"Every rose has its thorn." Friday's May payrolls report was the thorniest of them all. Non-farm payrolls at 172,000, nearly doubling consensus expectations, while unemployment held steady at 4.3%. In any other universe, a resilient economy would be cause for celebration - except, a strong labor market is the ghost that haunts the inflation story - one we've been warning about since January.

The bears, of course, were waiting, sharpening their claws in the corner, ready to pounce the moment the music skips. And the music did skip on Friday. But before one reaches for the panic button, remember - we are in a market where the "Magnificent Few" have been compounding earnings at unprecedented levels, where AI capex programmes are being funded at a scale that makes the dot-com era look like a blip, and where the earnings trajectory, for now, remains unbroken. Without doubt there is froth. IPOs at 94x revenue. Vanishing free cash flows dressed up as visionary disruption. "Concepts", not businesses being capitalized on the strength of a founder's LinkedIn profile and a nice-looking deck. The euphoric crescendo is louder than before. But the critical question, the only question that matters for positioning is -"is the trend broken or merely dented?"

Despite our long-standing concerns on inflation, excessive valuations and the tell-tale signs of exuberance, there is not enough evidence to call for a clear trend-reversal. While early-stage indicators suggest need for hedges to protect recent gains, until the earnings trajectory diverges meaningfully from price action Or the latter reverses convincingly, the trend is not broken.

S&P – Reversing Underperformance vs. Nasdaq – Rotation at Play

source: Trading View

- Equities – Visible signs of rotation towards quality, defensives and value, away from growth and momentum factors. Tech & growth sectors remain outperformers, but trend is decelerating. Priced to perfection, any miss on earnings/ guidance invites exponential negative reactions. US equities preferred vs. ROW. Tactically reduce delta/ beta especially to growth biased portfolios, but stay invested, especially in AI infrastructure (upstream) with high visibility on demand and earnings.

- Fixed Income – With inflationary concerns to the fore, we remain underweight fixed income. Both basis risk (higher treasury yields) and spread risk (currently near record lows) make the asset class unattractive top-down. Quality and bias towards short to medium term durations recommended for fixed income biased portfolios.

- Oil & Oil Equities– The elusive “deal” in the Middle East continues to keep oil in an elevated tight range – any resolution will likely see sharp sell-offs. While we are not bullish oil prices, oil equities are likely to see an extended period of super-normal profits.

- Gold & Silver – Despite a positive fundamental outlook, neither gold nor silver are trading positively. Risk of higher rates remains a dampener for long positions. Elevated volatility for both gold & silver support the case for derivatives/ structured products to accumulate positions in what remains the best dollar diversifier (gold).

- The Dollar Remains Resilient – While we expect the FED to remain on an extended pause, even as other central banks are likely to raise rates (ECB notably), higher treasury yields and a “flight to growth and safety” are likely to keep the Dollar Index supported.

- Alternatives – Macro strategies have struggled thus far in 2026 while long-biased strategies have delivered. Long/Short strategies appear best positioned alongside strong macro managers.

Macro – Better Or Worse?

Proprietary EconomicNowcaster – Trends Are Worsening

source: Lighthouse Canton

The market may have been spooked by a “strong” payroll number, but the fact is that payrolls were down vs. previous readings. No doubt the labor market remains relatively resilient in a “low hire, low fire” environment – BUT, there is broad based deterioration as inflation bites into consumer confidence with implications for future spending.

- The payrolls double-take. 172,000 new jobs in May, on a consensus of 85,000 - and April was revised up to 179,000. Stronger job-openings, further support the resilient labor market narrative.

- Inflationary threats – Headline PPI at 6% and CPI at 3.8% have worsened materially and we remain of the view that an easing in Middle-East tensions will unlikely result in an immediate pullback in inflationary threats. In an insular world, with elevated commodity prices and fiscal profligacy in the western world, inflation is likely to remain a thorny issue.

