Private credit in Asia is breaking out of its traditional mold as managers look beyond plain-vanilla direct lending to a broader spectrum of structured opportunities. Acquisition financing, real estate credit, trade finance, growth debt and recapitalisations are becoming central pillars of the market, offering better risk-adjusted returns than conventional deals.

“The universe in Asia goes well beyond direct lending,” said Sanket Sinha, MD & CEO, Global Asset Management at Lighthouse Canton. “That is where a lot of innovative structures are coming into play.”

Sinha was speaking on the panel “Beyond Direct Lending – Unlocking the full potential of senior secured credit” at SuperReturn Asia 2025, held in Singapore in September. The event, which draws more than 2,500 private market professionals annually, is the region’s largest private capital gathering. As a sponsor at this year’s event, Lighthouse Canton shaped the debate on credit in Asia at the events Private Credit Summit.

In developed markets, direct lending is typically defined as senior loans to mid-market corporates outside syndicated bank or bond markets. In Asia, managers prefer the term performing credit—secured loans to corporates with operating cash flows—but even this description falls short.

Sinha pointed to areas where banks are constrained and private funds step in.

"In the context of acquisition financing, regulations in some jurisdictions restrict banks from providing onshore funding for such transactions," he stated. This has created recurring demand for such financing in those onshore markets, where deal activity is rising but domestic lenders cannot participate.

Real estate is another fertile area. “Asset-backed financing in the real estate sector is again a big thing,” he said. “There are a lot of end uses that banks are not able to fund.” Private lenders are increasingly underwriting land purchases and last-mile financing, helping developers’ complete projects sidelined by tighter bank credit.

Trade finance, too, offers opportunities. “Banks are typically able to do traditional products, while there are certain situations where alternate lenders play a role in filling the gap” Sinha said. “As an example, there are certain transactions like non-assigned receivable financing for SMEs, where alternate lenders including private credit funds are active.” .”

The Asian Development Bank estimates the region’s trade finance gap (difference between the demand from businesses for financing of imports and exports vs the availability of such financing) exceeds USD500 billion annually, a shortfall that alternative lenders are targeting with bespoke receivables and supply-chain solutions.

Beyond these, Sinha highlighted growth debt and recapitalisation structures—areas where private funds are offering corporates alternatives to equity dilution or bank refinancing. Cross-border lending, particularly in Southeast Asia and the GCC, is also on the rise as corporates diversify their funding sources.

To put this rise into perspective, Asia Pacific-based private debt assets under management (AUM) has grown at an average rate of 29% over the past five years compared to the global average of 17%, according to research conducted by Preqin.

According to a 2024 OECD report, for private credit transactions where data is available, a large portion of the proceeds are used to finance buyouts and public-to-private transactions. This is true both globally and in Asia. However, there are significant differences between Asian jurisdictions even when it comes to the use of proceeds of sponsored deals. Japan is a notable example, where over half of total investment refers to growth capital deals, i.e. funding to expand real operations. This contrasts with other large markets where financial operations are more common; over 90% of Chinese private credit investment is used to take listed companies private, and in Korea buyout funding makes up 59% of total investment

NIMBLENESS IN A LATE-CYCLE MARKET

While opportunities are broadening, spreads have been under pressure. “Direct lending or performing credit spreads have come in considerably over the last two or three years,” Sinha said.

The narrowing reflects heavier fundraising globally and more capital chasing deals in Asia. In such conditions, adaptability becomes a differentiator. “It is important to be nimble and keep looking for opportunities where you can generate alpha,” Sinha added.

Nimbleness is not only about portfolio construction but also about fundraising.

“You can’t raise capital for very narrow strategies any longer, at least not in these markets,” Sinha said. Investors now expect managers to move across performing credit, structured lending, growth debt and opportunistic plays rather than be tied to a single vertical.

Industry observers agree that late-cycle caution is influencing allocator behavior. With global M&A subdued and base rates still elevated, managers able to pivot across strategies are more likely to sustain returns.

ASIA VERSUS DEVELOPED MARKETS

Sinha stressed that Asia’s relative advantage lies in both spreads and borrower quality. “Spreads are maybe 200–300 basis points higher in Asia,” he said.

But spreads alone do not explain the appeal. “In the US and Europe, there is so much supply of capital that GPs have gone down the credit spectrum,” Sinha observed. “The structures are much looser, and the covenants lighter.”

In Asia, by contrast, private lenders are still financing established corporates with conservative leverage. “You are still lending to top borrowers,” Sinha said. “Often with lower levels of leverage.”

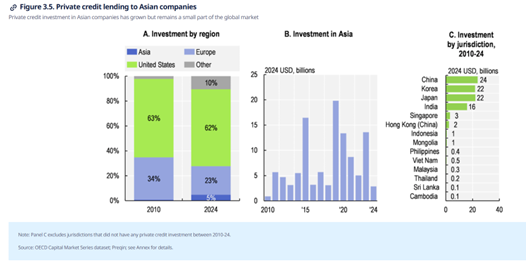

An OECD report supports this trend. Asia still remains a small part of the global private credit market, both in terms of funds’ assets under management and private credit lending to Asian firms. Four key markets have driven this trend, namely China, Korea, Japan and India, which together account for 91% of the region’s private credit investment from 2010 to 2024.

For allocators, the implication is that broad geographic comparisons miss the real point. “LPs need to look beyond country and geography risk,” Sinha concluded. “They should focus on micro borrower-level risk when making allocation decisions.”

.png)

%20(16).png)

.png)