Table of Contents

Markets have taken everything in stride – from tariff deadlines, to wars, to downward earnings revisions. At this stage, our aggregate model score is positive, with trend strength and earnings strength more than offsetting a decelerating economy and expensive valuations. Unless we see a material negative catalyst, especially from labor data, or markedly weak earnings guidance, the allocation to equities, especially growth sectors, warrants an overweight positioning.

We do expect a pause for breath in the uptrend, allowing momentum indicators to neutralize – aside from that, until reversed, goldilocks continues.

Please see our Investment Guide for a Detailed Presentation

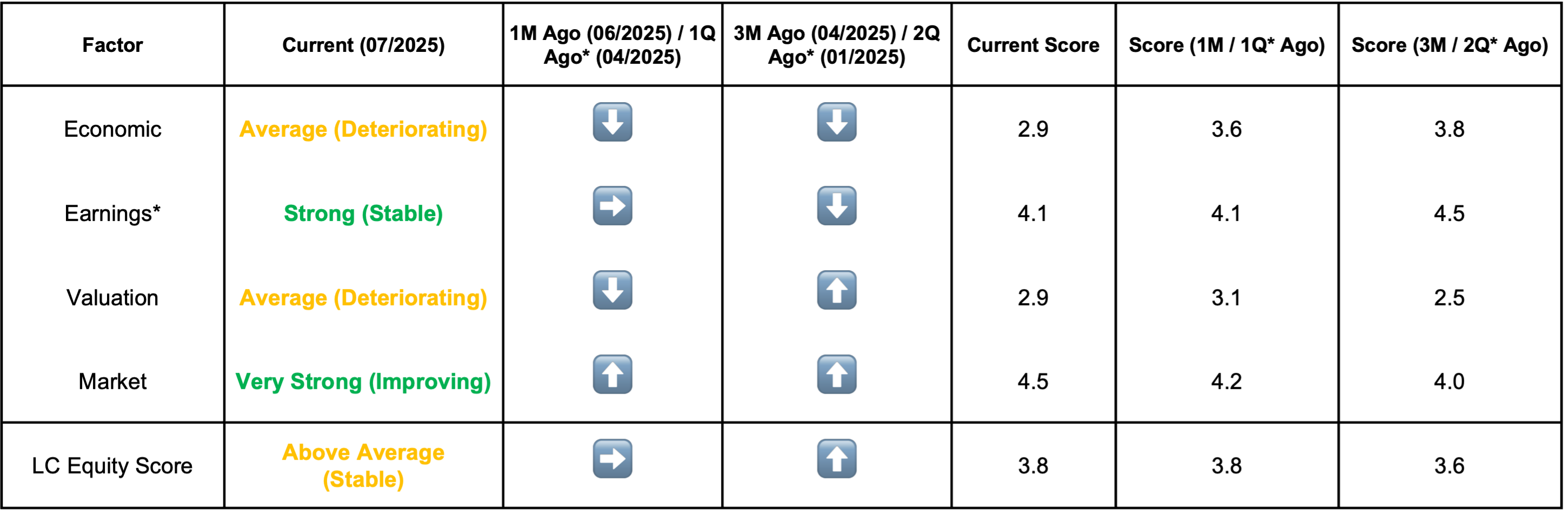

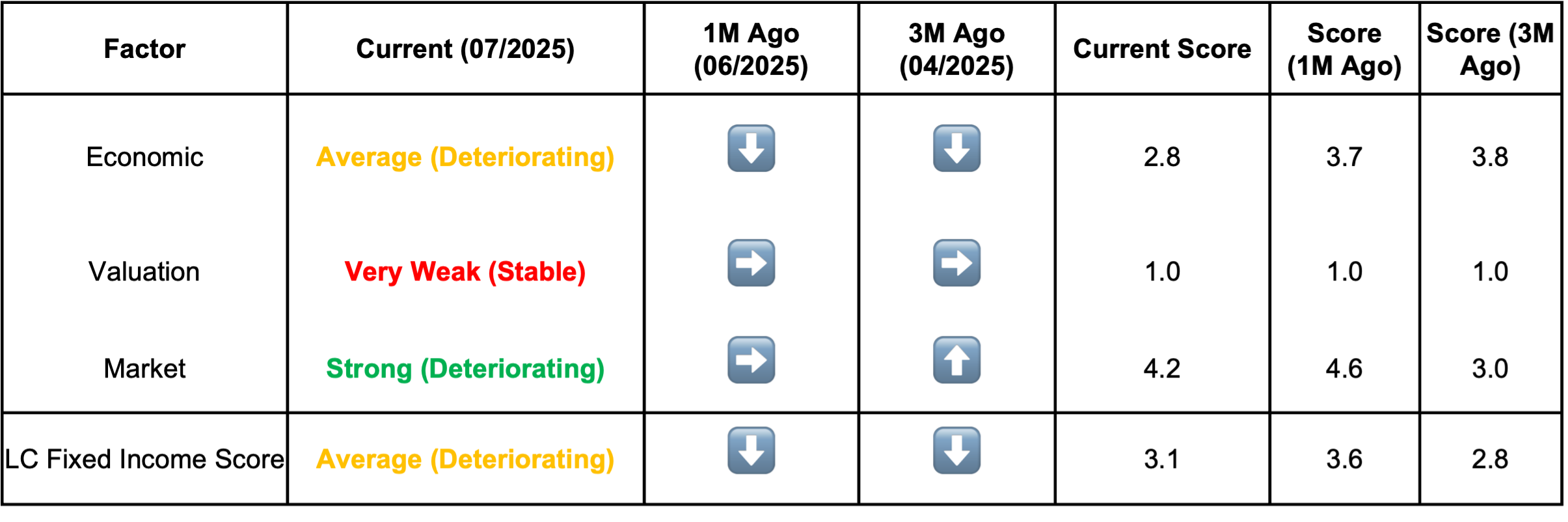

Model Summary

source: Lighthouse Canton

Executive Summary

- Macro Outlook - Our economic nowcaster suggests an economy that is decelerating but not collapsing - losing momentum across key pillars of consumption, housing, and business activity. Notable data coming week is inflation (consensus expects an uptick) and revival in Housing, after a shock collapse in May.

- Earnings Outlook – As 2Q kicks off, consensus expectations are muted for the quarter at 5% - appears to be an easy bar to beat. Guidance will probably be critical given market expectations of a marked slowdown for the rest of the year. Bank earnings will dominate coming week with focus on trading results from elevated volatility in 2Q and guidance related to easier capital requirements. Netflix among tech and GE in defence also keenly watched.