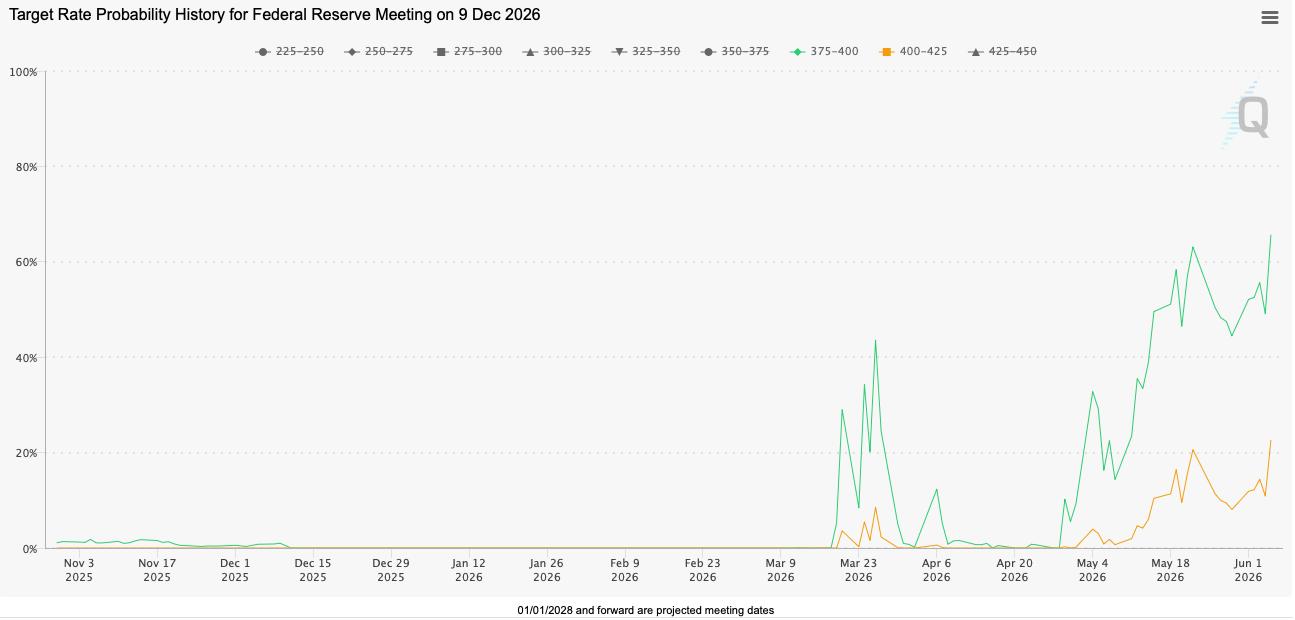

- The FED in a bind – From multiple cuts to none to now a 62% probability of a December hike – is how futures are pricing in the inflationary threat. While the mid-Jun FOMC is unlikely to see a rate change, commentary and dot plots will give an insight into how the Kevin Warsh FED is thinking. Given supply side heavy inflation drivers, we expect an extended pause rather than a hike.

Rate Hike Expectations- Rising

source: CME

source: Trading Economics

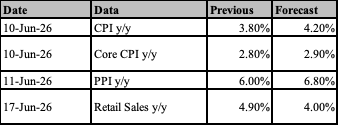

- CPI (10 Jun) - the moment of truth. A forecast of 4.20% against a previous 3.80% is already an admission that inflation is re-accelerating. If the print comes in at or above forecast, expect a violent repricing of rate expectations heading into the June 17 FOMC. A surprise to the upside can potentially force the market to price a July hike as a base case, rather than a tail risk. A downside surprise would offer temporary relief but would not, in our view, change the structural inflation narrative we have maintained since January.

- Core CPI (10 Jun) - the Fed's real compass. At 2.80% previously and 2.90% forecast, core is still elevated but not yet running away. The Fed's 2% target feels increasingly theoretical. Watch whether core surprises to the upside - that, more than the headline, will dictate the dot-plot language on June 17.

- PPI (11 Jun) - the dog that already barked. Previous reading of 6.00% year-on-year, with a forecast of 6.80%. This is not a number you dismiss. PPI is the upstream pressure that feeds into consumer prices with a 2–3 month lag. We have been flagging this since Q1. The market is now catching up. An upside surprise here, coming one day after CPI, would be the one-two punch that extinguishes any remaining rate-cut optimism.

- Retail Sales (17 Jun) - the consumer's confession. Forecast of 4.00%against a previous 4.90% suggests the consumer is beginning to crack under the weight of elevated prices and higher-for-longer borrowing costs. This is consistent with our proprietary Nowcaster's "broad-based deterioration" signal. A sharp miss here on the same day as the FOMC decision would create a genuinely stagflationary narrative - good for gold, bad for nearly everything else.

