Capital deployment in the Middle East is entering a structurally different phase, with asset managers and institutional investors increasingly treating the region as a destination for long-term allocations rather than merely a source of capital.

“This region has always been heavy on private markets, what’s changing is that access to these strategies is expanding meaningfully,” said Prashant Tandon, Managing Director and Chief Executive Officer, UAE at Lighthouse Canton. “Opportunities that were once reserved for sovereign wealth funds and very large family offices are now accessible to a broader ultra-high-net-worth investor base.”

That shift is already reflected in how global managers are positioning their balance sheets.

Lighthouse Canton has begun allocating private credit capital directly into the Middle East, signalling growing confidence in the region’s regulatory and legal frameworks. “Rather than just raising money from the region, we have started allocating to the region,” Tandon said, describing it as a significant inflection point.

The move has been underpinned by regulatory evolution across financial hubs such as the DIFC and ADGM.

“You can have contracts under common law frameworks, which gives managers confidence to deploy capital here,” Tandon noted, pointing to improved enforceability and investor protection.

Global asset managers are responding to the same signals.

Firms including BlackRock, Blackstone and Goldman Sachs have publicly identified the Middle East, and the UAE in particular, as a priority market for capital deployment, reflecting broader efforts to diversify geographically as Western markets become more saturated.

At the same time, the mechanics of private market access are changing. “This is not about retailisation,” Tandon said. “It’s about reducing minimum ticket sizes so that strategies requiring $20–25 million cheques are now investable with a few million dollars.”

That adjustment is reshaping capital flows on both sides of the market.

“Larger investors are increasingly willing to support smaller ecosystems, while families are gaining access to institutional-quality opportunities,” he added. “Democratization is happening both ways.”

PRIVATE CREDIT GAINS GROUND

Private credit is emerging as one of the most compelling expressions of the Middle East’s maturing private markets, supported by conservative structuring and yields that remain attractive relative to developed markets.

According to consulting firm Deloitte’s 2024 report, globally banks allocate around 22% of their loans to SME funding. In contrast, banks in the Middle East and North Africa (MENA) region allocate less than 10% to SMEs, with GCC banks allocating less than 2%.Consequently, access to capital for ambitious entrepreneurs and growing companies remains a largely unresolved challenge in the region, creating a strong case for the growth of private markets. This is where private market participants are stepping in.

“If you look at the investment universe for a family office in the UAE or institutional investment universe, about 40% of an investment portfolio is invested in private markets, as against the global average of 25%,” said Tandon. Within that allocation, real estate continues to dominate, but private credit is increasingly drawing attention as families diversify beyond property-led exposure.

The UBS family office report of 2024 supports this trend - with the private bank surveyed family offices having 50% portfolio in private markets and 50% in public..

The appeal lies less in complexity and more in discipline.

“The way covenants are structured in the East are far more conservative and robust than the way they are structured in the US,” Tandon explained, noting that downside protection and governance remain central to underwriting decisions in the region.

That conservatism has translated into a differentiated risk-return profile.

“The yields in the region are higher than they are in the US,” he added, pointing to feedback from institutional investors active in Middle Eastern private credit. “They see higher yield for a relatively safer returns.”

Tandon said the structural differences are enduring rather than cyclical. “Loans here are made in a much more secure and conservative manner than in the West,” he said, reinforcing the view that private credit in the region is benefiting from both pricing and prudence.

Public data supports that assessment.