- Valuations – The dominant signal from the model is one of broad overvaluation – with downward earnings revisions, and an all-time high index, extent of overvaluation is higher than at the start of the year. Corporate bond valuations are back to expensive readings with credit spreads (both IG and HY) at record lows – Unattractive, except for European Financials.

- Market Signals– Solid uptrend in place supports long positioning. However, momentum appears to be flattening –although there isn’t a clear reversal sign as yet. It’s likely that the trend pauses to catch a breath and for momentum indicators to neutralize. Growth sectors better positioned on price action.

Asset Allocation Summary

- Overweight US Equities - Earnings strength and Market signals offset macro deceleration and expensive valuations. Delivering on earnings will be critical to sustain the trend.

- International Equities – China best positioned. India is a tactical downgrade with catalysts played out. Similarly for Europe, outperformance appears over for now.

- Underweight Bonds, except European Financials – Record low credit spreads make bonds unattractive.

- Currencies – Tactical long on DXY even though we agree with consensus long-term struggles for the Dollar.

- Gold, Oil and Bitcoin - Gold stuck in a range for three months, needs resolution out of the 3200-3400 range. Equities bullishness weakens short-term outlook for gold. Oil in short-term uptrend has long-term challenges. Bitcoin’s breakout into new high ground is solidly bullish.

- Alternatives – Macro strategies preferred positioning. Expected increase in volatility will continue to challenge trend following systematic strategies. Non-correlated strategies, private credit remain preferred.