EARNINGS DRIVE VALUATIONS

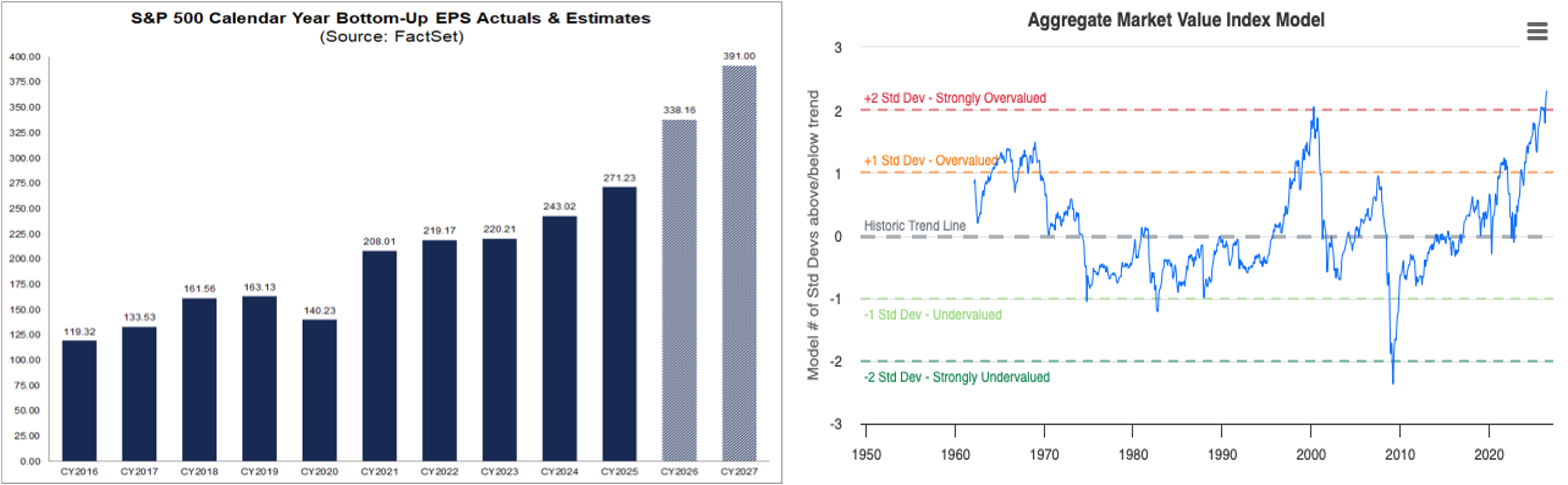

Rising EarningsExpectations – Do Valuations Matter?

source: Factset, Current Market Valuation

- Broadcom - The Icarus trade. Revenue of $22.2bn beat the $22.1bn consensus, and EPS of $2.44 topped the $2.39 estimate. By any conventional standard, this was a good quarter. AI semiconductor revenue surged 143% year-over-year, the 13th consecutive quarter of AI-centric growth. And yet, the company did not raise the full-year AI semiconductor target of $100bn+, and Q3 AI chip guidance of $16bn came in below the $17.2bn analyst consensus. In a market priced for exponential acceleration, "merely excellent" is a capital offence. The -12% single-day move is the starkest illustration yet of our core thesis - at these valuations, the margin for disappointment is zero.

- Upcoming - Oracle & Adobe. Both report this week.Oracle's cloud growth trajectory and any commentary on AI workloads will be closely watched, as will Adobe's AI-integration narrative in its creative suite. Any guidance caution will be punished severely given the current mood.

Earnings Outlook & Valuations – Following a blockbuster 1Q, earnings expectations remain elevated at 23% for 2026 and c16%for 2027. While equities are overvalued on most metrics, and they have been for a while, valuations are driven by earnings – as long as the earnings trajectory is supported, valuations will matter less in deciphering near-term returns for equities.

IPO Frenzy – Canary?

While not definitive, expensive IPOs, richly valued acquisitions are often associated with peak market behaviour (remember Time Warner- AOL?).

Space-X at 94x revenue is a bet on Elon Musk’s vision, hope and FOMO. Ever expanding valuations for Anthropic and Open AI rest on extrapolating current revenue trends. With compute capacity at a premium, can margin trends be extrapolated?

