Global markets are badly mispricing the structural roots of inflation, and when reality catches up, the repricing will be violent. Lighthouse Canton's Chief Investment Officer lays out the case for why a dip in oil prices will not fix what is fundamentally broken.

The macro call most investors are getting wrong is not about recession or rate cuts. It is about the durability of inflation and the danger of assuming that a geopolitical truce or a crude correction would make the problem disappear.

That is the warning from Sunil Garg, Managing Director and Chief Investment Officer at Lighthouse Canton, who argues that structural forces are lifting the global cost curve in ways the market has consistently failed to price.

"We have essentially gone into an insular world," Garg said. "Tariffs, although they keep going up and down, create uncertainty, but effectively the cost curve goes up, and somebody has to bear that cost."

The pressure does not stop at trade barriers.

Immigration restrictions across developed economies are tightening labour supply and pushing wages structurally higher. Key industrial commodities such as copper and uranium have seen sustained price gains that continue to feed through into production costs across sectors. Global commodity indices have reflected these pressures, with input costs remaining elevated even as headline energy prices fluctuate.

Layered on top is what Garg describes as chronic fiscal irresponsibility across the Western world.

"The entire Western world continues to be fiscally irresponsible," he noted. "The US has its major fiscal bill, Germany is spending more on defense, and the whole world will need to spend on defense. So fiscal impulse, commodity pressures, an insular world, and suddenly the whole inflation curve goes up," Garg explained.

Germany's decision to override its constitutional debt brake in early 2025, authorising hundreds of billions in additional spending, is precisely the kind of structural fiscal shift Garg sees markets discounting too readily.

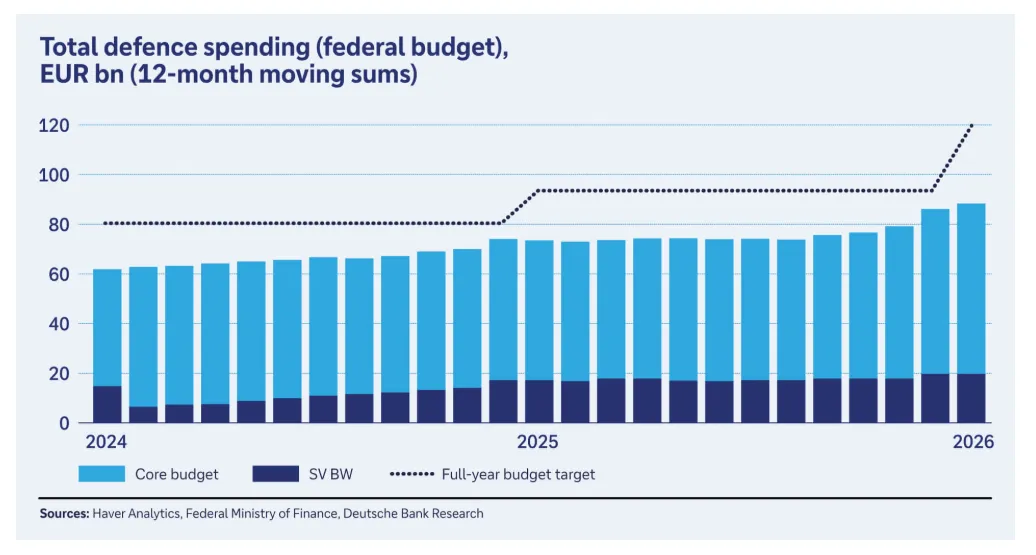

Source: Deutsche Bank (SV BW denotes Federal Armed Forces Fund)

NATO members have collectively committed to moving defense budgets toward 5% of GDP, a level not seen across the alliance since the Cold War.

The confluence of these pressures raises a scenario that markets are not pricing at all: stagflation. Rising costs, constrained monetary policy, and slowing corporate earnings can combine in ways that leave policymakers without effective tools to respond. Garg does not treat this as a base case but assigns it a material probability. "There is one possibility of a stagflation risk, and it is very high," he said, "though a lot of things need to happen for that to fully play out." The risk does not need to fully materialise to be disruptive. A partial repricing of that probability alone would be enough to move markets.

The real danger, in Garg's view, is not that inflation exists but that markets are treating it as an event rather than a condition.

"It is the single largest risk the market is under-appreciating and under-pricing," he said. "If there is peace in the Middle East tomorrow and oil collapses, inflation is still a problem."

That complacency is embedded in valuations.

Equity markets entered 2025 at stretched multiples, and credit spreads, while recently wider, had been compressing from historically tight levels. Neither asset class was offering meaningful compensation for a structurally higher inflation regime.

WHEN THE FED HAS NO GOOD OPTIONS

The Federal Reserve is caught between three options and none of them are clean. Garg frames the dilemma as a trap with no elegant exit and believes the most likely outcome is policy paralysis dressed up as deliberateness.

"If they ease, they will be repeating the 1973 mistake. If they tighten, that's going to anger the politicians. I think Fed Chair Powell has one meeting left and he's going to do nothing."

Doing nothing buys time but does not solve anything. If oil prices retreat and soften near-term inflation readings, the Fed may find temporary breathing room — but Garg argues that the structural inflation picture will not cooperate indefinitely. Rate cuts, in his view, are not the easy trade that markets were pricing at the start of the year.

There is also a currency dimension that investors are not fully accounting for. Interest rate differentials drive foreign exchange markets over meaningful time horizons. If U.S. rates remain elevated or push higher relative to peers, the widely anticipated dollar decline could sharply reverse.

"If inflation does rise sharply, you will oddly see money going into the US dollar, because US interest rates will rise, and currencies move based on interest rate differentials," Garg explained.

In case you missed it: On A Knife Edge | CIO Insights

PRIVATE CREDIT'S RECKONING HAS BEGUN

The bond market faces its own repricing. This is not just from inflation but from a recalibration of credit risk that has been deferred for years. Garg has been cautious on private credit for some time, and recent developments have confirmed rather than resolved his concerns.

The underlying logic is straightforward. Private credit is a lending business.

"Every lending business has a loss, and there is nothing wrong with that," Garg said. "But if the market starts to believe that this business will not have a loss, those are misplaced assumptions, and that's what's causing the upheaval."

Asian private credit differs here, added Garg. Asia continues to see lending to higher-quality borrowers with lower leverage and more conservative, lender-friendly frameworks. Despite its growth, the market is still relatively underpenetrated, shaping a more selective, borrower-focused investment approach rather than one driven purely by geography.

“We remain constructive on Asian private credit for these reasons," observed Garg.

Also read: Lighthouse Canton’s take on the recent private market turmoil and what investors need to focus on

For allocators, the implication is direct. Both public fixed income and private credit are offering inadequate compensation for the risks building in the background. In a world where the inflation curve has structurally shifted upward, the safe harbours are fewer than they appear.

.png)

%20(14).png)

.png)