Macro Outlook – Decelerating Momentum

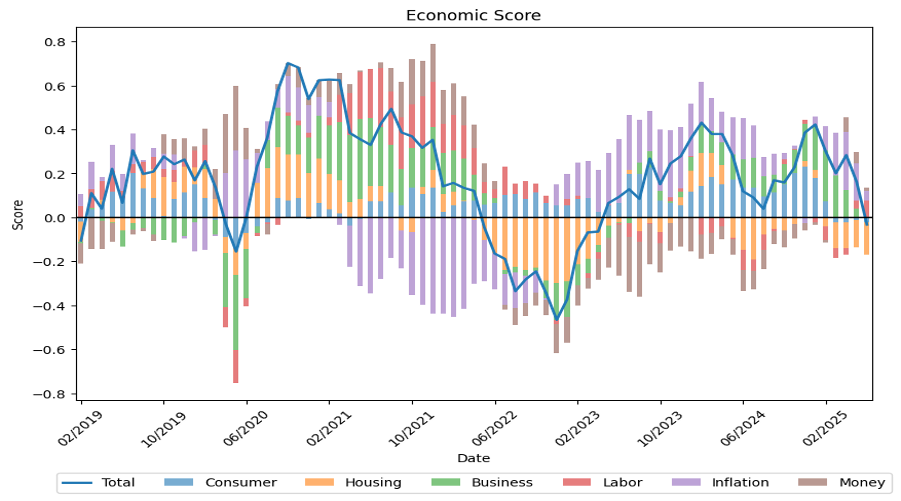

Lighthouse Canton Proprietary Economic Nowcaster

source: Lighthouse Canton

Our economic nowcaster suggests an economy that is decelerating but not collapsing - losing momentum across key pillars of consumption, housing, and business activity. Even inflation, while better than consensus expectations, is showing signs of deterioration, albeit moderate at this stage. Labor market remains the bright spot with not just positive readings, but also positive momentum – a key factor, in our view, holding up the broad economy. The environment appears more balanced than outright bearish –although softening breadth and declining trend in housing and consumer components warrant close monitoring.

Notable Data Coming Week:

- Inflation expected to pick up - CPI (Tuesday;June Consensus Core CPI 2.9% vs. 2.8% for May) and PPI (Wednesday; June CorePPI 3.2% vs. 3% in May). This remains a key decision criterion for the FED’s rate stance, currently concerned about tariff induced inflation

- Consumption – Consensus expects revivalin retail sales (Wednesday) after drop in May

- Housing – Consensus expects pick up inHousing Starts (Friday) after shock collapse in May.

Earnings – Muted Expectations – Guidance Critical

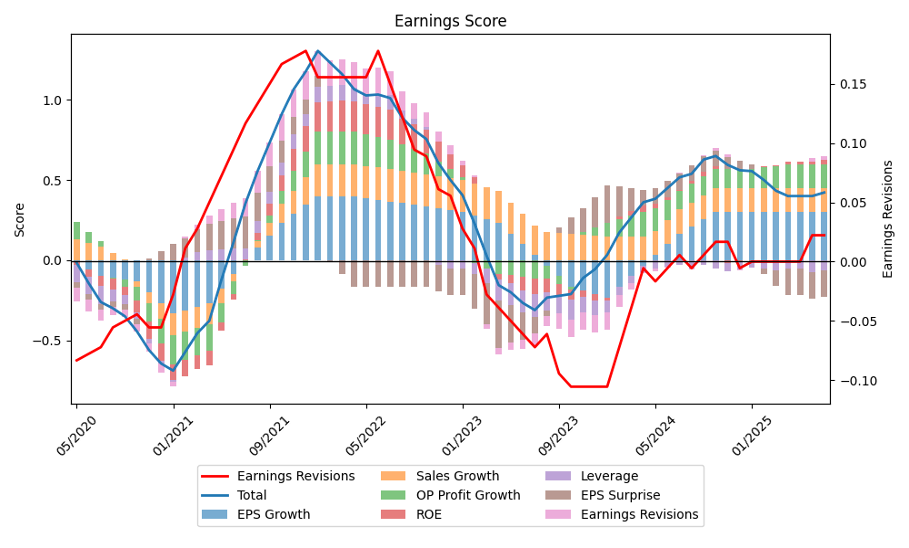

Lighthouse Canton proprietary Earnings Nowcaster

Source: Lighthouse Canton

Consensus Expects Deceleration: The aggregate earnings score remains strong and stable, with broad-based support from core growth and profitability metrics. However, with fewer earnings surprises and persistent leverage risks, the upside from here may be more selective. Unless revisions reaccelerate or surprises turn positive again, equity markets may require fresh catalysts to sustain higher valuations.

As the 2Q earnings season kicks off, consensus expectations are muted at a modest 5% EPS growth, a relatively easy bar to beat. What will be critical will be guidance for rest of the year given a somewhat low 9% consensus expectation.

