Table of Contents

Executive Summary

The prevailing narrative across much of Wall Street is that the recent correction in enterprise software stocks is overdone. We take a different view. We believe the selloff is not a temporary dislocation but an early-stage repricing of a structural shift in how software businesses generate revenue and sustain margins.

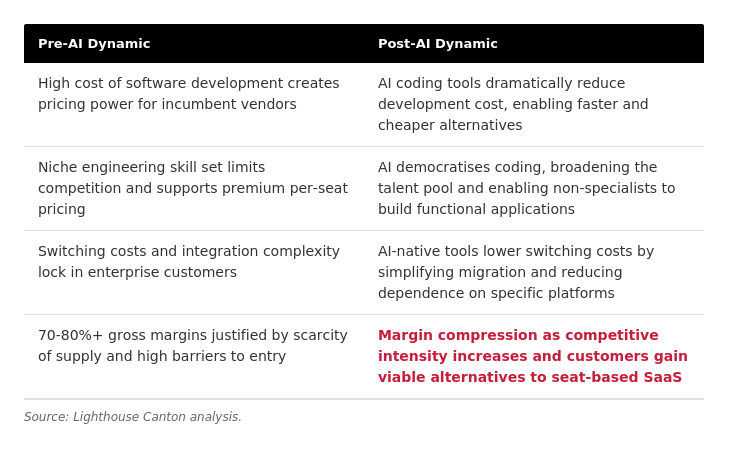

The core thesis is straightforward: AI is not eliminating the need for software. If anything, the world will need more software than ever. What AI is fundamentally challenging is the per-seat, per-month subscription model that has underpinned SaaS economics for over a decade. That model worked because developing software was inherently expensive and required specialised skills that few possessed. Both of those conditions are now eroding rapidly. Frontier coding tools from model developers have dramatically lowered the cost of building software and broadened the pool of people capable of doing so. This disrupts the pricing power that justified 70-80%+ gross margins and the premium valuation multiples that accompanied them.

The financial implication is a sector that transitions from 80% gross margin businesses to something materially lower, with a direct impact on return profiles and, consequently, the valuation multiples these businesses deserve. This, in our view, is exactly what is playing out: valuation multiples are compressing even as earnings per share for many of these businesses continues to grow. The market is not punishing these companies for poor execution. It is repricing the future.

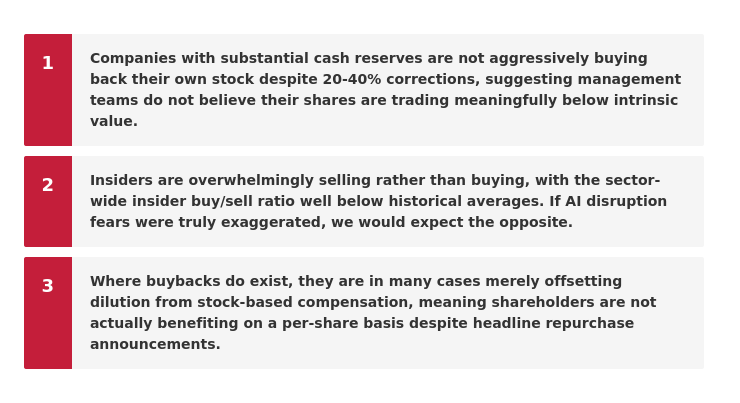

If this thesis is wrong, and the selloff is genuinely overdone, we would expect to see clear signals of conviction from those who know these businesses best: the management teams and insiders themselves. We do not see those signals. Instead, we observe three patterns that corroborate our structural concern:

Taken together, these observations suggest the selloff is less about market irrationality and more about a rational repricing of a business model whose competitive moat is narrowing. The remainder of this note explores each dimension in detail.

The Structural Thesis: It Is Not About Needing Less Software

A common mischaracterisation of the bear case on enterprise software is that AI will make software obsolete. This is a straw man. Enterprises will almost certainly deploy more software in the years ahead, not less. The digitisation of workflows, the proliferation of data, and the integration of AI itself into business processes all point to expanding software demand at the application layer.

What is being challenged is not the demand for software but the pricing model under which it is sold. For over a decade, enterprise SaaS companies have operated under a per-seat, per-month subscription model that has generated gross margins in the 70-80%+ range. This model was sustainable because of two structural advantages:

First, the cost of developing high-quality software was extremely high. Building enterprise-grade applications required large teams of highly skilled engineers, years of development, and significant ongoing maintenance investment. This created natural barriers to entry and justified premium pricing.

Second, software development was a niche skill. The pool of people capable of writing production-quality code was limited, which kept labour costs elevated and further reinforced the scarcity-driven pricing that SaaS vendors could command.

Both of these conditions are now under direct assault from AI-powered coding tools. Frontier model developers, including Anthropic, OpenAI, Google, and others, have released code generation and assistance tools that have fundamentally altered the economics of software creation:

The financial implication of this transition is significant. A business that moves from 80% gross margins to, say, 60-65% gross margins experiences a fundamental change in its return profile. Operating leverage diminishes, free cash flow conversion weakens, and the valuation multiple the market is willing to assign contracts accordingly. This is not a hypothetical concern. It is precisely what we are observing: EPS continues to grow for many of these companies, yet multiples are compressing. The market is not ignoring their current profitability; it is discounting their future margin trajectory.

Corroborating Signal #1: The Absence of Aggressive Buybacks

If the structural thesis above is wrong, and these businesses truly are being mispriced by the market, we would expect their management teams to act on that conviction. The most direct expression of management confidence in intrinsic value is an accelerated share repurchase programme. When the gap between price and value is wide, buying back stock is the highest-returning use of capital. This is foundational corporate finance.