There is then the case of capital raising by businesses established 6 months ago on a “concept”, a leap of faith based on the founders’ pedigree and a nice looking presentation deck.

The transformation is real, as are demand and earnings. But canaries don't die gradually. They die suddenly, mid-song, and by the time you hear the silence it is already too late to get out cleanly. The question is not whetherAI is transformational. It is. The question is what perpetual growth rate is implied by a near trillion dollar valuation for a company that hasn't filed public accounts, or a $750 billion price tag for one that is still burning cash at scale. When Anthropic's confidential IPO filing hit the wires this week, alongside Alphabet's $80 billion equity raise and Meta's secondary offering, the fourth Horseman of the bubble framework quietly walked into the room. Three of four conditions (elevated valuations, retail inflows, frothy sentiment) have been present all year. Equity issuance at scale, the moment insiders rush to sell to the public, is the missing ingredient that has historically defined the peak. It is now arriving. We are not calling the top. But we are watching the door.

Market Signals – Rotational Trends

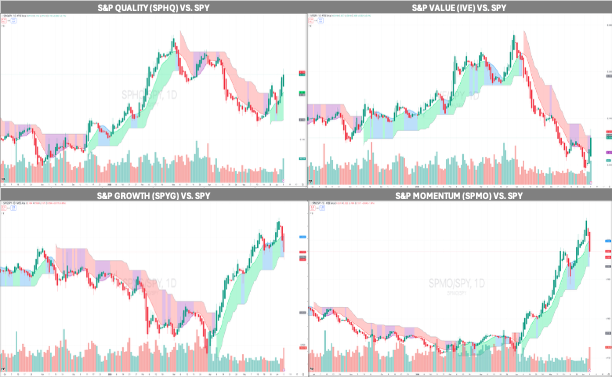

Growth and Momentum Give Way to Quality and Value – Whether the shift from growth and momentum, to quality and value factors, can sustain, remains to be seen – but for now, technicals support reducing beta/delta in growth biased portfolios.

Rotation – From Growth and Momentum to Quality and Value

The four-panel comparison tells a consistent story - Quality (SPHQ) and Value (IVE) are beginning to outperform the broader SPY benchmark, while Growth (SPYG) and Momentum (SPMO), the factors that have dominated the past two years, are rolling over. This is not yet a sustained rotation, but the directional shift is clear enough to act on tactically. The practical implication - portfolios that are heavily tilted toward high-multiple, high-momentum names should be trimming beta at current levels, not adding. The rotation to quality is not a bearish call, it is a sensible repositioning within a bull market that is maturing.

source: Trading View

Treasury Yields – Upside Bias – 4.5% remains a critical support for treasury yields and a bounce off these levels continues to suggest caution in owning bonds and treasuries, especially of the longer-duration variety.