2Q EPS Forecasts By Sector – Tech & Comm. Serv. Lead; Overall Muted

Source: Factset

Notable Earnings in Week of 14 Jul 2025:

- Bank Earnings Will Dominate the coming week – Major large cap banks all expected to report a strong 2Q backed by strength in trading given increased volatility in the quarter. Of interest will be guidance following expectations of easier capital rules

- Tech reporting will be lighter but notable will be Netflix, on a tear – both on earnings and share price trends.

- Defence is also a focus area and guidance from General Electric will set the stage for the sector, not just in the US, but globally

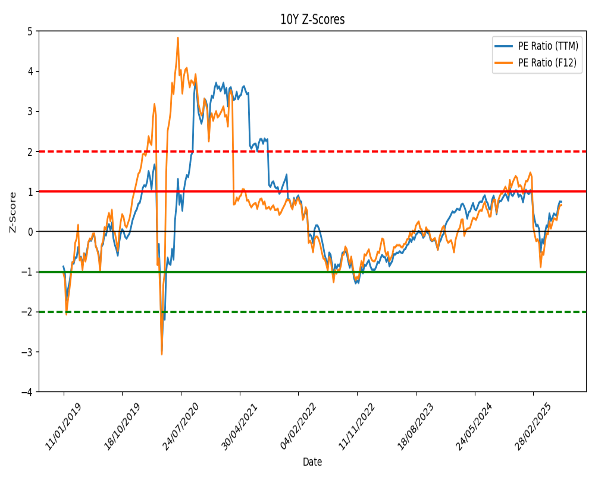

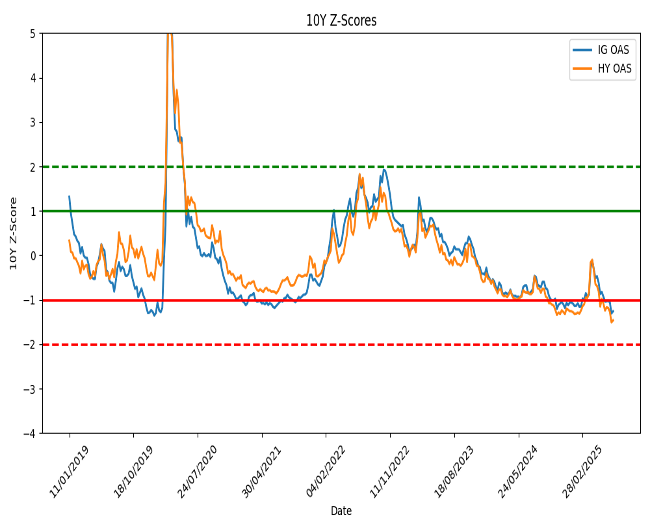

Valuations – Expensive – Both Equities & Bonds

The aggregate valuation score is "Average(Stable)", primarily due to EV/EBITDA offering an offset to stretched readings elsewhere. However, the dominant signal from the model is one of broad overvaluation – with downward earnings revisions, and an all-time high index, extent of overvaluation is higher than at the start of the year. Corporate bond valuations are back to expensive readings with credit spreads (both IG and HY)at record lows – Unattractive, except for European Financials.

TTM and Forward PE – Z-Score -Expensive Equities

Source:Lighthouse Canton

Credit Spreads – Record Lows

Source:Lighthouse Canton

Market Signals – Strong Trend, Pause for Breath Likely

Our market signal model remains solidly strong, especially due to a clear uptrend. With the index in new high ground, market signals suggest long positioning. Arguably, while the trend is strong, momentum appears to be flattening –although there isn’t a clear reversal sign as yet. It’s likely that the trend pauses to catch a breath and for momentum indicators to neutralize.

