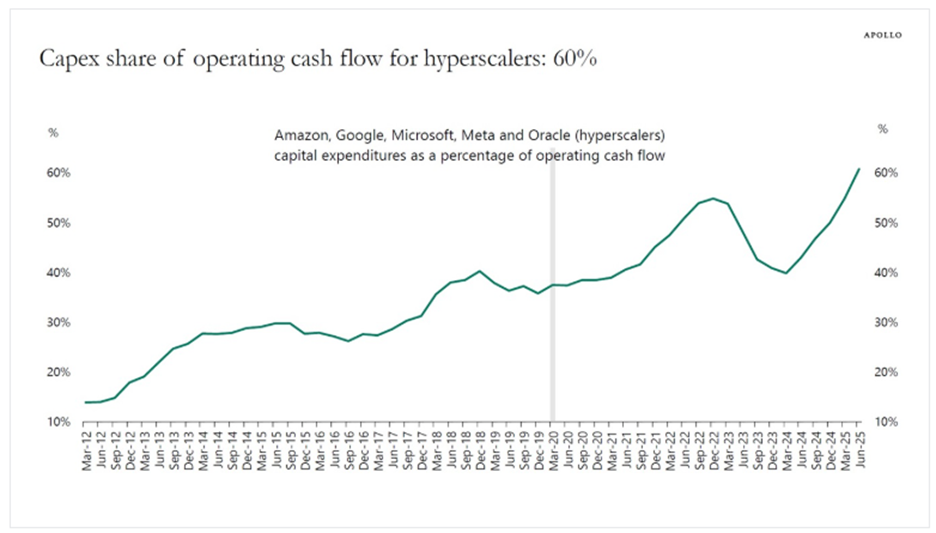

- Hyperscalers are spending record-high shares of their operating cash flow (over 60% for some) on capex, driving a shift from historically asset-light business models to capex-heavy structures.

- Despite the dramatic ramp-up, the sector maintains strong investment-grade credit ratings (AA- or higher for most, except Oracle). Solid operating fundamentals, robust cash flow generation (over $700bn annually), and sizable liquidity help buffer the impact of rising leverage from debt issuance.

- The need for external funding is growing while large hyperscalers can fund much of their capex through free cash flow, they increasingly tap public and private debt markets due to the relatively lower cost of debt compared to using retained earnings or equity.

- Issuance volumes in investment grade credit are expected to remain strong, with the AI infrastructure capex cycle driving supply, yet the market is becoming more selective and cautious in pricing, especially for non-pristine balance sheets and weaker credits.

Sources: Bloomberg, Apollo Chief Economist.

Risk Factors and Investor Considerations

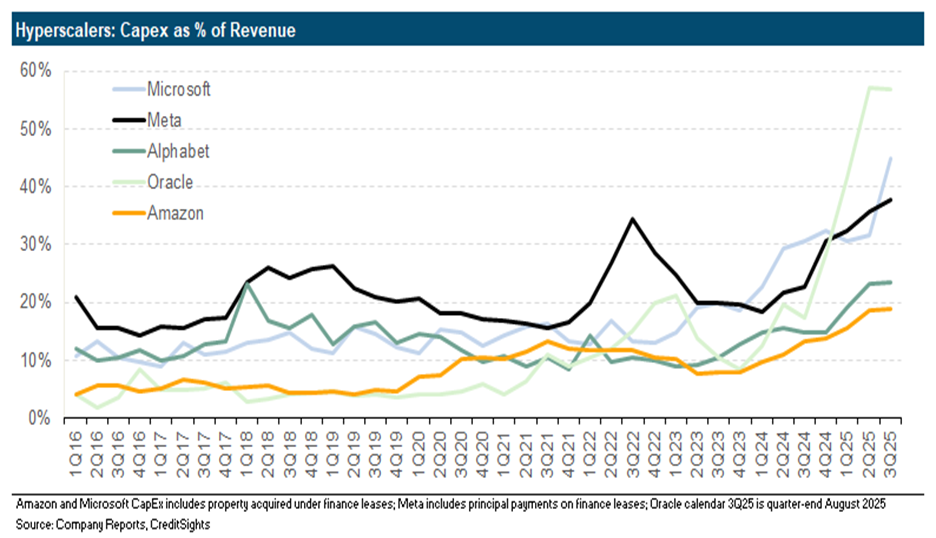

The elevated capex-to-revenue ratio (recently above 22% versus a historical mean of 12.5%) signals potential margin compression and exposes firms to elevated risk in an environment of decelerating cloud revenue growth and global trade uncertainty.

For private credit, rapid scaling can pressure investment teams to compromise underwriting standards, resulting in lower selectivity and potential erosion of returns—especially if large direct lending deals compete with broadly syndicated markets.

Credit risk is also tied to how efficiently capex translates into revenue growth and underlying technological differentiation (e.g., LLM/AI performance gains versus incremental cost escalation).

Investors should closely monitor both the pace and efficiency of capital deployment, potential overlap in loan portfolios, and early signs of stress, particularly in debt-heavy or aggressively scaling entities.

%20(16).png)

.png)

.png)