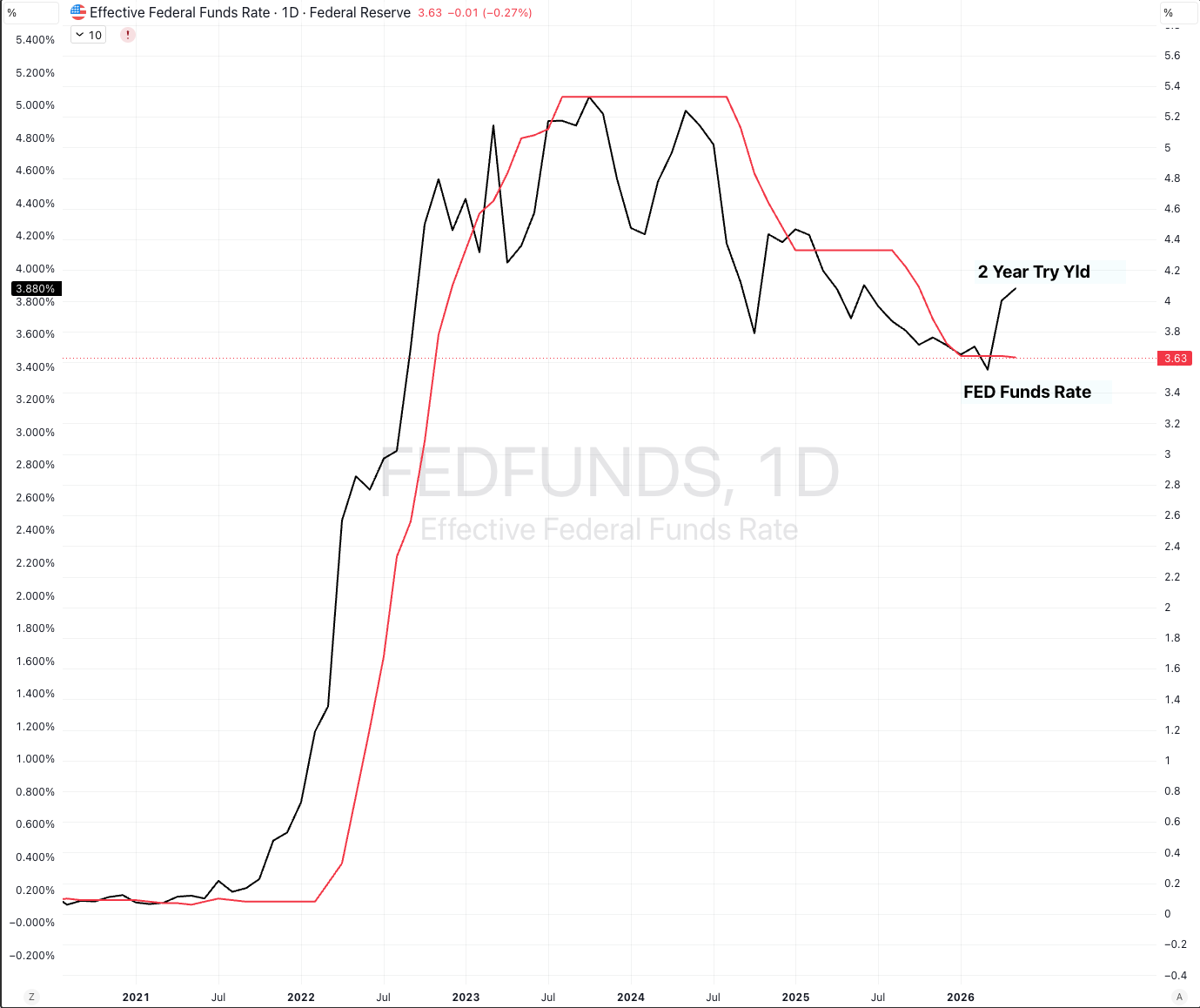

Will Treasury Yields Force the FED to Raise?

The chart overlays the 2-year Treasury yield against the Effective Federal Funds Rate - and the gap between them is the market's polite way of telling the Fed it is behind the curve. The 2-year yield, at 4.15%, is pricing in conditions that are tighter than the current Fed Funds Rate, which is a classic signal that the market expects the Fed to move. The question is the direction. Post-Friday's payrolls print, futures have moved to a 62% probability of a December hike - a number that was close to zero as recently as March. We expect an extended pause rather than an imminent hike, given the supply-side drivers of current inflation, but the direction of travel is unambiguous - the era of rate cuts is over.

source: Trading View

US > ROW – Momentum trends favour US equities relative to the rest of the world – resumption of a long standing trend. Emerging Markets (EEM) however remain supported, largely a Korea/Taiwan trade – not dissimilar to the Tech/ AI trade in the US.

ROW (ACWX) – Back to Underperforming the US (SPY)

The ACWX/SPY ratio has resumed its multi-year downtrend after a brief period of outperformance in early 2026 driven by dollar weakness and tariff-relief optimism. The message is blunt - US equities remain the destination of choice for global capital, and the momentum gap between US and rest-of-world is widening again. The notable exception within the EM complex is the Korea/Taiwan trade, essentially a proxy for global AI infrastructure demand via Samsung, SK Hynix, and TSMC. That trade remains supported so long as AI capex programmes continue. A meaningful deceleration in US tech earnings would hit Seoul and Taipei before it hits the S&P, watch those markets as a leading indicator.