Lighthouse Canton proprietary Market Signals Model –Trend Strength

Source:Lighthouse Canton

S&P Daily – Uptrend in Place

Source: TradingView

Asset Allocation

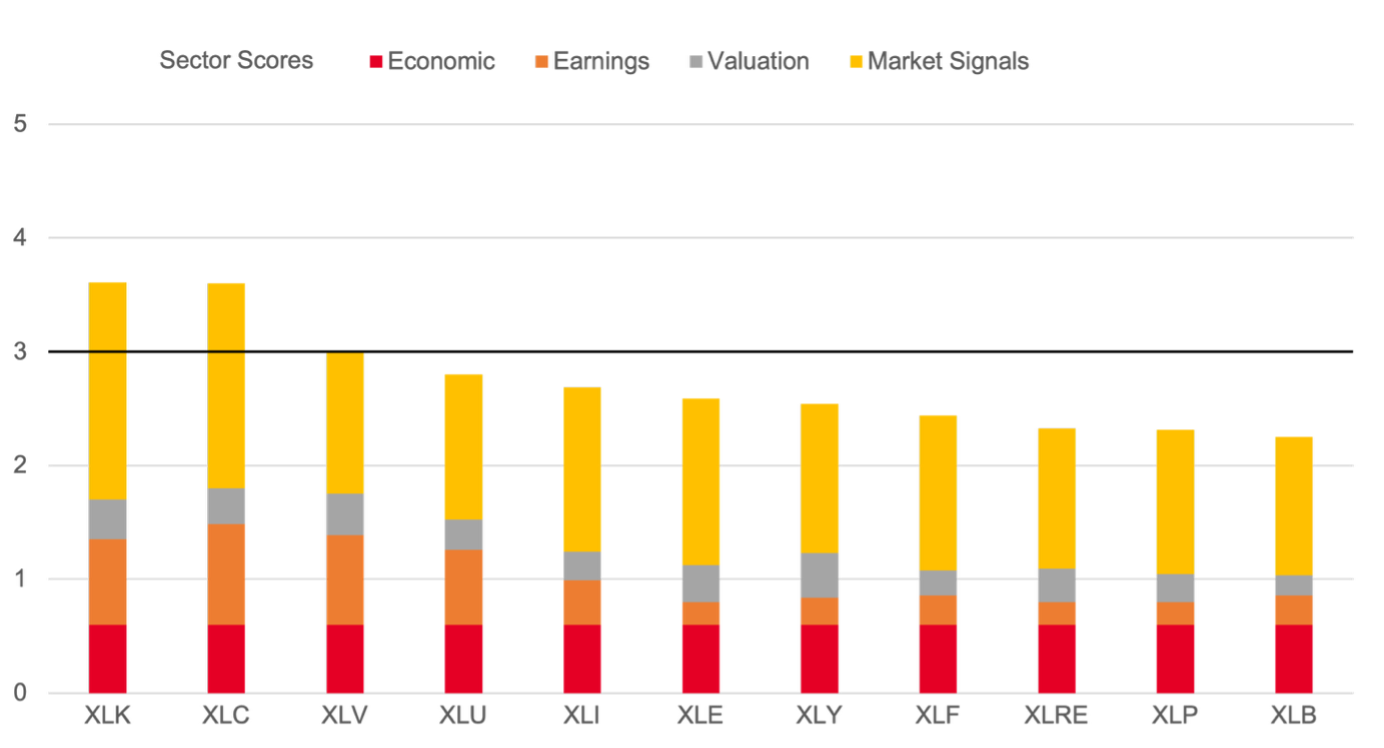

- Equities: Our proprietary nowcaster is overweight in equities with strength across earnings and particularly price signals offsetting macro deceleration and expensive valuations. Unsurprisingly, the model is overweight growth sectors at the cost of defensives. Amongst international equities, Europe’s outperformance, already retraced substantially, is no longer a given. China appears better placed while Japan struggles for direction near highs. We tactically downgrade India with most catalysts (rate cuts) played out and price signals suggesting caution ahead.

- Fixed Income: With credit spreads on both HY and IG corporate bonds back to record lows, other than European financials, corporate bonds do not appear attractive. As for treasuries, yields remain in balance – potential inflationary threats (from tariffs and easy financial conditions) offset by decelerating growth. We see a case for gradually increasing duration in portfolios.

- Currencies: Consensus view on the dollar is bearish citing risks from loss of US’ haven status as well a European/ EM revival. While the arguments for dollar bearishness appear sound, we see the move as having gone too far and expect a likely rebound in the DXY.

- Gold, Oil and Bitcoin: Gold is stuck in a range for the last three months – it needs resolution out of the 3200-3400 range. Should the bullishness in equities continue, the case for being long Gold remains weak, at least in the short-term. As for oil, the trend remains up, although the case for long-term bullishness is weak. Bitcoin’s breakout into new high ground is solidly bullish.

- Alternatives: With a dominant macro narrative, such strategies remain a preferred positioning. Volatility, currently depressed, is expected to rise and challenge trend following approaches. Relatively non-correlated strategies – insurance, life settlement and to a large extent private credit, remain a preferred positioning.

Rules Based Sector Positioning

Source: Lighthouse Canton

%20(16).png)

.png)