Many of the enterprise software companies that have corrected 20-40% from their highs are sitting on substantial cash positions and carry investment-grade balance sheets. They have the resources to buy back stock aggressively. Yet, by and large, we are not seeing accelerated buyback programmes from the very companies whose advocates argue are undervalued. Most continue with routine, modest repurchase activity that existed before the correction. Some have no buyback programmes at all.

This is a revealed preference signal and it is consistent with our structural thesis. If management teams believed their gross margin profiles and competitive positions were secure, buying back stock at a 30% discount would be an obvious decision. The fact that they are not doing so suggests they may share the market's reassessment of long-term margin sustainability, even if they cannot articulate it publicly without damaging employee morale or customer confidence.

Corroborating Signal #2: Insiders Are Selling, Not Buying

If the corporate-level signal from buyback behaviour is concerning, the individual-level signal from insider transactions is equally so. Across the technology sector in 2025 and into early 2026, the insider buy/sell ratio has been notably depressed.

Technology executives at major firms accounted for record insider stock sales in 2025, even as share prices declined. If a CEO or CFO truly believed that AI disruption fears were overblown and their stock was a compelling buy at current levels, we would expect to see open-market purchases reflected in their Form 4 filings. Instead, the filings overwhelmingly show consistent selling as options vest and RSUs are exercised.

We acknowledge that insider selling alone is not necessarily bearish. Executives sell for many reasons, including diversification, tax planning, and liquidity needs. However, the near-total absence of meaningful insider buying across the sector during a period where stocks have corrected 20-40% is difficult to reconcile with the thesis that these businesses are fundamentally undervalued. The people closest to these businesses are choosing to reduce their exposure, not increase it.

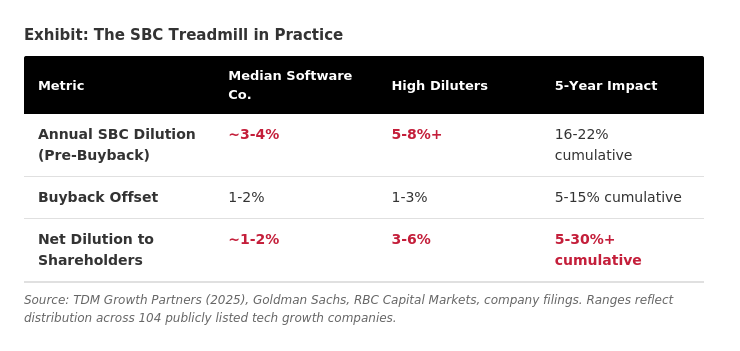

Corroborating Signal #3: The Stock-Based Compensation Treadmill

Even among those software companies that do conduct buybacks, a critical examination of shares outstanding over time reveals a troubling pattern: in many cases, the repurchased shares are merely offsetting dilution from stock-based compensation (SBC), and shareholders are making no net progress.

The data on this is unambiguous. TDM Growth Partners' 2025 benchmarking study of 104 publicly listed growth technology companies found that pre-buyback SBC dilution ranged from 0.2% to 8.6% annually, with the median software company diluting shareholders at approximately 3% per year. Goldman Sachs data from recent years showed median annual dilution for software companies reaching nearly 4%, up from approximately 2% in 2020.

RBC Capital Markets highlighted that a company diluting at 5.5% annually would see its share count grow by over 30% in five years. In such a scenario, net income could grow 30% over that period, but earnings per share would remain flat. The shareholder experience would be one of running in place.

Furthermore, the standard financial reporting in the software sector exacerbates this issue. The vast majority of these companies add back SBC as a non-cash expense when reporting "adjusted" free cash flow and "adjusted" EBITDA. This makes profitability metrics appear significantly more attractive than they are on a GAAP basis. Yet when these same companies then spend real cash on buybacks to offset the resulting dilution, the SBC that was characterised as "non-cash" effectively becomes a cash expense. As Morgan Stanley's Counterpoint Global research noted: "Companies should not get the benefit of adding back SBC expense without a full acknowledgement of the cost of buying back shares."

Counterpoint Global's research further demonstrated that companies with low SBC and high buybacks consistently generated superior total shareholder returns versus companies with high SBC and low buybacks. This held across both three-year and five-year measurement periods, and on both an absolute and risk-adjusted basis.

This SBC dynamic is particularly relevant in the context of our structural thesis. If gross margins are set to compress as the competitive moat around software development narrows, the SBC burden becomes even more painful. Companies that are already struggling to deliver genuine per-share value to shareholders through a period of peak margins will find it significantly harder to do so as margins contract. The treadmill accelerates precisely when the runner is slowing down.

Conclusion

The enterprise software sector is not experiencing a temporary crisis of confidence. It is undergoing a structural repricing driven by a fundamental challenge to the per-seat subscription model that has generated extraordinary margins and valuations for over a decade. AI is not making software irrelevant; it is making it cheaper to build, easier to replicate, and harder to price at a premium.

The behaviour of the people closest to these businesses is consistent with this view. Management teams are not aggressively buying back stock. Insiders are selling, not buying. And where buybacks exist, they are often running on the SBC treadmill, generating no net benefit for shareholders.

None of this precludes individual names from being mispriced, or the sector from experiencing tactical rallies. But for investors evaluating the broader "selloff is overdone" thesis, we would counsel caution. The evidence, both structural and behavioural, suggests this repricing has further to run.

.png)

%20(14).png)

.png)