source: Trading View

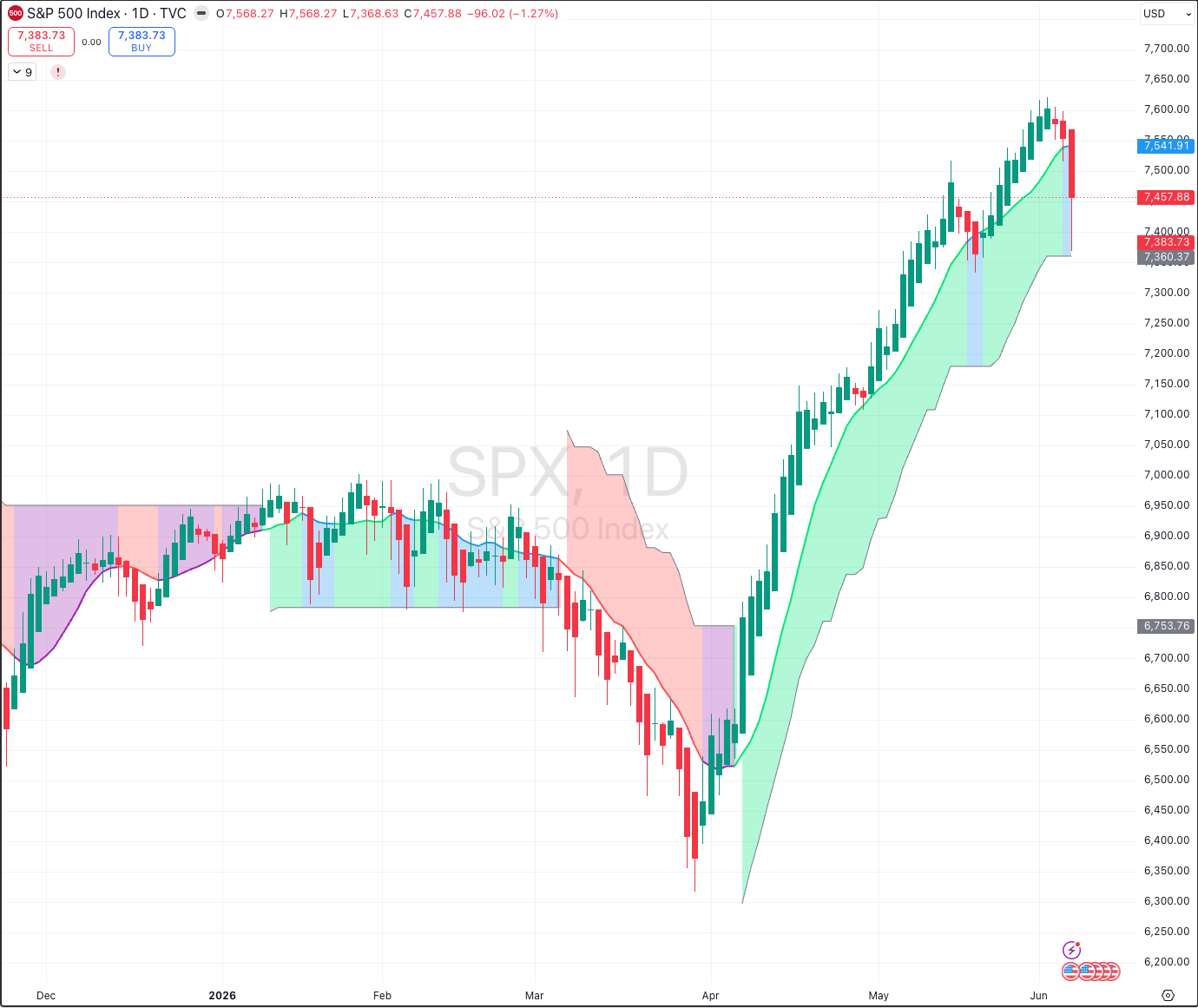

S&P Dented, Not Broken - The S&P 500's historic nine-week winning streak came to a crashing end on Friday, with the index shedding 2.64% (Nasdaq 100 down 4.77%) – our proprietary market signals model calls for protective hedges rather than a broken trend. While every major decline starts with a small one, there is not yet enough evidence to call for a trend reversal.

The S&P chart tells you everything you need to know about where we are. A clean breakout above 7,500, then a single Friday that takes you back to 7,383. Dented. Not broken, yet. The uptrend remains supported and the pullback appears to be just that, a correction. The next few weeks will define whether this was a healthy pause or the first crack in the foundation. June 10 CPI and June 17 FOMC are not just data points, they are the judgment on whether the inflation risk finally forces the market's hand. Stay invested. Reduce beta in growth-heavy portfolios. Add hedges. And watch the 7,000 level on the S&P, that is where the debate ends and the decision begins.

source: Trading View

.png)

%20(14).png)

.png)