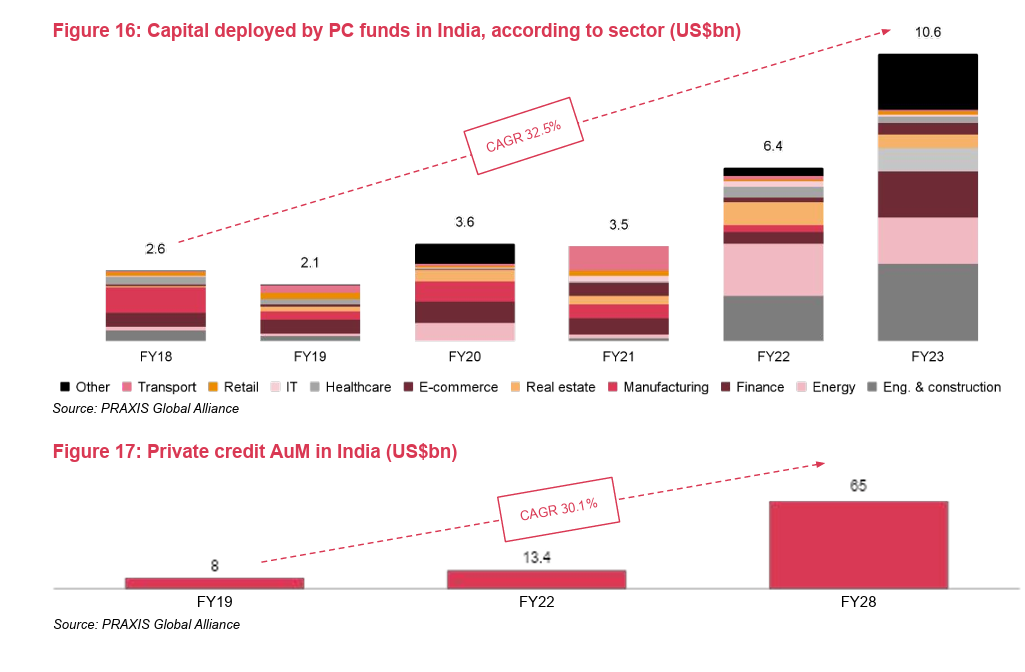

According to a January 2025 research by consulting firm EY, in FY19, the Indian private credit market was valued at US$8 billion, and by FY22, grew to US$13.4 billion, marking a CAGR of c.19%. Projections suggest this market could reach between US$60 billion and US$70 billion by FY28, with an expected CAGR of c.30%.

The GCC and Egypt are becoming increasingly attractive to investors due to their tightening credit regulations and enhanced bankruptcy and insolvency laws. If India’s growth story can be replicated, the market could grow from an estimated US$5 billion in FY24 to US$14 billion in FY30 (low case scenario).

WEALTH MIGRATION ACCELERATES INSTITUTIONALISATION

Capital flows into the Middle East are being reinforced by the physical relocation of wealth, a dynamic that is reshaping the region’s investment ecosystem and accelerating institutional maturity.

“Not only are global billionaires moving to the UAE, but they are also setting up structures within the country,” said Tandon. “And not just to raise capital, but to deploy.”

The scale of this shift is well documented. The Henley & Partners Global Wealth Migration Report consistently ranks the UAE as the world’s leading destination for millionaire migration, driven by long-term residency programmes, regulatory reforms and geopolitical positioning.

As wealth settles, investment behaviour is evolving alongside it. “The ecosystem is becoming more institutional, more process-driven and more robust,” Tandon said, describing a move away from transactional deal-making toward long-term portfolio construction.

Global firms are adapting to that shift. Some of the world’s biggest asset managers have moved senior managers to the region and are building meaningful bases here,” he said. “They’re not here just to raise capital, but to deploy.”

That institutional deepening is raising expectations among ultra-high-net-worth and institutional clients. “

As more institutional clients and younger generations move to the region, expectations around advisory, infrastructure and execution are rising,” Tandon noted. Demand is increasing for integrated networks, cross-border structuring capabilities and global-quality governance standards.

Talent migration is becoming more visible as a result, but gaps remain. “There is a shortage of specialised skills,” Tandon said, pointing in particular to demand for Mandarin-speaking investment professionals as Chinese wealth migrates into the region. “That creates both opportunity and constraint for firms operating here.”

The impact extends beyond financial assets. “The UAE is the number one destination for global millionaire migration,” Tandon said, adding that capital inflows naturally drive demand for luxury homes, lifestyle infrastructure and related real assets — trends reflected in the steady pipeline of high-profile branded developments across the country.

TECHNOLOGY ADOPTION SHIFTS

Technology is increasingly shaping how businesses and investors operate in the region, though the emphasis remains pragmatic rather than speculative.

“Every business is now becoming tech-enabled,” Tandon said. “AI is becoming second nature, and businesses that don’t adapt risk being left behind.”

Investment activity, however, is concentrated less on early-stage innovation and more on operational enablement. “A lot of investment is happening in infrastructure and systems that support existing businesses,” he said, rather than in locally driven innovation ecosystems.

That approach reflects the region’s current stage of development, where technology is viewed as a productivity and scalability lever rather than a standalone investment theme.

.png)

%20(16).png)

.png)